An annuity, at its core, is a financial contract between an individual and an insurance company. It’s designed to provide a stream of regular payments to the annuitant, either immediately or at some point in the future. While the concept might seem straightforward, the world of annuities is rich with nuance, offering a variety of products tailored to different financial goals, risk tolerances, and time horizons. For individuals seeking a reliable income stream, particularly during retirement, understanding what an annuity means in practical financial terms is paramount. It represents a promise of future income, often used as a tool for wealth preservation and predictable cash flow, acting as a financial security blanket against the uncertainties of longevity and market volatility.

The Fundamental Mechanics of an Annuity

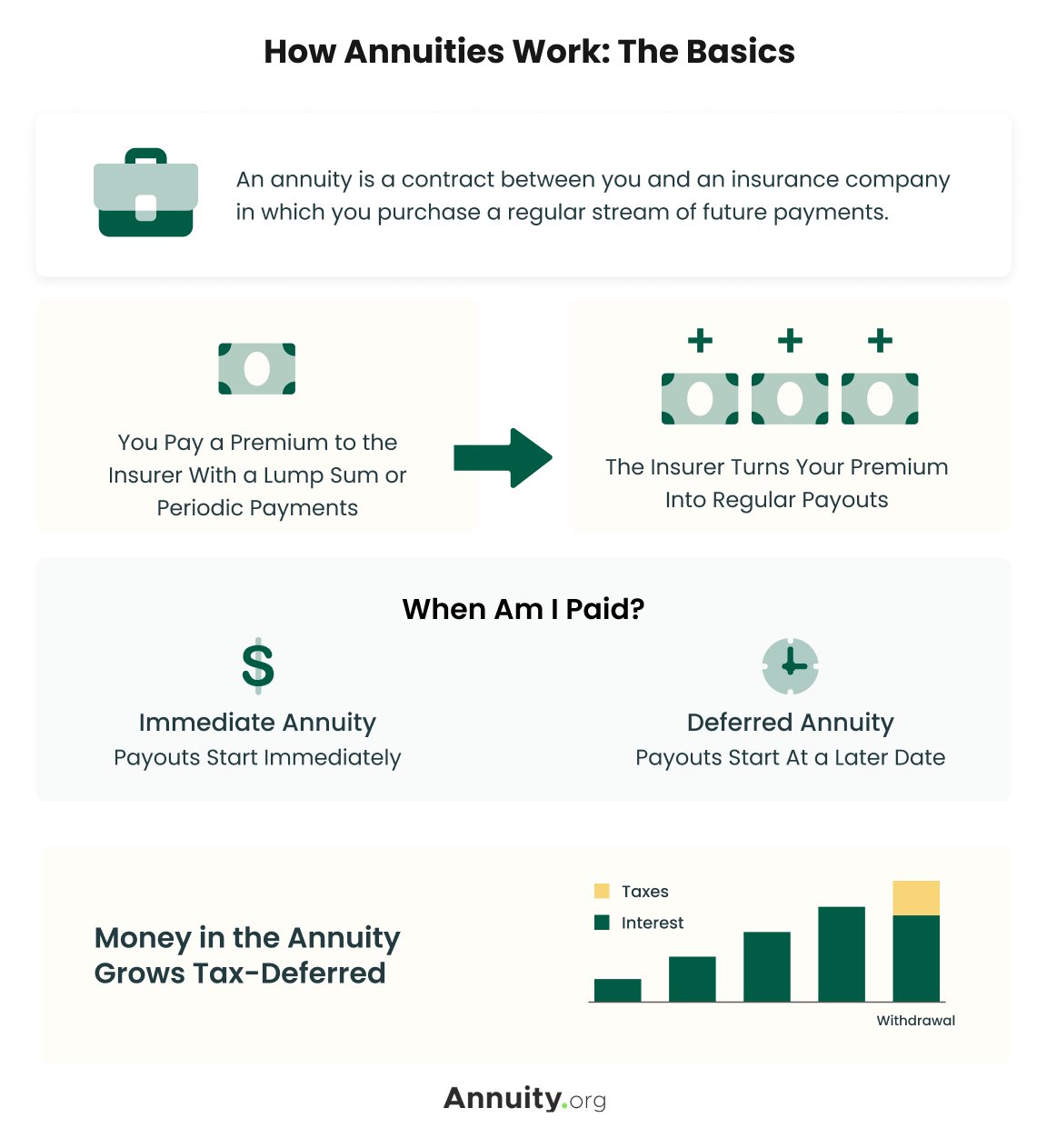

At its heart, an annuity is a contract. You, the annuitant (or the contract owner), make a payment or a series of payments to an insurance company. In return, the insurance company promises to make a series of payments back to you at a later date. This later date can be immediate, or it can be deferred to a future point, typically retirement. The fundamental principle is that you are essentially buying a guaranteed income stream.

The Two Phases: Accumulation and Annuitization

Every annuity contract goes through two distinct phases, though not all annuitants will experience both in the same way.

The Accumulation Phase

This is the period during which your investment grows. If you purchase a deferred annuity, you contribute funds to the contract, and these funds can grow tax-deferred. The growth within the annuity is typically based on a specific interest rate, investment performance, or a combination of factors, depending on the type of annuity. This phase can last for many years, allowing your money to compound over time. The key benefit here is the tax-deferred growth; you don’t pay taxes on the earnings each year, only when you start taking withdrawals or receiving payments.

The Annuitization Phase

This is the phase where the accumulated value is converted into a stream of income payments. You choose how and when you want to receive these payments. This is where the “annuity” aspect truly comes into play, as you are annuitizing your principal and earnings. The insurance company calculates the payment amounts based on the accumulated value, your life expectancy, the payout option you select, and prevailing interest rates at the time of annuitization. This phase provides the guaranteed income stream that is the primary appeal of annuities for many.

Types of Annuities: A Spectrum of Options

