Social Security stands as a cornerstone of financial security for millions of Americans, providing retirement income, disability benefits, and support for survivors. For many, it represents a significant, if not primary, source of income in their later years. Yet, despite its pervasive influence, the mechanics behind how individual benefits are calculated often remain a mystery. Understanding what your Social Security benefit is based on is crucial for effective financial planning, allowing you to make informed decisions about your retirement age, savings strategies, and overall financial future. It’s not a simple equation, but rather a sophisticated system that factors in your entire working history, inflation, and your age at which you choose to claim benefits. This article will demystify the core components that determine your Social Security payout, offering insights into how the system works and what you can do to optimize your own financial outlook.

The Foundation: Your Earnings Record and Work History

At the heart of your Social Security benefit calculation lies your individual earnings record. This comprehensive history tracks every dollar you’ve earned in jobs where you paid Social Security taxes throughout your career. The system is designed to provide benefits proportional to your lifetime contributions, meaning those who earn more and work longer typically qualify for higher benefits.

Understanding “Covered Earnings”

Not all income counts towards your Social Security earnings record. Only “covered earnings,” which are wages or self-employment income subject to Social Security taxes (FICA or SECA), are considered. Each year, there’s a maximum amount of earnings subject to Social Security tax, known as the “Social Security Wage Base.” Earnings above this limit are not taxed for Social Security, nor do they count towards increasing your future benefits. This cap is adjusted annually to account for changes in average wages in the U.S. economy. It’s vital to ensure your employers accurately report your earnings to the Social Security Administration (SSA), as any discrepancies could negatively impact your future benefits. Regularly checking your Social Security statement, which you can access online through your My Social Security account, allows you to verify your earnings history and correct any errors. This seemingly minor task can have significant long-term implications for your retirement security.

The Importance of Your Highest 35 Years

The Social Security Administration doesn’t simply average all your covered earnings. Instead, it focuses on your highest-earning years. Specifically, the SSA takes your 35 highest-earning years (adjusted for inflation, as discussed below) to calculate your primary benefit amount. If you have worked for less than 35 years, any years without earnings will be counted as zero, which can significantly lower your overall average. This rule underscores the importance of a consistent and lengthy work history. Individuals who take extended breaks from the workforce, perhaps for childcare or other family responsibilities, may find their benefit amount reduced if they don’t accrue at least 35 years of significant earnings. Conversely, working beyond 35 years can be beneficial, as lower-earning years from early in your career can be replaced by higher-earning years later on, potentially increasing your average.

Averaging Indexed Monthly Earnings (AIME)

Once your highest 35 years of earnings are identified, they are “indexed” to account for changes in average wages over time. This indexing process brings your past earnings up to a comparable current value, ensuring that your benefits reflect the general increase in wages and living standards since you earned those dollars. Without indexing, earnings from decades ago would appear artificially low compared to today’s wages. After indexing, these 35 highest annual earnings are summed up and then divided by 420 (the number of months in 35 years) to arrive at your Average Indexed Monthly Earnings (AIME). The AIME is a crucial intermediate step, representing your average monthly indexed earnings over your career, and it forms the basis for calculating your Primary Insurance Amount (PIA).

Determining Your Primary Insurance Amount (PIA)

