For millions of Americans, Social Security represents a cornerstone of their retirement security, providing a reliable income stream that helps cover essential living expenses. Yet, despite its critical role, many individuals lack a clear understanding of how their monthly Social Security benefit is actually calculated. It’s not a one-size-fits-all figure, but rather a complex computation based on a unique combination of your earnings history, your age at retirement, and several other contributing factors. Understanding these elements is paramount for effective retirement planning, allowing you to make informed decisions that could significantly impact your financial well-being in your golden years.

This comprehensive guide will demystify the intricacies of Social Security benefit determination, breaking down the key components that the Social Security Administration (SSA) uses to calculate your payment. By grasping these fundamentals, you can better estimate your future benefits, strategize your claiming age, and integrate Social Security more effectively into your broader financial strategy.

The Foundational Pillar: Your Earnings History

At the heart of your Social Security benefit calculation lies your lifetime earnings record. The system is designed to provide benefits that are progressive, meaning lower-income workers receive a higher percentage of their past earnings back than higher-income workers, but the absolute dollar amount is still heavily influenced by how much you’ve earned over your career.

The Role of Covered Earnings

Social Security benefits are funded by dedicated payroll taxes (FICA taxes) paid by both employees and employers. Only earnings up to a certain annual limit, known as the Social Security “taxable maximum,” are subject to these taxes and count towards your benefit calculation. Any income earned above this annual limit (which adjusts annually) does not contribute further to your Social Security record for that year.

To qualify for Social Security retirement benefits, you generally need to accumulate 40 “credits” of work, which typically translates to 10 years of employment. You can earn up to 4 credits each year, with each credit requiring a minimum amount of earnings (this minimum also adjusts annually). While 40 credits are required for eligibility, the amount of your benefit depends on a much longer earnings history.

Calculating Your Average Indexed Monthly Earnings (AIME)

The SSA doesn’t just look at your raw historical earnings. Instead, it uses a process called “indexing” to adjust your past earnings for changes in the national average wage level over time. This ensures that the purchasing power of your early career earnings is comparable to your later career earnings when calculating your benefit.

Here’s the general process:

- Identify Your Top 35 Years: The SSA takes your highest 35 years of indexed earnings. If you haven’t worked for 35 years, any years short of that will be counted as zero-earning years, which will reduce your overall average.

- Sum and Divide: These 35 years of indexed earnings are summed up and then divided by 420 (the number of months in 35 years) to arrive at your Average Indexed Monthly Earnings (AIME). This AIME is the core figure used to determine your Primary Insurance Amount (PIA).

- The Primary Insurance Amount (PIA): Your PIA is the basic benefit amount you would receive if you claim benefits at your Full Retirement Age (FRA). It’s calculated by applying a progressive formula to your AIME using “bend points.” These bend points are dollar amounts that separate different tiers of your AIME, to which different percentages are applied (e.g., 90% of the first segment, 32% of the next, 15% of the remainder). This progressive formula is what gives lower-income workers a higher replacement rate of their earnings.

The Impact of Zero-Earnings Years

It’s crucial to understand the impact of years with no earnings or very low earnings. If you work for fewer than 35 years, the SSA will fill in the missing years with zeros when calculating your AIME. For example, if you worked for 30 years, there would be 5 years of zero earnings averaged into your calculation, which significantly lowers your AIME and, consequently, your PIA. This highlights the importance of consistent work history, especially if you have periods out of the workforce.

Timing Is Everything: Age and Claiming Strategies

While your earnings history determines your base benefit (PIA), the age at which you decide to start receiving your Social Security benefits is one of the most powerful factors you control, directly affecting the monthly payment you will receive for the rest of your life.

Understanding Full Retirement Age (FRA)

Your Full Retirement Age (FRA), sometimes called “normal retirement age,” is the age at which you are entitled to 100% of your Primary Insurance Amount (PIA). This age varies depending on your birth year:

- Born 1943-1954: FRA is 66

- Born 1955: FRA is 66 and 2 months

- … (incrementally increasing)

- Born 1960 or later: FRA is 67

Knowing your FRA is critical because it serves as the benchmark for any adjustments to your benefit amount, whether you claim early or delay.

