In an increasingly globalized world, where borders are becoming less relevant for commerce and personal connections, the ability to transfer money across countries seamlessly is paramount. Whether you’re a business owner paying international suppliers, an individual sending funds to family abroad, or receiving payments from overseas clients, understanding the mechanics of international money transfers is crucial. At the heart of this intricate global financial network lies the SWIFT code – a standardized identifier that ensures funds reach their intended destination. For customers of one of the largest financial institutions in the United States, JPMorgan Chase Bank, understanding their SWIFT code is a frequent necessity.

This comprehensive guide will demystify SWIFT codes, specifically focusing on those associated with Chase Bank. We’ll delve into why these codes are indispensable, how to locate the correct one for your transactions, and best practices for navigating international money transfers with confidence and security through Chase.

Understanding SWIFT Codes: The Global Language of Finance

The SWIFT code is more than just a series of letters and numbers; it’s a critical financial tool that facilitates the smooth and secure movement of capital across international borders. Without it, the global financial system would face significant hurdles in identifying banks and processing cross-border payments efficiently.

What Exactly is a SWIFT Code?

A SWIFT code, also known as a Bank Identifier Code (BIC), is a standard format of Business Identifier Codes approved by the International Organization for Standardization (ISO). It is used to identify banks and financial institutions globally and is a critical component for international wire transfers. The acronym SWIFT stands for the Society for Worldwide Interbank Financial Telecommunication, the organization that manages and registers these codes. Essentially, a SWIFT code acts like a universal address for financial institutions, ensuring that your money is routed to the correct bank, branch, and country.

Why SWIFT Codes are Essential for Global Finance

Imagine trying to send a letter to a specific building in a foreign city without knowing its street address or postal code. The chances of it reaching its destination would be slim to none. SWIFT codes serve a similar purpose in the financial world. They provide a unique identifier that removes ambiguity and prevents errors in international transactions. When you initiate an international wire transfer, the sending bank uses the recipient bank’s SWIFT code to determine the exact institution and often the specific branch where the funds should be directed. This standardization is vital for:

- Accuracy: Ensuring funds go to the correct bank.

- Efficiency: Speeding up the processing of international payments.

- Security: Reducing the risk of fraud and misdirection of funds.

- Compliance: Meeting regulatory requirements for international financial transactions.

