In an increasingly digital world, peer-to-peer (P2P) payment platforms like Venmo have revolutionized how we send and receive money. From splitting dinner bills with friends to paying rent to a roommate, Venmo has become a ubiquitous tool for quick and convenient transactions. Its user-friendly interface and social features have cemented its place in daily financial interactions for millions. However, beneath the surface of apparent simplicity and often “free” transactions, lies a nuanced fee structure that many users may not fully understand. For individuals and small businesses relying on Venmo, grasping these costs is not just a matter of curiosity but a critical aspect of effective personal and business financial management.

Understanding “what is the Venmo fee” is essential for making informed financial decisions, avoiding unexpected charges, and maximizing the utility of this popular platform. This article will delve deep into Venmo’s various transaction costs, explore the rationale behind them, and provide practical strategies for minimizing fees, all viewed through the lens of sound personal and business finance.

Understanding the Core Venmo Fee Structure

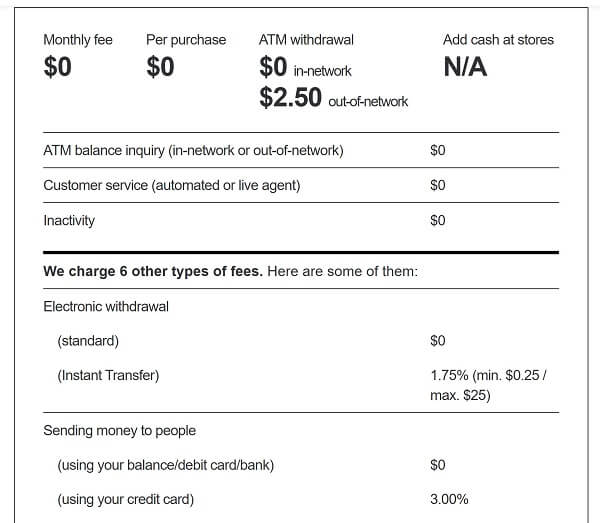

At its heart, Venmo aims to provide a free service for its most common use cases, primarily personal payments funded by linked bank accounts or debit cards. However, several scenarios trigger fees, which are crucial for users to identify and anticipate. These charges are typically a percentage of the transaction amount or a flat fee, reflecting the cost of expediting services or processing certain types of payments.

Personal Payments: The Free and the Fee-Bearing

The cornerstone of Venmo’s appeal is the ability to send money to friends and family without charge. This applies when you fund your payment using your Venmo balance, a linked bank account, or a debit card. This “free” model is what makes Venmo so attractive for casual splitting of expenses and informal transactions.

However, a significant distinction arises when you opt to use a credit card to fund a personal payment. In such cases, Venmo levies a 3% fee on the transaction amount. This fee is standard across most payment processors, as credit card networks charge merchants (in this case, Venmo) for facilitating transactions. Venmo passes this cost onto the user to cover its own processing expenses. From a financial planning perspective, using a credit card for Venmo payments should be considered carefully, especially for larger sums, as the 3% can add up quickly, eroding the convenience benefit. For instance, sending $1000 via credit card would incur a $30 fee – a significant charge for what might otherwise be a free transaction.

Expedited Transfers: The Price of Speed

Once you receive money into your Venmo balance, you have two primary options for moving those funds to your external bank account or debit card: standard transfer and instant transfer.

-

Standard Transfers are free and typically take 1-3 business days to process. This option functions much like a standard ACH transfer, where funds are moved through the banking system without additional charges. For most users, especially those not in immediate need of funds, this is the financially prudent choice. It requires a bit of foresight but ensures that the full amount of your Venmo balance lands in your bank account.

