Debt is an intrinsic part of the American financial landscape. For many, it’s a tool for achieving life goals – buying a home, pursuing higher education, or starting a business. For others, it can become a persistent burden, impacting financial well-being and future opportunities. Understanding the prevalence of debt across the American population is crucial for comprehending the broader economic health of the nation and for individuals to contextualize their own financial situations. This exploration delves into the statistics surrounding American indebtedness, examining the various forms debt takes and the demographics most affected.

The Ubiquity of Debt in American Households

The reality is that a significant majority of Americans carry some form of debt. This isn’t necessarily indicative of poor financial management; rather, it reflects the structure of the American economy and the common pathways to wealth accumulation and consumption. From mortgages to student loans, credit card balances to auto loans, debt is interwoven into the fabric of daily life for a vast portion of the population.

The Overwhelming Majority Carries Debt

Numerous studies and surveys consistently reveal that a substantial percentage of American households are in debt. These figures often exceed 70% and can climb higher depending on the specific definition of debt used and the demographic surveyed. This widespread indebtedness highlights how essential borrowing has become for achieving milestones that were once attainable through savings alone for a larger segment of the population. The perception of debt as a universal experience can sometimes normalize it, but it’s vital to distinguish between manageable, strategic debt and overwhelming, detrimental debt.

Defining “Debt”: A Multifaceted Concept

When discussing American debt, it’s imperative to define what constitutes “debt.” The term encompasses a wide array of financial obligations:

- Mortgage Debt: The most common form of secured debt, representing loans taken out to purchase real estate. These are typically the largest debts individuals carry but are also often considered investments with potential for appreciation.

- Student Loan Debt: A growing concern, this debt arises from financing higher education. While intended to increase earning potential, the burden of these loans can be substantial and long-lasting.

- Auto Loan Debt: Loans taken out to finance the purchase of vehicles. These are essential for many Americans to commute to work and manage daily life, but they represent depreciating assets.

- Credit Card Debt: Unsecured debt, often characterized by higher interest rates. This type of debt is frequently associated with discretionary spending and can quickly accumulate if not managed carefully.

- Personal Loans and Other Debts: This category includes various forms of unsecured debt, such as payday loans, medical debt, and personal loans taken out for various reasons.

The prevalence of each type of debt varies significantly across different income levels, age groups, and geographic locations, painting a complex picture of financial burdens.

Trends in American Indebtedness: A Shifting Landscape

The landscape of American debt is not static; it evolves with economic conditions, societal norms, and policy changes. Understanding these trends provides crucial context for the current state of debt in the U.S. and offers insights into potential future challenges and opportunities.

The Rise of Specific Debt Categories

Historically, mortgage debt has been a cornerstone of American household liabilities. However, in recent decades, other forms of debt have seen significant growth, particularly student loan debt and, to some extent, credit card debt. The escalating cost of higher education has made student loans almost a necessity for many, leading to an aggregate student loan debt that now rivals or exceeds credit card debt for many demographics. This trend has profound implications for wealth building and economic mobility, as individuals may delay major life decisions like homeownership or starting a family due to their student loan obligations.