Decoding the SWIFT Code Structure

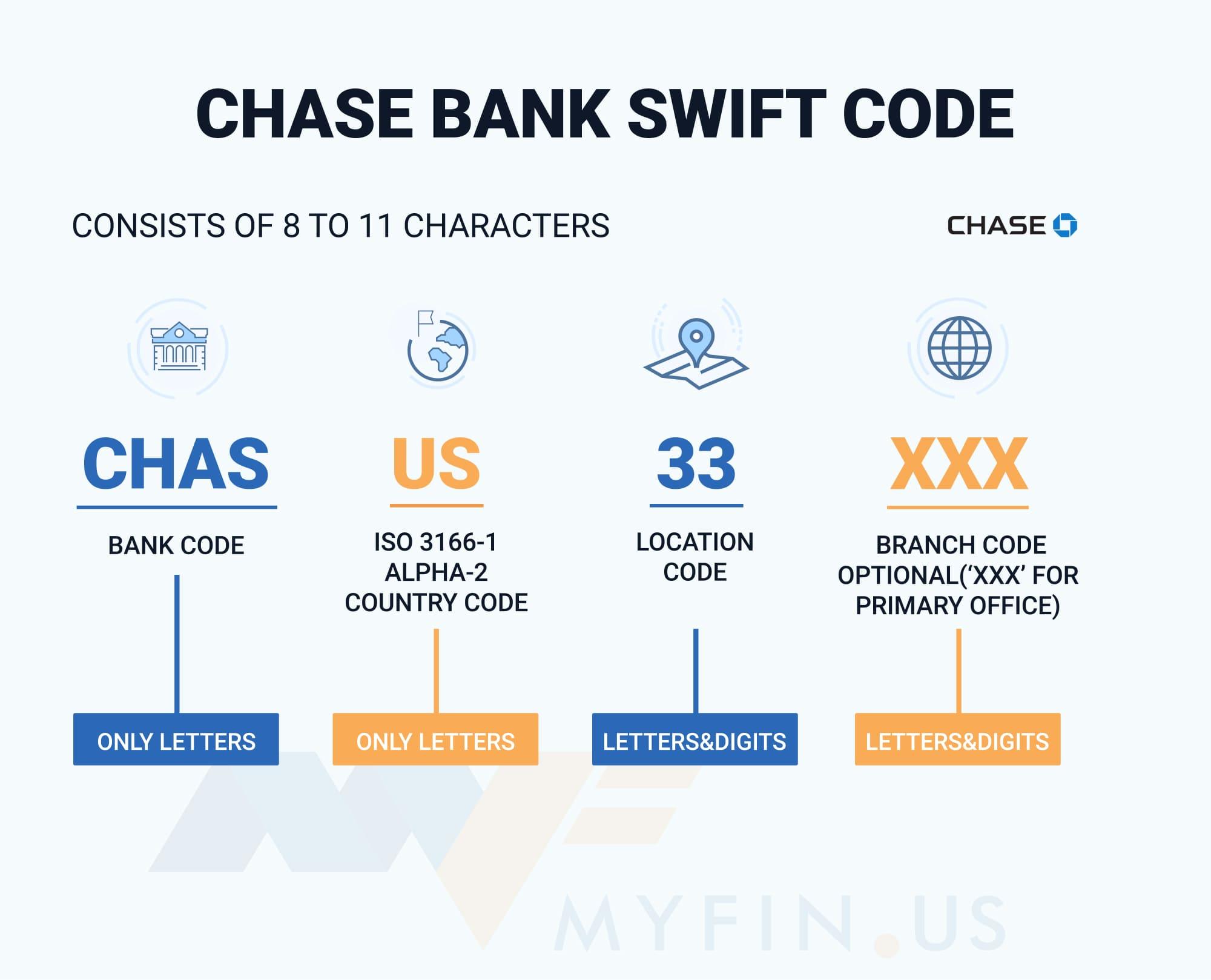

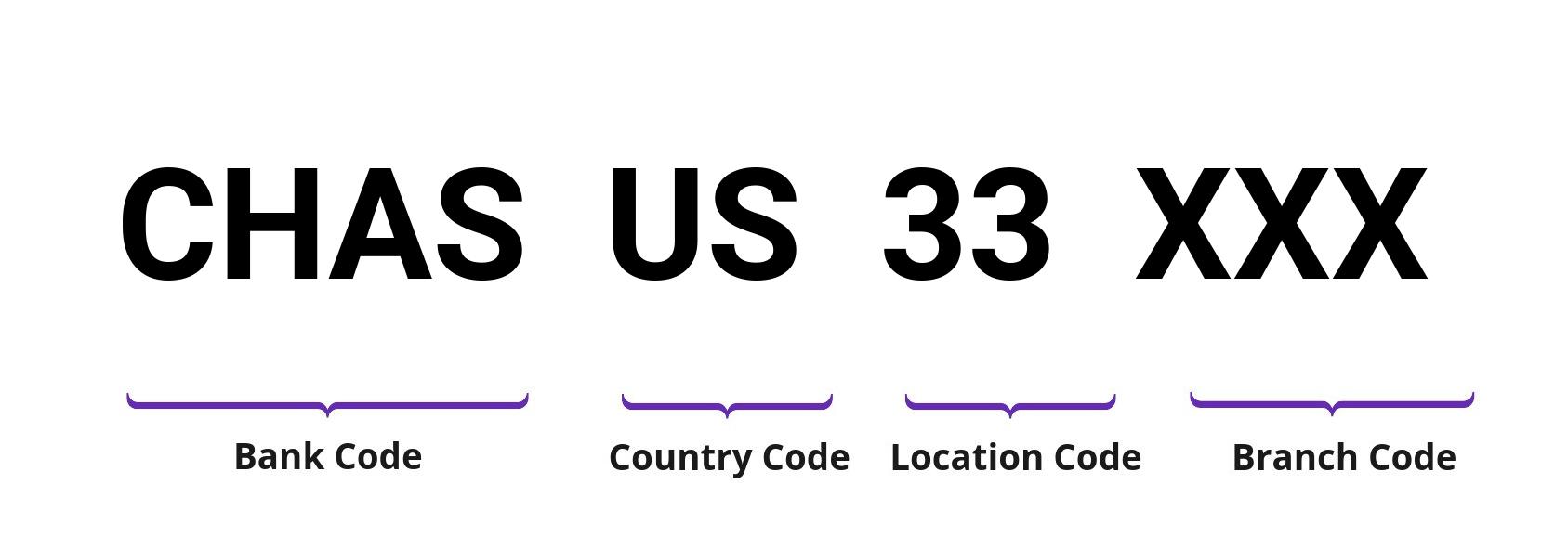

A SWIFT code is typically 8 or 11 characters long, structured in a way that provides specific information about the financial institution:

- AAAA (Bank Code): The first four characters represent the bank code, identifying the financial institution. For Chase, this is typically “JPMR”.

- BB (Country Code): The next two characters denote the country where the bank is located, following the ISO 3166-1 alpha-2 standard. For the United States, this is “US”.

- CC (Location Code): The subsequent two characters represent the location code of the bank’s head office or a primary branch. These can be letters or numbers. For Chase, this is often “33”.

- DDD (Branch Code – Optional): The last three characters are optional and specify a particular branch of the bank. If omitted, the code refers to the bank’s primary office. For many international transactions with Chase, the branch code is not always necessary, defaulting to the main branch.

Therefore, a common SWIFT code for Chase Bank might look like JPMRUS33.

Locating Chase Bank’s SWIFT Code for Your Transactions

For Chase Bank, the primary SWIFT code used for most international wire transfers is widely known. However, it’s always prudent to confirm the exact code required for your specific transaction, as sometimes variations can occur depending on the type of transaction or the specific branch involved, although this is less common for major banks like Chase.

The Primary SWIFT Code for Chase Bank (JPMORGAN CHASE BANK, N.A.)

The most commonly used and accepted SWIFT code for JPMORGAN CHASE BANK, N.A., which covers the vast majority of international transfers to and from its U.S. accounts, is:

JPMRUS33

This code identifies JPMorgan Chase Bank’s main operations in the United States. When you provide this code to a sender, it directs the funds to Chase’s central processing hub for international wires, from where they are then routed to your specific Chase account using your account number.