-

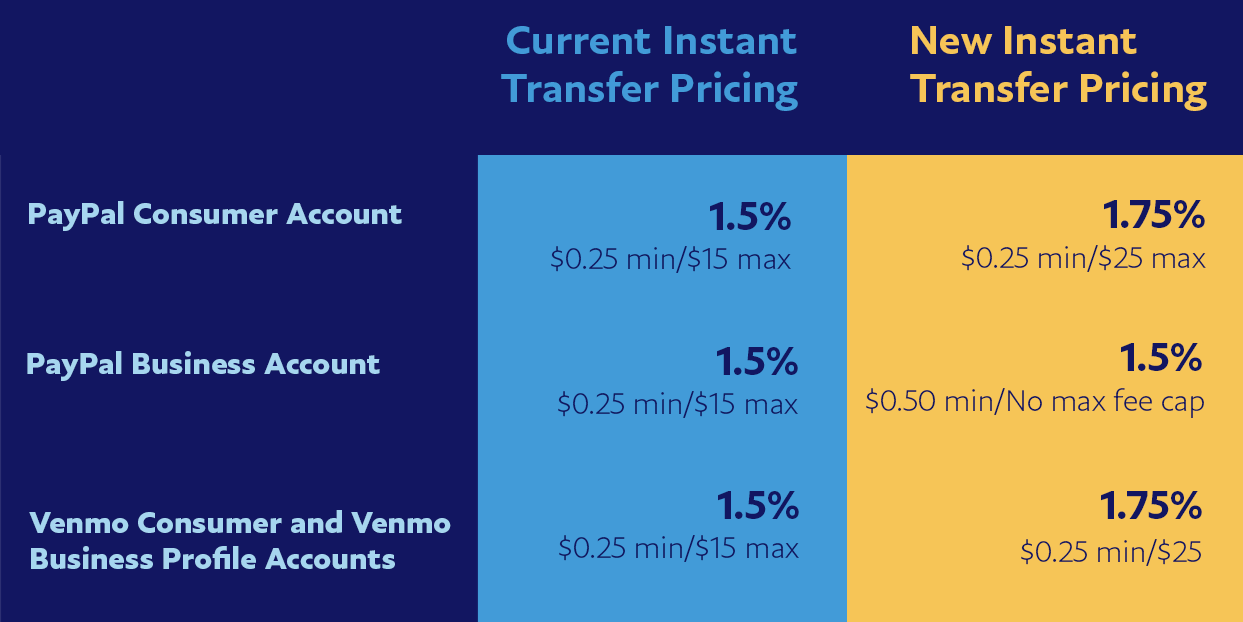

Instant Transfers, as the name suggests, offer immediate access to your funds, usually within minutes, 24/7. This convenience, however, comes with a fee. Venmo charges a 1.75% fee for instant transfers, with a minimum fee of $0.25 and a maximum fee of $25. This fee reflects the value of instant liquidity and the underlying infrastructure required to facilitate such rapid transactions outside of standard banking hours. From a financial perspective, deciding whether to pay for an instant transfer involves weighing the cost against the urgency of accessing the funds. If waiting a few days poses no hardship, opting for the free standard transfer is the financially superior choice. For example, transferring $500 instantly would cost $8.75 (1.75% of $500), while a $10 transfer would still incur the minimum $0.25 fee.

Specialized Services: Cashing Checks and Crypto Purchases

Venmo has expanded its offerings beyond simple P2P payments, introducing features like check cashing and cryptocurrency trading. These specialized services also come with their own fee structures:

-

Cash a Check: Venmo allows users to cash certain types of checks, depositing the funds into their Venmo balance. This service typically incurs a fee, which can vary based on the type of check. For payroll and government checks, the fee is generally 1% of the check amount (minimum $5). For all other approved checks, the fee is 5% (minimum $5). This service can be a convenient option for those without traditional bank accounts or who need immediate access to funds, but the fees should be carefully considered against alternatives like traditional bank deposits, which are usually free.

-

Cryptocurrency Transactions: Venmo also enables users to buy and sell cryptocurrencies directly within the app. These transactions are subject to a fee structure similar to other crypto platforms, typically a percentage of the transaction value. For transactions up to $200, the fee is a flat amount ranging from $0.50 to $2.50. For transactions above $200, the fee is 1.5% of the transaction amount. As with any investment, understanding these transaction costs is vital for calculating potential returns and managing overall investment expenses.

Business Transactions and Seller Fees

While Venmo started as a P2P app, it has increasingly catered to businesses, allowing them to accept payments for goods and services. This expansion introduces a different set of fees, reflecting the commercial nature of these transactions.