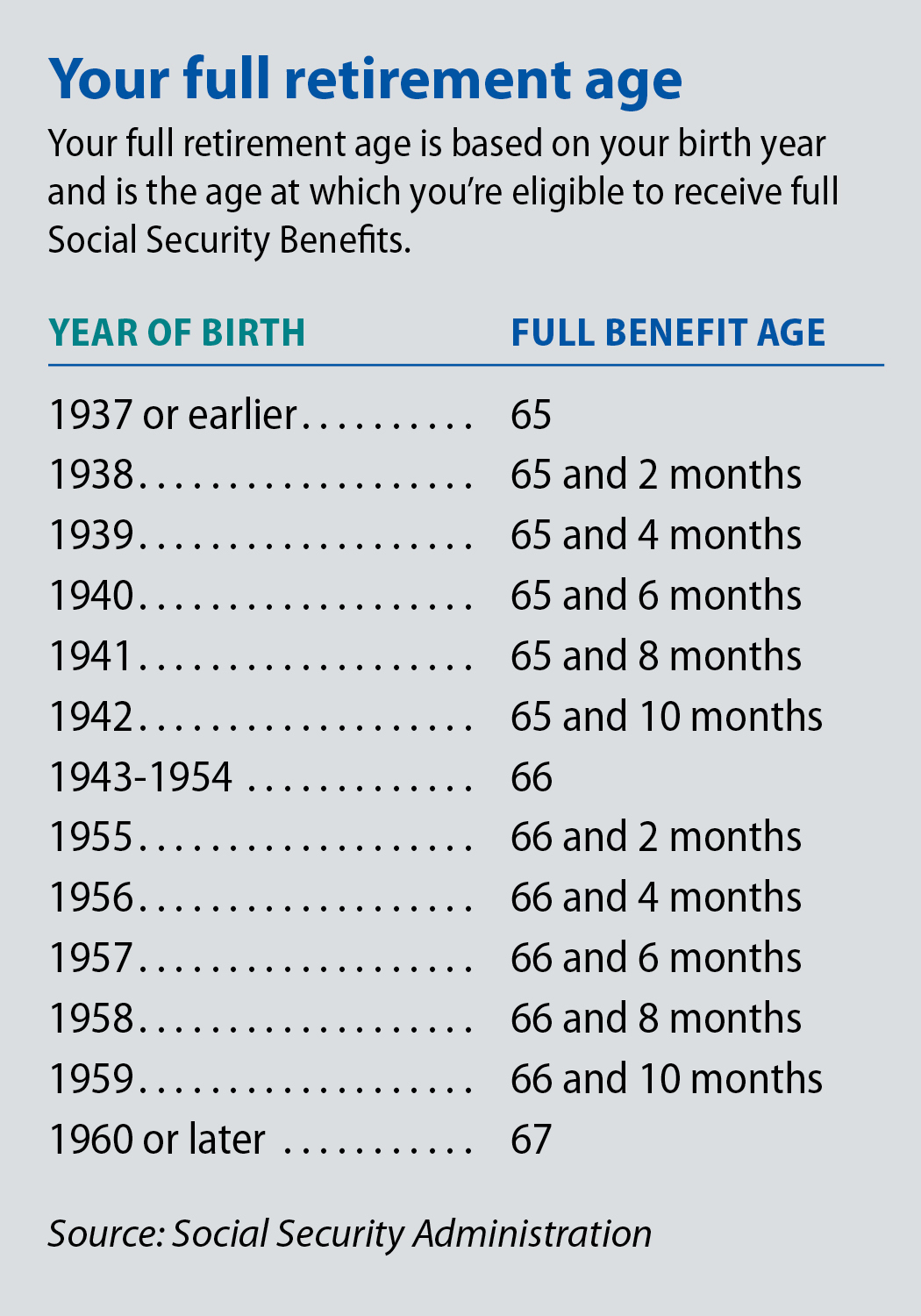

The Primary Insurance Amount (PIA) is the monthly benefit you are entitled to if you claim Social Security benefits at your Full Retirement Age (FRA). The FRA varies depending on your birth year, gradually increasing from age 65 to 67. The calculation of your PIA is not a simple percentage of your AIME; instead, it uses a progressive formula designed to provide a higher percentage of pre-retirement earnings to lower-income workers.

The Bend Points Formula

The SSA uses a progressive formula involving “bend points” to convert your AIME into your PIA. This formula applies different percentage factors to different segments of your AIME, ensuring that Social Security benefits replace a larger proportion of earnings for lower-income workers than for higher-income workers. For example, a higher percentage might be applied to the first segment of your AIME, a lower percentage to the next segment, and an even lower percentage to any AIME above that. These bend points are also indexed annually to keep pace with changes in national average wages, ensuring the formula remains relevant over time. This progressive structure is a fundamental aspect of Social Security’s design, aiming to provide a basic safety net for all covered workers while still reflecting lifetime earnings.

Cost-of-Living Adjustments (COLAs)

Once your PIA is established, your actual benefit amount is further protected against inflation through annual Cost-of-Living Adjustments (COLAs). COLAs are increases in Social Security benefits that are applied almost every year to counteract the effects of inflation and maintain the purchasing power of your benefits. These adjustments are based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). When the CPI-W increases, so do Social Security benefits. This crucial feature ensures that your monthly payments, once started, do not lose significant value over time due to rising costs of living, providing ongoing financial stability throughout your retirement years. COLAs apply not only to your initial benefit but also to benefits for spouses, survivors, and disabled individuals.

The Impact of Early vs. Delayed Claiming

While your PIA is determined by your earnings record and the bend point formula, the actual monthly benefit you receive can be significantly altered by your claiming age. You can begin receiving retirement benefits as early as age 62, but doing so will result in a permanent reduction of your monthly payment. Conversely, if you delay claiming benefits past your Full Retirement Age (FRA) up to age 70, you will earn “delayed retirement credits.” These credits permanently increase your monthly benefit by a certain percentage for each month you delay, up to age 70.

For instance, if your FRA is 67 and you claim at 62, your benefit could be reduced by around 30%. If you wait until age 70, your benefit could be 24-32% higher than your PIA, depending on your birth year. This flexibility allows individuals to tailor their claiming strategy to their personal financial situation, health, and longevity expectations. The decision of when to claim is one of the most critical factors influencing the total amount of Social Security benefits you will receive over your lifetime.

Beyond Retirement: Other Types of Benefits

Social Security is more than just a retirement program. It also provides a vital safety net for families through various other benefit categories, all of which are ultimately based on the primary worker’s earnings record.