How to Verify the Correct Code for Your Specific Needs

While JPMRUS33 is the standard, verifying is a good financial practice. There are several ways to confirm the correct SWIFT code:

- Chase Online Banking: Log in to your Chase online banking portal. Often, information regarding international transfers, including the bank’s SWIFT code, can be found in the “Help” or “FAQs” section related to wire transfers.

- Chase Bank Statements: Sometimes, SWIFT or BIC codes are printed on bank statements, particularly for business accounts that regularly conduct international transactions.

- Contact Chase Customer Service: The most reliable method is to directly contact Chase customer service. They can provide the exact SWIFT code applicable to your account and the specific type of international transaction you intend to make.

- Visit a Chase Branch: A banking representative at your local Chase branch can also assist you with finding the correct SWIFT code and any other necessary details for your international transfer.

It’s crucial to obtain this information directly from Chase or a trusted source to avoid delays or misdirection of funds.

Common Scenarios Requiring Chase’s SWIFT Code

You will typically need Chase’s SWIFT code in the following situations:

- Receiving an International Wire Transfer: If someone from another country is sending money to your Chase account, you will need to provide them with Chase’s SWIFT code (JPMRUS33), your full account number, and your name and address as they appear on your account.

- Sending Money from an Overseas Account to Your Chase Account: If you have an account with a foreign bank and wish to transfer funds to your Chase account, you’ll need to input Chase’s SWIFT code during the transfer process.

- Certain International Payment Platforms: Some international payment services or third-party money transfer providers might require the SWIFT code when linking your Chase account for receiving payments.