Receiving Payments for Goods & Services

For businesses, freelancers, or individuals selling items, Venmo offers Business Profiles, which allow customers to pay for goods and services. When customers pay a Venmo Business Profile or use the “turn on for purchases” option for a personal profile transaction, these transactions are protected by Venmo Purchase Protection. This added security and the commercial nature of the transaction incur a fee for the seller.

The standard fee for receiving payments for goods and services is 1.9% + $0.10 per transaction. This fee structure is comparable to other merchant processing fees and covers the costs associated with payment processing, fraud protection, and customer service for commercial transactions. For small businesses, understanding this fee is crucial for accurate pricing and revenue forecasting. For example, if you sell an item for $50, the fee would be $0.95 + $0.10 = $1.05, meaning you would receive $48.95.

Venmo Debit and Credit Card Related Fees

Venmo also offers its own branded debit and credit cards, which integrate with a user’s Venmo account and provide additional functionalities and potential fees.

-

Venmo Debit Card: This card allows users to spend money directly from their Venmo balance wherever Mastercard is accepted. While many transactions are fee-free, specific charges apply. For instance, ATM withdrawals can incur fees from both Venmo ($2.50 for out-of-network ATMs) and the ATM operator. There might also be a fee for over-the-counter cash withdrawals ($3.00). Foreign transaction fees may apply for international purchases, typically a percentage of the transaction value, when using the card outside the U.S. These are standard fees for many debit cards, but Venmo users should be aware of them to avoid unexpected charges while traveling or making international online purchases.

-

Venmo Credit Card: The Venmo Credit Card operates like a traditional credit card but offers integration with the Venmo app and cashback rewards. While the card itself usually doesn’t have an annual fee, users should be mindful of standard credit card fees such as late payment fees, cash advance fees, and foreign transaction fees. The interest rates (APR) for purchases and cash advances will also apply if balances are not paid in full each month, making responsible credit card management paramount.

Strategies for Minimizing Venmo Fees

Navigating Venmo’s fee landscape can seem daunting, but with a few smart financial habits, users can significantly reduce or even eliminate many of the associated costs. The key lies in understanding which actions trigger fees and choosing alternatives where available.

Leveraging Linked Bank Accounts and Debit Cards

The most straightforward strategy for avoiding fees on Venmo is to consistently use your linked bank account or debit card for sending personal payments. As discussed, these funding sources incur no fees for standard P2P transactions. By contrast, using a credit card for personal payments instantly adds a 3% surcharge. From a budgeting perspective, training yourself to default to bank-funded transactions ensures you keep more of your money. If a credit card is absolutely necessary for points or rewards, the 3% fee must be weighed against the value of those benefits, which for many, will not justify the cost.

Opting for Standard Transfers

For receiving money into your bank account, patience is a virtue that pays off. Choosing the free standard transfer option over the instant transfer can save you 1.75% of your transaction amount. While the allure of immediate access to funds is strong, especially in emergencies, planning ahead can save a significant amount over time. If you receive regular payments via Venmo, even small instant transfer fees can accumulate to a substantial sum annually. Incorporating a slight buffer in your financial planning to allow for 1-3 business day transfers is a sound financial practice.

Understanding Merchant Agreements and Business Profile Use

For individuals selling goods or services, understanding the 1.9% + $0.10 fee for commercial transactions is vital. This fee should be factored into your pricing strategy. When a customer pays through a Venmo Business Profile, or explicitly marks a payment as for “goods and services,” the fee applies. If you are regularly conducting sales, it might be beneficial to compare Venmo’s business fees with other payment processors (e.g., PayPal, Square) to ensure you are using the most cost-effective solution for your specific business needs. Avoid using personal Venmo payments for business transactions simply to avoid fees, as this violates Venmo’s terms of service and deprives both parties of purchase protection. Transparency and compliance are key to long-term financial health.

The Economic Rationale Behind Venmo’s Fee Model

Understanding why Venmo charges certain fees offers insights into the economics of digital payment platforms and helps users appreciate the services they are paying for. These fees are not arbitrary; they are essential for the platform’s sustainability and ability to deliver value.

Covering Operational Costs and Ensuring Profitability

Like any technology company, Venmo incurs substantial operational costs. These include maintaining secure servers, developing new features, marketing, customer support, and complying with complex financial regulations. Fees, particularly on high-value or expedited services, contribute to covering these expenses and ultimately driving profitability for its parent company, PayPal. Without a robust revenue model, Venmo could not continue to innovate and provide its services.