Spousal and Survivor Benefits

If you are married or were previously married, your Social Security benefits can extend to your spouse or eligible ex-spouse. Spousal benefits allow a spouse to claim up to 50% of the primary worker’s PIA. If your own retirement benefit based on your earnings record is less than 50% of your spouse’s, you might receive a combination of your own benefit and a spousal benefit to reach that 50% threshold.

Survivor benefits provide financial support to the family of a deceased worker. Eligible survivors, including spouses, children, and dependent parents, can receive monthly benefits. The amount of survivor benefits is also based on the deceased worker’s earnings record, with various rules determining eligibility and the percentage of the deceased worker’s PIA that each survivor can receive. These benefits are a crucial form of life insurance provided by the Social Security system, offering a lifeline during difficult times.

Disability Benefits

Should you become unable to work due to a severe medical condition, Social Security Disability Insurance (SSDI) can provide income replacement. To qualify for SSDI, you must have worked long enough and recently enough under Social Security to earn the required “work credits.” The amount of your disability benefit is also directly linked to your earnings record, calculated in a similar way to retirement benefits. It’s designed to provide financial stability when unforeseen circumstances prevent you from earning a living, serving as a critical safety net for workers and their families.

Benefits for Children

In certain circumstances, dependent children of a retired, disabled, or deceased worker may also be eligible for Social Security benefits. This includes biological children, adopted children, and stepchildren, generally until age 18 (or 19 if still in high school) or at any age if disabled before age 22. These benefits are also derived from the parent’s Social Security earnings record, providing essential support for families.

Maximizing Your Social Security Benefits

Given that Social Security is based on your earnings and claiming decisions, there are strategic steps you can take to potentially maximize your benefits.

Reviewing Your Earnings Statement Regularly

Your Social Security statement is a powerful tool. It provides a detailed summary of your indexed earnings history and estimates your future benefits at different claiming ages (early, full, and delayed). Regularly reviewing this statement, ideally annually, allows you to check for accuracy in your reported earnings. Errors can occur, and if your earnings are underreported, it can negatively impact your future benefits. Correcting these issues while you’re still working is much easier than trying to fix them years into retirement.

Strategic Claiming Age Decisions

As discussed, your claiming age significantly impacts your monthly benefit. The optimal claiming age is a highly personal decision, influenced by factors such as your current health, family longevity, other retirement income sources, and financial needs. If you are in good health and have sufficient savings to cover your expenses, delaying benefits until age 70 can provide the highest possible monthly payment, offering a powerful hedge against inflation and longevity risk. Conversely, if health issues or immediate financial needs dictate, claiming earlier might be the right choice, despite the reduction. Consider consulting a financial advisor to help model various claiming scenarios.

Working While Receiving Benefits

It’s possible to work while receiving Social Security benefits, but there are earnings limits if you haven’t reached your Full Retirement Age (FRA). If your earnings exceed these limits, a portion of your benefits may be withheld. However, these withheld benefits are not lost; they are factored back into your benefit calculation at your FRA, potentially increasing your future monthly payments. Once you reach your FRA, there are no limits on how much you can earn while receiving Social Security benefits. Understanding these rules is essential if you plan to continue working part-time or full-time in early retirement.

Coordinated Financial Planning

Social Security should be viewed as one component of a comprehensive retirement plan. Integrating your expected Social Security benefits with your personal savings (401k, IRAs, taxable accounts), pensions, and other income sources is crucial. A holistic approach allows you to understand how Social Security fits into your overall financial picture, helping you determine how much you need to save independently to achieve your desired retirement lifestyle. For instance, a higher expected Social Security benefit might allow you to save slightly less in personal accounts, while a lower benefit might necessitate more aggressive personal savings.

The Future and Sustainability of Social Security

While the current system is robust, Social Security faces long-term financial challenges due to demographic shifts, specifically increasing longevity and lower birth rates. These trends mean there will be fewer workers contributing per retiree in the future.

Challenges and Proposed Reforms

The Social Security program currently projects that it will be able to pay 100% of promised benefits until around the mid-2030s, after which it would only be able to pay about 80% if no changes are made. Various reforms have been proposed to address this long-term shortfall, including increasing the full retirement age, raising the Social Security payroll tax rate, increasing the wage base subject to taxation, or modifying the benefit formula. These discussions are ongoing, and while the program’s fundamental structure is expected to remain, it’s prudent for individuals to stay informed about potential future adjustments.

Personal Responsibility in Retirement Planning

Regardless of any future changes to Social Security, it’s always wise to assume personal responsibility for your retirement planning. Social Security was never intended to be your sole source of retirement income; rather, it was designed as a foundation. Supplementing your Social Security benefits with personal savings, investments, and other retirement vehicles is essential for achieving true financial independence and security in your later years. Understanding what your Social Security benefits are based on is the first step towards effectively integrating this vital program into your overall financial strategy.

In conclusion, your Social Security benefit is a complex calculation rooted in your lifetime earnings, specifically your 35 highest-earning years, adjusted for inflation. Factors like your claiming age, marital status, and health also play significant roles. By understanding these components and proactively managing your financial plan, you can optimize your Social Security benefits and build a more secure financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.