The term “annuity” is an umbrella term that covers a diverse range of products. These can be broadly categorized by how their earnings are determined and when payments begin.

Fixed Annuities: Predictable Stability

A fixed annuity offers a guaranteed rate of return during the accumulation phase and a guaranteed, fixed payment amount during the payout phase. This means your principal and earnings are protected, and you know exactly how much you will receive in income. They are ideal for conservative investors who prioritize safety and predictability over potentially higher, but riskier, returns. The trade-off for this security is that the growth potential is generally lower compared to other annuity types, and the fixed payments may not keep pace with inflation over long periods.

Variable Annuities: Market Participation with Growth Potential

Variable annuities offer the potential for higher growth because your money is invested in sub-accounts, which are similar to mutual funds. You can choose from a range of investment options, allowing you to participate in market performance. However, this also means your principal is at risk, as the value of your investments can fluctuate. During the annuitization phase, the payment amounts can vary based on the performance of these sub-accounts. Many variable annuities also offer optional riders for guarantees, such as guaranteed minimum withdrawal benefits (GMWBs) or guaranteed minimum income benefits (GMIBs), which provide some protection against market downturns while still allowing for growth potential.

Indexed Annuities: A Hybrid Approach to Growth

Indexed annuities, also known as fixed indexed annuities or equity indexed annuities, offer a unique blend of protection and growth potential. During the accumulation phase, your principal is typically protected, and your earnings are linked to the performance of a specific market index, such as the S&P 500. However, there are usually caps or participation rates that limit your upside potential. This means you can benefit from market gains up to a certain point, but you also won’t experience the full brunt of market losses. During the annuitization phase, the payout is often based on the accumulated value, which reflects the index-linked growth.

The Purpose and Benefits of Annuities in Financial Planning

Annuities are not simply investment products; they are financial planning tools designed to address specific needs, primarily related to income security and longevity risk. Their value lies in their ability to provide a dependable stream of income that can help individuals maintain their lifestyle throughout retirement.