Navigating International Money Transfers with Chase

Once you have the correct SWIFT code, the next step is understanding how to effectively send and receive money internationally using Chase’s services. This involves knowing the various channels, potential costs, and processing times.

Sending Money Internationally Through Chase

Chase offers several ways to send international wire transfers:

- Chase Online Banking: For personal and business customers, initiating an international wire transfer through Chase Online or the Chase Mobile app is a convenient option. You will typically navigate to the “Pay & Transfer” section, select “Wire money,” and follow the prompts to input the recipient’s bank details, including their SWIFT code, account number, name, and address.

- Chase Branches: You can visit any Chase bank branch to send an international wire transfer. A banker will assist you with filling out the necessary forms and verifying the details. This option can be particularly useful for first-time senders or for high-value transactions where in-person assistance is preferred.

- Chase Business Online / Commercial Banking: For larger businesses, Chase offers more sophisticated online platforms and treasury services tailored for frequent and high-volume international payments, often with dedicated support and potentially better foreign exchange rates.

When sending money, always double-check all recipient details, including their SWIFT/BIC code, account number (IBAN for European countries), full name, and address. A single error can lead to significant delays or even loss of funds.

Receiving Funds from Abroad via Chase

To receive an international wire transfer into your Chase account, you will need to provide the sender with the following information:

- Bank Name: JPMorgan Chase Bank, N.A.

- SWIFT Code: JPMRUS33

- Your Full Name: As it appears on your Chase account.

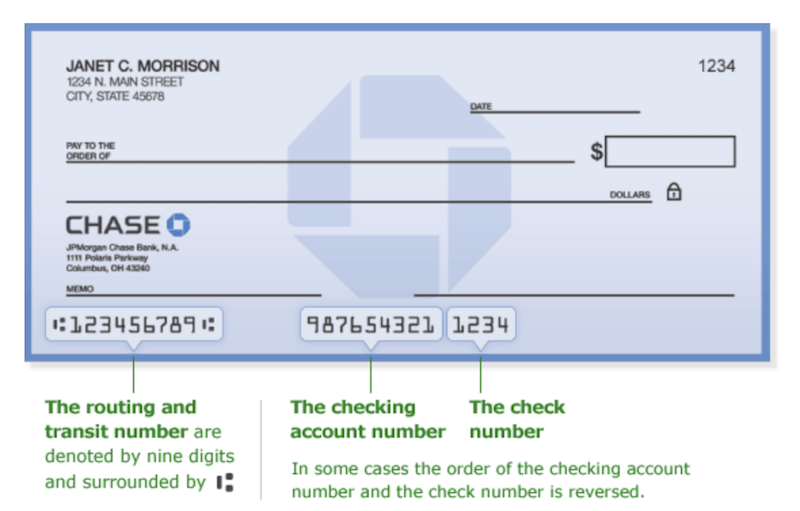

- Your Full Account Number: The 9-digit routing number for domestic transfers is not typically needed for international SWIFT transfers, but your full account number is crucial.

- Your Address: As registered with Chase.

It’s important to provide all this information accurately to the sender to ensure the funds arrive without issue. Chase does not charge a fee for receiving international wire transfers, but the sender’s bank or intermediary banks may impose their own fees, which could be deducted from the transferred amount.

Fees, Exchange Rates, and Transfer Limits

International money transfers involve several financial considerations:

- Fees: Chase charges fees for sending international wire transfers. These fees can vary depending on whether the transfer is in U.S. dollars or a foreign currency, and whether it’s sent online or in-branch. Always review the current fee schedule on Chase’s website or inquire with a representative.

- Exchange Rates: When sending money in a foreign currency, Chase applies an exchange rate. This rate can include a markup over the interbank exchange rate, which is how banks profit from currency conversions. It’s advisable to compare Chase’s exchange rates with other services if the exchange rate is a significant concern for your transaction.

- Transfer Limits: Chase may impose daily or transaction limits on international wire transfers, especially when initiated online. These limits can vary based on your account type, relationship with the bank, and security protocols. For larger transfers, you might need to visit a branch or contact customer service to arrange them.