Claiming Early: The Permanent Reduction

You can begin receiving Social Security retirement benefits as early as age 62. However, claiming before your FRA results in a permanent reduction of your monthly payment. The reduction is approximately 5/9 of 1% for each month you claim early, up to 36 months. If you claim more than 36 months early, the reduction is 5/12 of 1% per month.

For someone with an FRA of 67, claiming at age 62 would result in a permanent reduction of about 30% of their PIA. This means if your PIA was $1,500, claiming at 62 would reduce your monthly benefit to around $1,050. This reduction is permanent and will apply for the remainder of your life, unless you suspend benefits and restart them later (which is generally only possible if you claim after FRA).

Delaying Benefits: The Advantage of Delayed Retirement Credits

Conversely, you can choose to delay claiming your Social Security benefits past your FRA, up to age 70. For each year you delay past your FRA, your monthly benefit increases by a certain percentage, known as Delayed Retirement Credits (DRCs). This increase is approximately 8% per year (or 2/3 of 1% per month) for those born in 1943 or later.

Delaying benefits provides a significant financial incentive. For example, if your FRA is 67 and you delay claiming until age 70, your monthly benefit will be 124% of your PIA (100% at FRA + 3 years x 8% per year = 24% increase). If your PIA was $1,500, delaying to age 70 would boost your monthly payment to $1,860, a substantial increase compared to claiming early or even at FRA. This strategy is particularly appealing for individuals who are in good health, have other retirement income sources, and anticipate a long lifespan.

