In the landscape of global finance, few names carry as much weight, or command as much respect, as Vanguard. To the average person, Vanguard is a website where they check their 401(k) or a name on a monthly brokerage statement. To the seasoned investor, however, it represents a revolutionary shift in how wealth is built and managed.

Founded in 1975 by John C. “Jack” Bogle, The Vanguard Group has grown from a fledgling experiment in Pennsylvania to one of the world’s largest investment management companies, currently overseeing trillions of dollars in global assets. But to truly understand “what” Vanguard is, one must look beyond the balance sheets and explore the philosophy, the unique corporate structure, and the democratization of investing that the firm pioneered.

The Philosophy of Low-Cost Investing: The Bogle Legacy

The story of Vanguard is inseparable from the story of Jack Bogle. Before Vanguard, the investment world was dominated by high-cost, actively managed funds. Wall Street “experts” promised to beat the market for a steep fee—often taking a significant percentage of an investor’s returns regardless of performance. Bogle challenged this paradigm with a radical proposition: if you can’t beat the market, why not just own the whole market at the lowest possible cost?

The Invention of the Index Fund

In 1976, Vanguard launched the first-ever index mutual fund for individual investors, now known as the Vanguard 500 Index Fund. At the time, critics labeled it “Bogle’s Folly,” arguing that settling for “average” market returns was un-American. However, Bogle understood a fundamental mathematical truth: in the long run, active managers as a group must underperform the market after accounting for their high fees. By creating a fund that simply tracked the S&P 500, Vanguard allowed investors to capture the growth of the American economy without losing their gains to administrative costs and trading commissions.

Jack Bogle’s “Common Sense” Approach

The “Boglehead” philosophy, which has since become a global movement, rests on the pillar of common-sense investing. This approach emphasizes long-term thinking, broad diversification, and, most importantly, cost-minimization. Bogle famously remarked that in investing, “you get what you don’t pay for.” By keeping “expense ratios” (the annual fee investors pay) near zero, Vanguard ensures that a larger portion of compound interest stays in the investor’s pocket rather than the fund manager’s.

Understanding the Unique Vanguard Ownership Structure

What truly sets Vanguard apart from competitors like Fidelity, BlackRock, or Charles Schwab is not just its products, but its DNA. Most financial institutions are either publicly traded (beholden to shareholders) or privately held (beholden to a group of owners). This creates an inherent conflict of interest: the firm wants to maximize its own profits, while the clients want to maximize their investment returns.

Why Being Client-Owned Matters

Vanguard operates under a unique “mutuality” structure. The company is owned by its member funds, and those funds, in turn, are owned by the investors who buy them. In short, if you own a Vanguard fund, you are a part-owner of the company. This structural innovation eliminates the conflict of interest mentioned above. Because the “shareholders” of the company and the “clients” of the company are the same people, any profits made by the firm are reinvested into the business to lower the cost of investing further.

The Alignment of Interests

This alignment of interests has triggered what is known as the “Vanguard Effect.” Over the decades, as Vanguard grew larger and its economies of scale increased, it systematically lowered its fees. This forced the rest of the financial industry to lower their prices just to remain competitive. Today’s world of zero-commission trades and ultra-low-cost ETFs is a direct result of the pressure Vanguard’s ownership structure put on the traditional Wall Street model.

Vanguard’s Key Investment Vehicles: Mutual Funds and ETFs

Vanguard offers a vast array of financial products, but they are primarily recognized for their mastery of two specific vehicles: Mutual Funds and Exchange-Traded Funds (ETFs). Understanding the distinction between these is crucial for any investor looking to utilize the Vanguard platform.

Diversification Through Mutual Funds

Vanguard’s traditional mutual funds allow investors to pool their money into a diversified basket of stocks or bonds. One of their most popular offerings is the Total Stock Market Index Fund (VTSAX). This single fund holds thousands of companies, providing instant diversification. Mutual funds are typically traded once per day after the market closes and are ideal for long-term investors who use automated monthly contributions.

The Rise of Vanguard ETFs

In recent years, Vanguard has become a dominant force in the ETF market. ETFs, such as the Vanguard S&P 500 ETF (VOO) or the Vanguard Total Bond Market ETF (BND), function similarly to index funds but trade like stocks on an exchange. They offer high liquidity and, in many cases, even lower entry points than mutual funds. Vanguard’s “patented” ETF structure (where the ETF is a share class of the mutual fund) allows for unique tax efficiencies that are highly prized by investors in taxable brokerage accounts.

Comparing Expense Ratios and Tax Efficiency

When people ask “What is the Vanguard advantage?” the answer is usually the expense ratio. While some active funds in the industry charge 1.00% or more annually, many Vanguard index funds charge as little as 0.03%. On a $100,000 portfolio, that is the difference between paying $1,000 a year versus just $30. Over thirty years, that difference can amount to hundreds of thousands of dollars in lost wealth due to the erosion of compounding.

How to Build a Vanguard Portfolio

Investing with Vanguard is often praised for its simplicity. While the firm offers thousands of options, the most successful Vanguard investors often adhere to a “less is more” strategy. Building a portfolio doesn’t require a degree in finance; it requires discipline and a basic understanding of asset allocation.