Value Proposition of Instant Gratification

The fee for instant transfers directly reflects the value of speed and convenience. In a fast-paced world, immediate access to funds can be critical for managing cash flow, responding to emergencies, or simply avoiding financial delays. Users who choose instant transfers are essentially paying a premium for this immediate gratification, a common economic principle where convenience commands a higher price.

Credit Card Processing Expenses

The 3% fee for credit card-funded payments is a direct pass-through of the interchange and network fees charged by credit card companies and banks. When you use a credit card, multiple parties are involved in processing that transaction (your bank, the merchant’s bank, Visa/Mastercard/Amex). These entities all take a slice. Venmo, as the facilitator, covers these costs by charging the user, rather than absorbing them, which would be unsustainable for a free-to-use P2P service.

Venmo Fees in the Broader Digital Payment Landscape

Venmo does not operate in a vacuum. It is part of a crowded ecosystem of digital payment services, each with its own fee structures and unique selling propositions. A comparative glance helps put Venmo’s fees into perspective.

A Comparative Glance at Competitors

-

PayPal: As Venmo’s parent company, PayPal offers similar P2P services. Personal payments funded by bank accounts or PayPal balances are generally free. However, like Venmo, PayPal charges a 2.9% + $0.30 fee for goods and services transactions and a similar fee for credit card-funded payments. Instant transfers to bank accounts also incur a 1.75% fee (minimum $0.25, maximum $25). The fee structures are largely consistent, reflecting industry standards for different transaction types.

-

Cash App: Square’s Cash App also provides free P2P transfers using a linked bank account or debit card. Credit card-funded payments for personal use typically incur a 3% fee. Instant deposits to a debit card are subject to a 0.5% to 1.75% fee, making it competitive with Venmo. Business transactions on Cash App typically carry a 2.75% fee, which is slightly higher than Venmo’s 1.9% + $0.10.

-

Zelle: Zelle, integrated into many banking apps, stands out by offering entirely free P2P transfers from bank account to bank account, typically instant, with no fees for sending or receiving money. The key difference is that Zelle only works with linked bank accounts and does not support credit card funding or an in-app balance like Venmo or Cash App. This makes Zelle a purely bank-centric free transfer service, but it lacks some of the social features and specialized services (like crypto or business profiles) of its competitors.

This comparison highlights that Venmo’s fee structure is generally in line with industry norms for the types of services it offers, particularly concerning credit card processing and instant transfers. Zelle serves a specific niche for purely free, fast bank-to-bank transfers, while platforms like Venmo and Cash App provide more comprehensive features at a slight cost for specific functionalities.

Future Trends in Digital Payment Fee Structures

The digital payment landscape is constantly evolving. As competition intensifies and new technologies emerge, fee structures may shift. We might see:

- Increased focus on subscription models: Platforms could offer premium tiers with reduced or waived fees for a monthly subscription.

- Dynamic pricing based on user behavior: Fees could be adjusted based on transaction volume, loyalty, or other factors.

- Integration with broader financial services: As platforms become “super apps,” fees might be bundled or offset by other financial products like lending or investing.

- Regulatory changes: Governments and financial bodies may impose new regulations that impact how fees are charged or disclosed.

Staying informed about these trends is crucial for users to continue making financially astute decisions in their digital payment choices.

Conclusion

Understanding “what is the Venmo fee” is more than just knowing a few percentages; it’s about grasping the underlying economics of digital payments and making conscious choices that align with your financial goals. While Venmo offers a remarkably convenient and often free service for personal transactions, specific actions—like using a credit card, opting for instant transfers, or conducting business transactions—will incur costs.

By leveraging free funding sources, choosing standard transfers, and transparently managing business payments, users can effectively minimize their Venmo expenses. For businesses, accurately factoring in Venmo’s merchant fees into pricing is vital for profitability. In a competitive market where alternatives like Zelle, PayPal, and Cash App each present their own cost-benefit analyses, a clear understanding of Venmo’s fee structure empowers users to make the most financially sound decisions for their personal and business finances. As digital payments continue to evolve, staying informed about these costs remains a cornerstone of intelligent money management in the modern age.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.