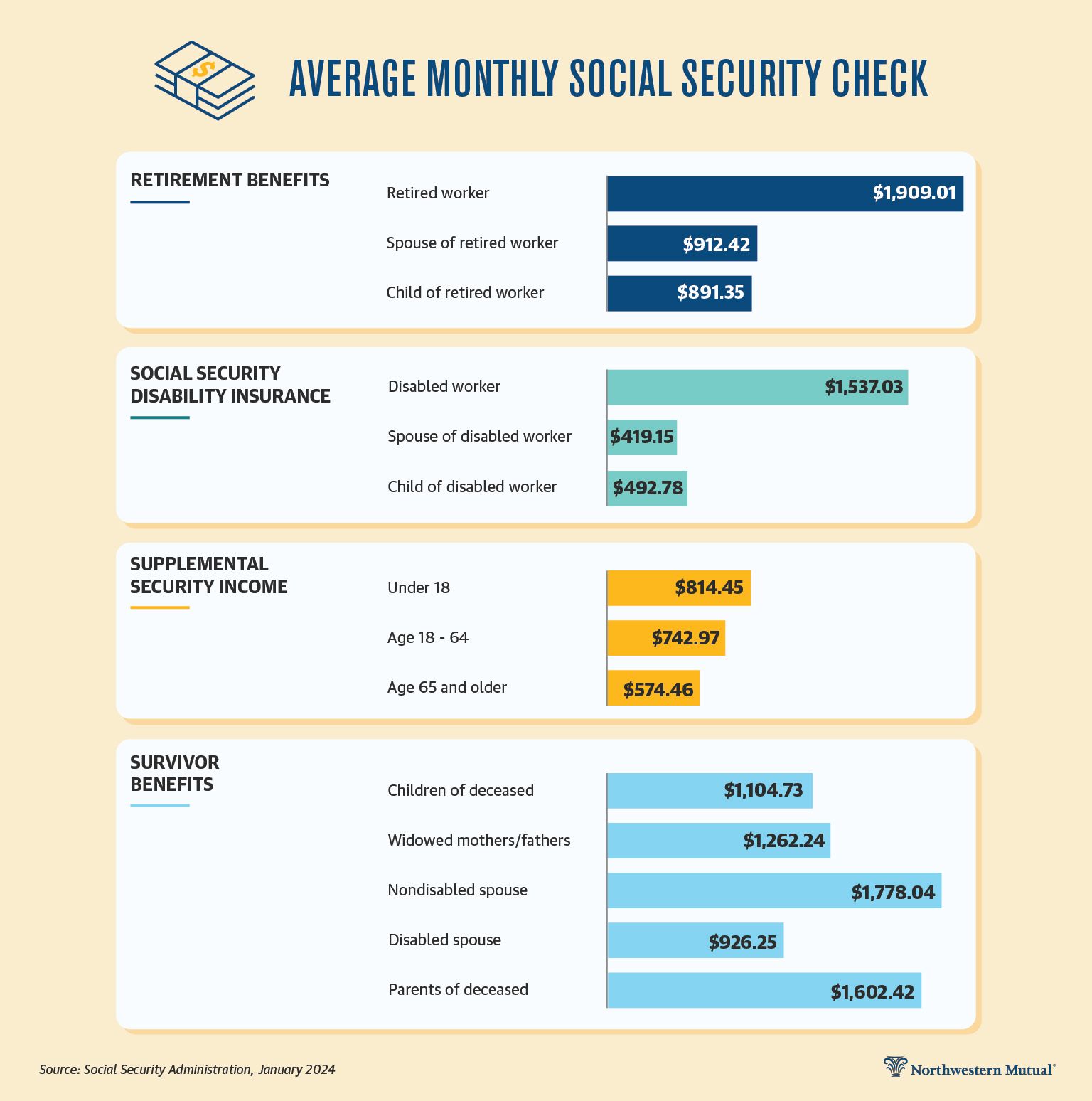

Beyond Your Own Record: Spousal, Survivor, and Disability Benefits

Social Security isn’t just about your individual retirement benefit. It also provides a safety net for families through spousal, survivor, and disability benefits, which are tied to the earnings record of a primary worker.

Benefits for Spouses and Divorced Spouses

If you are married or were previously married, you might be eligible for benefits based on your spouse’s (or ex-spouse’s) earnings record, even if you have little or no earnings history of your own.

- Spousal Benefits: A spouse can claim up to 50% of the primary earner’s PIA if they claim at their own FRA. If the spouse claims early, their benefit will be reduced. A key rule is that the primary earner must have filed for their own benefits for the spouse to collect spousal benefits, unless the spouse is filing under the “file and suspend” strategy (which has been limited significantly).

- Divorced Spousal Benefits: If you were married for at least 10 years, are currently unmarried, and your ex-spouse is at least 62, you may be eligible for benefits based on their record. The amount is similar to spousal benefits (up to 50% of their PIA), and importantly, claiming these benefits does not affect your ex-spouse’s benefits or their current spouse’s benefits.

Survivor Benefits: Supporting Loved Ones

Social Security provides crucial financial support to surviving family members when a worker passes away. Eligible survivors can include:

- Widows/Widowers: Can receive benefits as early as age 60 (or 50 if disabled), or at any age if caring for the deceased worker’s child under 16 or disabled. The full survivor benefit can be up to 100% of the deceased worker’s benefit amount if claimed at the survivor’s FRA.

- Dependent Unmarried Children: Can receive benefits if they are under age 18 (or 19 if still in high school), or at any age if disabled before age 22.

- Dependent Parents: In some cases, if the deceased worker provided at least half of their support.

These benefits are essential for families coping with the loss of an income provider, helping to replace a portion of the lost earnings.

Social Security Disability Insurance (SSDI)

If you become disabled and are unable to work, Social Security Disability Insurance (SSDI) can provide income replacement. Eligibility is based on having worked long enough and recently enough, accumulating a certain number of work credits. The amount of your disability benefit is essentially your full Primary Insurance Amount (PIA), calculated as if you had reached your FRA at the time of your disability. SSDI serves as a vital safety net, protecting individuals and families from financial hardship due to severe health conditions.

Navigating the Nuances: COLAs, Taxation, and Maximums

Beyond the core calculation, several dynamic factors and limitations can influence the actual dollar amount of your Social Security payment and its net value.