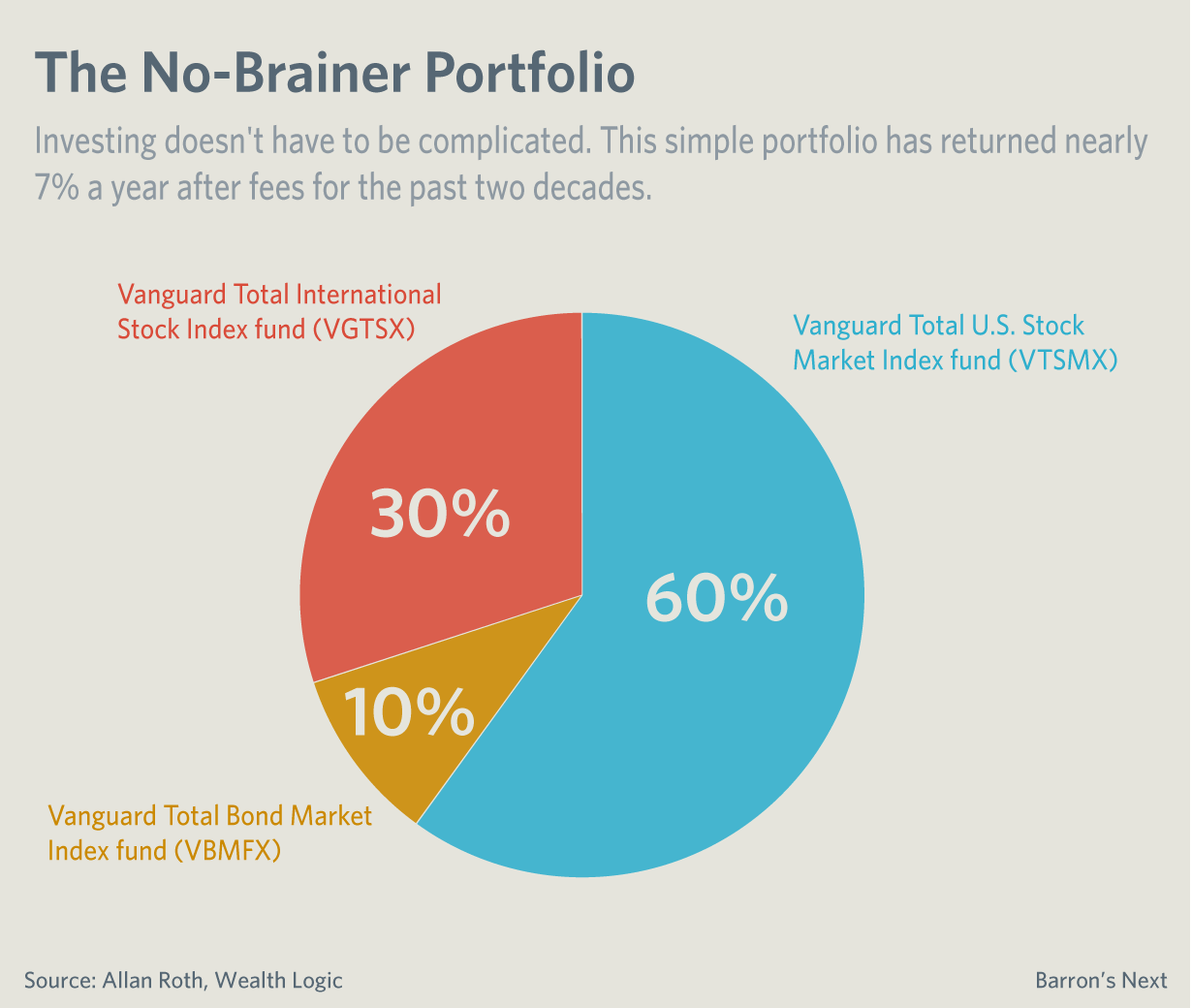

The Three-Fund Portfolio Strategy

Popularized by the Bogleheads community, the “Three-Fund Portfolio” is a hallmark of the Vanguard way. It consists of:

- A Total Domestic Stock Market Index Fund (covering all U.S. companies).

- A Total International Stock Market Index Fund (covering non-U.S. companies).

- A Total Bond Market Index Fund (providing stability and income).

By holding just these three funds, an investor owns a piece of nearly every publicly traded company in the world and a diversified slice of the global debt market.

Target Retirement Funds for Hands-Off Investors

For those who prefer a “set it and forget it” approach, Vanguard’s Target Retirement Funds (also known as Target Date Funds) are an industry standard. The investor simply chooses the year they plan to retire (e.g., 2055), and Vanguard automatically manages the asset allocation. As the investor gets older, the fund gradually shifts from aggressive stocks to more conservative bonds, ensuring the portfolio is appropriately risked for the investor’s stage in life.

The Future of Vanguard in a Digital Age

As we move deeper into the 21st century, Vanguard is evolving to meet the needs of a new generation of digital-native investors. While the core philosophy remains unchanged, the delivery of their services is undergoing a significant transformation.

Personal Advisor Services and Fintech Integration

Recognizing that some investors want more than just a platform to buy funds, Vanguard has expanded into “Personal Advisor Services” (PAS). This hybrid model combines sophisticated algorithmic rebalancing with access to human financial planners. It represents a “middle path” between the high cost of traditional wealth management and the DIY nature of early index investing. Furthermore, Vanguard has invested heavily in its mobile app and web interface, aiming to make complex financial planning accessible via a smartphone.

Navigating Global Market Volatility

As global markets become more interconnected and volatile, Vanguard’s emphasis on “staying the course” is more relevant than ever. In an era of “meme stocks” and crypto-volatility, Vanguard stands as a bastion of the slow-and-steady approach. The firm continues to advocate for the “Investor’s Manifesto”: invest early, invest often, diversify broadly, and ignore the noise of the daily news cycle.

In conclusion, Vanguard is more than just a financial services company; it is a structural anomaly in the world of capitalism that favors the individual over the institution. By prioritizing low costs, client ownership, and long-term index-based strategies, Vanguard has transformed investing from a “rich man’s game” into a powerful tool for the masses to achieve financial independence. Whether you are a young professional starting your first IRA or a retiree preserving your nest egg, understanding the Vanguard model is essential to mastering the world of personal finance.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.