Combating Longevity Risk: Outliving Your Savings

One of the most significant financial concerns in retirement is the risk of outliving one’s savings. With increasing life expectancies, individuals may spend decades in retirement, and traditional savings vehicles might not be sufficient to cover expenses for such an extended period. Annuities directly address this “longevity risk” by offering a guaranteed income for life, or for a specified period, regardless of how long you live. This peace of mind allows retirees to spend their savings with greater confidence, knowing a portion of their income is secured.

Tax-Deferred Growth and Retirement Income

As mentioned earlier, the accumulation phase of a deferred annuity provides tax-deferred growth. This means that any earnings generated within the annuity are not taxed until they are withdrawn or paid out. For individuals in their working years, this can be a powerful way to accelerate wealth accumulation, as their investments can grow without the annual drag of taxes. During retirement, when an individual’s tax bracket might be lower, receiving these payments can also be more tax-efficient than drawing from taxable investment accounts.

Guaranteed Income Streams for Specific Needs

Annuities can be structured to provide income for various needs. For instance, some individuals use annuities to supplement their Social Security benefits, ensuring a consistent cash flow for essential living expenses. Others may use them to fund specific goals, such as paying for healthcare costs in retirement or leaving a legacy for their heirs. The flexibility in payout options allows for customization to meet a wide range of individual circumstances and financial objectives.

Potential Drawbacks and Considerations When Purchasing an Annuity

While annuities offer compelling benefits, it’s crucial to approach them with a clear understanding of their potential downsides. Like any financial product, they come with trade-offs and complexities that individuals must carefully consider before committing their funds.

Fees and Charges: The Cost of Guarantees

Annuities, especially variable and indexed annuities, can come with a variety of fees and charges. These can include mortality and expense (M&E) charges, administrative fees, sub-account management fees, and fees for optional riders. These fees can erode the overall returns of the annuity, particularly if the underlying investments do not perform exceptionally well. It is essential to meticulously review the contract’s fee structure and understand how these costs will impact your net earnings and eventual payout.

Surrender Charges and Liquidity Issues

Many annuities have surrender charges, which are penalties imposed if you withdraw more than a certain amount of money from the contract before a specified period, often 5 to 10 years. These charges can be substantial and significantly reduce the amount of money you receive if you need early access to your funds. This lack of liquidity means annuities are best suited for long-term savings goals, and individuals should ensure they have adequate emergency funds elsewhere before committing money to an annuity.

Complexity and Transparency

The diverse range of annuity products and their intricate features can make them complex to understand. Variable annuities, with their investment sub-accounts and optional riders, can be particularly confusing. The guarantees and limitations of indexed annuities can also be challenging to decipher. It’s vital to work with a qualified financial advisor who can clearly explain the terms, conditions, and implications of any annuity product you are considering, ensuring you fully grasp what you are purchasing.

Inflation Risk with Fixed Payouts

For annuities with fixed payout amounts, there is a risk that the purchasing power of those payments could diminish over time due to inflation. While the payment amount remains constant in nominal terms, its real value can decrease if the cost of living rises faster than the annuity payments. Some annuities offer inflation-adjusted payout options, but these often come with a lower initial payment.

Conclusion: Annuities as a Strategic Component of Financial Security

In essence, “what means annuity” translates to a contractual promise of future income, designed to address critical financial planning needs, particularly in retirement. They are not a one-size-fits-all solution but rather a sophisticated tool that, when understood and chosen appropriately, can provide significant financial security and peace of mind. For individuals seeking to mitigate longevity risk, benefit from tax-deferred growth, and secure a predictable income stream, annuities can play a valuable role. However, a thorough understanding of the different types of annuities, their associated costs, surrender charges, and inherent complexities is crucial. By carefully evaluating your financial goals, risk tolerance, and time horizon, and by seeking professional guidance, you can determine if an annuity is the right strategic component to enhance your long-term financial well-being.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.