Cost-of-Living Adjustments (COLAs)

To help maintain the purchasing power of benefits in the face of inflation, Social Security benefits are subject to annual Cost-of-Living Adjustments (COLAs). Each year, typically in October, the SSA announces the COLA for the following year, which is based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). If the CPI-W shows an increase, benefits are adjusted upwards accordingly starting in January. This automatic adjustment is a critical feature, helping retirees’ fixed incomes keep pace with rising costs over time.

Taxation of Social Security Benefits

While often considered a sacred cow, a portion of Social Security benefits can be subject to federal income tax, depending on your “provisional income.” Provisional income is calculated as your Adjusted Gross Income (AGI) + tax-exempt interest + 50% of your Social Security benefits.

- Individuals: If your provisional income is between $25,000 and $34,000, up to 50% of your benefits may be taxable. Above $34,000, up to 85% of your benefits may be taxable.

- Married Filing Jointly: If your provisional income is between $32,000 and $44,000, up to 50% of your benefits may be taxable. Above $44,000, up to 85% of your benefits may be taxable.

Additionally, some states also tax Social Security benefits, further impacting the net amount you receive. It’s important to factor potential taxation into your retirement income planning.

The Maximum Benefit Limit

While high earners will receive higher Social Security payments, there is an upper limit to the monthly benefit anyone can receive. This “maximum benefit” is the highest possible monthly amount for a worker claiming at their Full Retirement Age. This limit is adjusted annually and depends on the highest taxable earnings history over 35 years. For example, in 2024, the maximum benefit for someone claiming at FRA was $3,822. This means that even if your indexed earnings history would technically produce a higher PIA, your benefit will be capped at this maximum.

Strategic Planning for a Secure Retirement

Understanding the mechanics of Social Security is only the first step. The real value comes from leveraging this knowledge to make optimal decisions for your retirement.

Accessing Your Social Security Statement

The easiest and most effective way to understand your personalized Social Security benefit is to regularly check your Social Security Statement. You can create an account and access your statement online at the SSA website (ssa.gov/myaccount). This statement provides:

- Your complete earnings history (crucial for checking accuracy).

- Estimates of your retirement benefits at various claiming ages (62, FRA, 70).

- Estimates of potential disability and survivor benefits.

Regularly reviewing this statement allows you to identify any discrepancies in your earnings record and helps you project your future income streams.

Factors to Consider in Your Claiming Decision

Deciding when to claim Social Security is a highly personal decision with no single “right” answer. Key factors to weigh include:

- Health and Longevity: If you anticipate a long lifespan, delaying benefits generally results in a higher cumulative payout over your lifetime. If your health is poor, claiming earlier might be more advantageous.

- Other Income Sources: Do you have significant savings, pensions, or other retirement income? If so, you might be able to afford to delay Social Security and let your benefits grow.

- Spousal/Family Needs: The claiming decision can impact spousal and survivor benefits. A higher earner delaying their benefits also increases the potential survivor benefit for their spouse.

- Employment Status: Are you still working? If you claim benefits before FRA while still working, your benefits may be reduced if your earnings exceed certain limits.

- Tax Implications: Consider how claiming Social Security might affect your overall tax situation.

Integrating Social Security into Your Overall Retirement Plan

Social Security should be viewed as one component of a holistic retirement income strategy, not the sole source. It typically replaces about 40% of an average worker’s pre-retirement earnings, meaning other savings and investments are critical. Use your estimated Social Security benefits as a baseline, and then plan how your 401(k), IRAs, pensions, and other assets will bridge the gap to meet your desired lifestyle in retirement. Consulting with a financial advisor can provide personalized guidance on optimizing your Social Security claiming strategy within your broader financial plan.

In conclusion, your Social Security payment is based on a robust calculation factoring in your indexed lifetime earnings, your Full Retirement Age, and your actual claiming age. Beyond that, it offers critical protections for spouses, survivors, and disabled individuals, while adapting to economic changes through COLAs. By taking the time to understand these elements, you empower yourself to make better financial decisions, ensuring Social Security plays its intended role in securing your financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.