- Intermediary Bank Fees: For some international transfers, particularly to less common destinations or currencies, intermediary (correspondent) banks might be involved. Each intermediary bank can deduct its own processing fee, which can reduce the final amount received by the beneficiary.

Best Practices for Secure and Efficient International Transfers

Navigating international transfers requires diligence. Adhering to best practices can save you time, money, and potential headaches.

Double-Checking Details: Preventing Costly Errors

This cannot be stressed enough: verify every single piece of information. An incorrect digit in an account number or a misplaced letter in a SWIFT code can cause funds to be delayed, returned (often with fees), or, in rare cases, sent to the wrong recipient. When receiving information from a sender or providing it to a recipient, ask them to double-check their bank’s guidelines. For transfers to European countries, ensure you have the correct International Bank Account Number (IBAN), which is typically a longer alphanumeric code that incorporates the bank code, country code, and account number.

Understanding Processing Times

International wire transfers are generally faster than older methods like checks, but they are not instantaneous. While some transfers might complete within 24-48 hours, others can take 3-5 business days or even longer, depending on the destination country, currency, time zones, banking holidays, and compliance checks. Banks typically process wires during specific operating hours, and transfers initiated outside these hours might not begin processing until the next business day. Always factor in these processing times, especially for time-sensitive payments.

Alternatives to Traditional SWIFT Transfers

While SWIFT transfers are the standard for bank-to-bank international payments, it’s worth noting that other financial tools and services exist for international money movement. These include:

- Remittance Services: Platforms like Western Union or MoneyGram, often preferred for cash pickups or transfers to individuals without bank accounts.

- Online Money Transfer Services: Digital-first platforms such as Wise (formerly TransferWise), Xoom, or Remitly often offer competitive exchange rates and lower fees for certain corridors, and can be faster for smaller personal transfers.

- Cryptocurrency: While volatile, digital currencies offer a decentralized way to transfer value across borders, though their regulatory status and ease of use for everyday transactions are still evolving.

These alternatives can sometimes be more cost-effective or faster for specific use cases, but for robust, secure, and large-value bank-to-bank transactions, the SWIFT network remains the go-to standard used by institutions like Chase.

Beyond the Code: Maximizing Your International Banking Experience with Chase

Understanding the SWIFT code is the first step, but a deeper knowledge of the broader international banking landscape can further enhance your financial management.

The Role of Correspondent Banks

When you send money internationally, especially to less common destinations or in specific currencies, your bank (Chase) might not have a direct relationship with the recipient’s bank. In such cases, the transfer will go through one or more intermediary banks, known as correspondent banks. These banks facilitate the transfer between institutions that don’t have direct clearing relationships. While this process is largely invisible to the customer, it’s why some transfers involve additional fees (deducted by these intermediaries) and can take slightly longer. Chase, as a global bank, has an extensive network of correspondent banks, which helps streamline these complex paths.

Protecting Yourself from Fraud

International transactions can sometimes be targets for fraudsters. Always be suspicious of unsolicited requests for wire transfers, especially from individuals claiming to be government officials, lottery organizers, or distant relatives in distress. Only send money to people and businesses you know and trust. Chase employs robust security measures, but ultimate responsibility for verifying the recipient’s legitimacy lies with the sender. If you suspect fraud, contact Chase immediately.

Leveraging Chase’s Resources for International Banking

As a Chase customer, you have access to a wealth of resources for international finance. Beyond standard wire transfers, Chase offers foreign currency accounts for businesses, treasury management solutions, foreign exchange services, and expert advice for complex international financial needs. Familiarizing yourself with these offerings can help both individuals and businesses optimize their global financial operations.

In conclusion, the SWIFT code for Chase Bank, primarily JPMRUS33, is a vital piece of information for anyone involved in international money transfers. By understanding its purpose, how to use it correctly, and the broader context of international banking best practices, you can ensure your funds are sent and received securely, efficiently, and without unnecessary complications through Chase. This knowledge empowers you to navigate the global financial landscape with confidence.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.