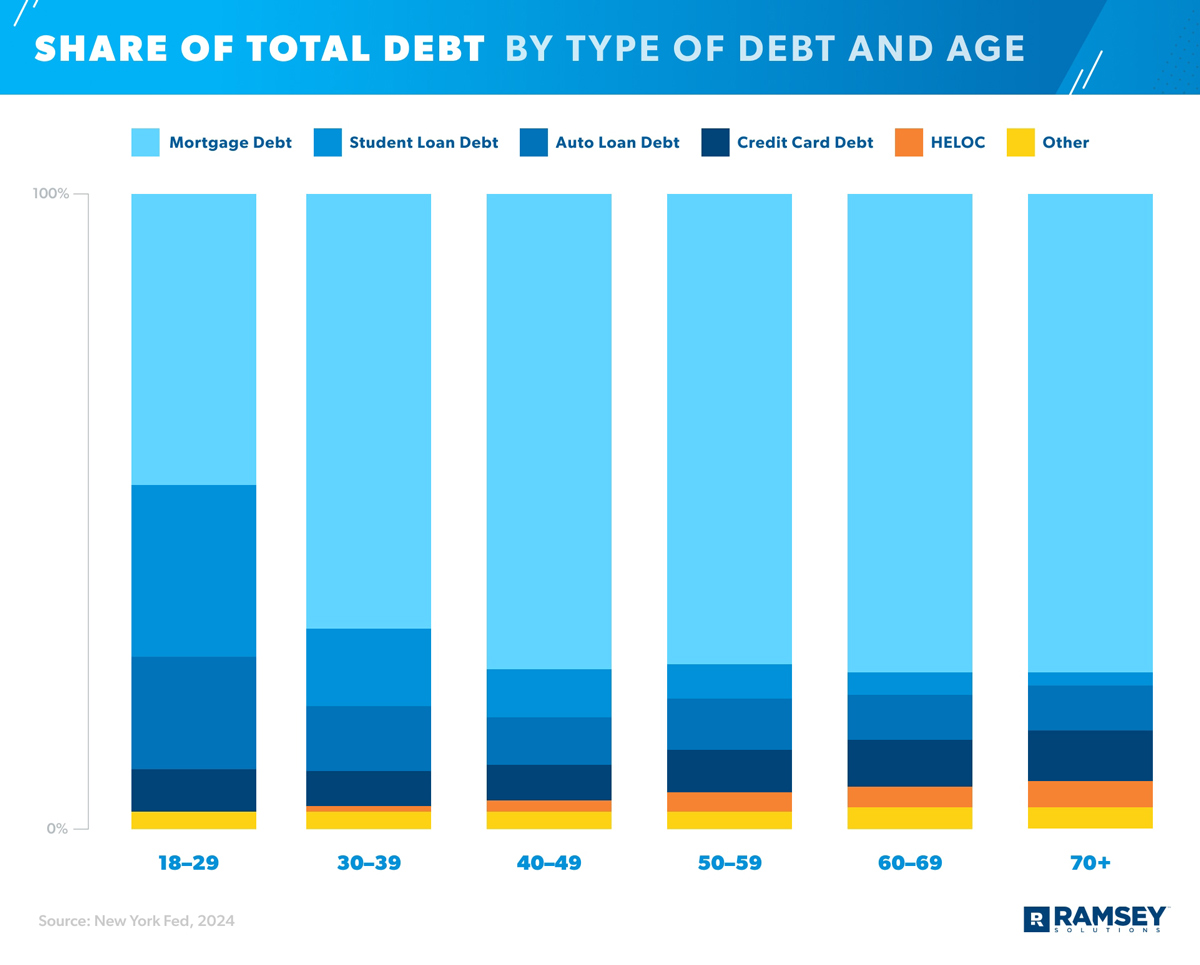

Generational Differences in Debt Burden

Generational cohorts often exhibit distinct patterns of debt accumulation and management.

- Baby Boomers: While many Baby Boomers may have paid off significant portions of their mortgages, they can still carry substantial debt, including home equity loans, medical debt, or lingering mortgage balances. Some may also be supporting adult children burdened by student loans.

- Generation X: This generation often finds itself juggling multiple forms of debt, including mortgages, student loans (both their own and potentially their children’s), auto loans, and credit card balances. They are often at the peak of their careers, making financial decisions that impact their retirement.

- Millennials: Millennials are notably burdened by student loan debt, often entering the workforce with significant financial obligations. Many also face challenges in homeownership due to high housing costs and their existing student loan burdens. Credit card debt is also a common concern.

- Generation Z: As they begin their financial journeys, Gen Z is already facing rising education costs and is likely to accumulate student loan debt. Their experience with credit cards and auto loans is just beginning to take shape.

These generational differences highlight how economic shifts and evolving societal expectations impact debt accumulation across different life stages.

The Impact of Debt on American Households

The presence of debt, especially significant or unmanageable debt, can have far-reaching consequences on individual financial health, mental well-being, and broader economic participation.

Financial Strain and Reduced Purchasing Power

High levels of debt, particularly high-interest debt like credit cards, can create significant financial strain. A substantial portion of a household’s income may be dedicated to debt repayment, leaving less for savings, investments, and discretionary spending. This reduced purchasing power can stifle economic growth at a macro level and limit individual opportunities for wealth creation and financial security. The constant pressure of debt payments can lead to stress, anxiety, and a diminished sense of financial control.

The Link Between Debt and Key Life Milestones

Debt can profoundly impact the ability of Americans to achieve critical life milestones. For instance, a significant student loan burden can delay or prevent individuals from saving for a down payment on a home, a traditional cornerstone of wealth building. Similarly, high credit card debt or other consumer loan obligations can make it more difficult to qualify for mortgages or auto loans, further hindering financial progress. This can create a cycle where debt prevents the very activities that could help one escape debt, impacting social mobility and economic equality.

Mental and Emotional Well-being

The psychological toll of debt cannot be overstated. Constant worry about making payments, the fear of default, and the feeling of being trapped by financial obligations can lead to significant stress, anxiety, depression, and even physical health problems. This mental burden can impact relationships, work performance, and overall quality of life. For many, debt is not just a financial problem but an emotional one, requiring a holistic approach to financial management that includes mental resilience.

Navigating the Debt Landscape: Strategies for Americans

While debt is prevalent, it doesn’t have to be an insurmountable obstacle. Understanding the nuances of debt and employing strategic financial management can help individuals navigate their obligations and work towards financial freedom.

Understanding Your Debt: Assessment and Prioritization

The first step in managing debt is understanding its scope. This involves:

- Inventorying all debts: Listing every outstanding debt, including the amount owed, interest rate, minimum payment, and due date.

- Categorizing debt: Distinguishing between good debt (e.g., mortgages, strategic student loans that enhance earning potential) and bad debt (e.g., high-interest credit card debt).

- Assessing affordability: Evaluating how much of your income is dedicated to debt repayment and identifying areas where spending can be reduced to accelerate payments.

Once a clear picture emerges, prioritizing debt repayment becomes crucial. Strategies like the debt snowball (paying off smallest debts first for psychological wins) or the debt avalanche (paying off highest interest debts first to save money) can be employed based on individual preferences and financial goals.

The Role of Financial Planning and Tools

Effective financial planning is essential for managing debt and building a secure future. This includes:

- Budgeting: Creating and sticking to a detailed budget is fundamental to controlling spending and allocating funds towards debt repayment and savings.

- Emergency Funds: Building an emergency fund is critical to prevent unexpected expenses from leading to new debt.

- Professional Guidance: Consulting with a financial advisor can provide personalized strategies for debt management, investment, and long-term financial planning.

- Utilizing Financial Apps and Tools: A plethora of digital tools exist to help with budgeting, debt tracking, and financial planning, making it easier for individuals to stay on top of their finances.

By taking a proactive and informed approach, Americans can move from being burdened by debt to strategically using it as a tool for financial progress, ultimately improving their financial well-being and achieving their life goals. The question of “what percent of Americans are in debt” is less about a single, alarming statistic and more about understanding the multifaceted nature of financial obligations and empowering individuals to manage them effectively.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.