The landscape of American personal finance underwent a seismic shift with the introduction of the Saving on a Valuable Education (SAVE) plan. For millions of borrowers, student loan debt has long been a primary obstacle to achieving traditional financial milestones—such as purchasing a home, investing in the stock market, or building a robust emergency fund. The SAVE plan, introduced by the U.S. Department of Education, is not merely a technical adjustment to repayment terms; it is a fundamental reimagining of how federal student debt interacts with an individual’s financial health.

As an income-driven repayment (IDR) plan, SAVE replaces the older Revised Pay As You Earn (REPAYE) plan, offering more generous terms that prioritize the borrower’s ability to cover essential living expenses before calculating loan payments. In the following sections, we will explore the mechanics, benefits, and strategic financial implications of this plan.

The Core Mechanics of the SAVE Plan

To understand the SAVE plan, one must first understand the concept of discretionary income. In the context of federal student loans, discretionary income is the portion of your earnings that the government deems “extra” after you have paid for basic necessities. The SAVE plan changes the math of this calculation in favor of the borrower more than any plan in history.

The Shift from REPAYE to SAVE

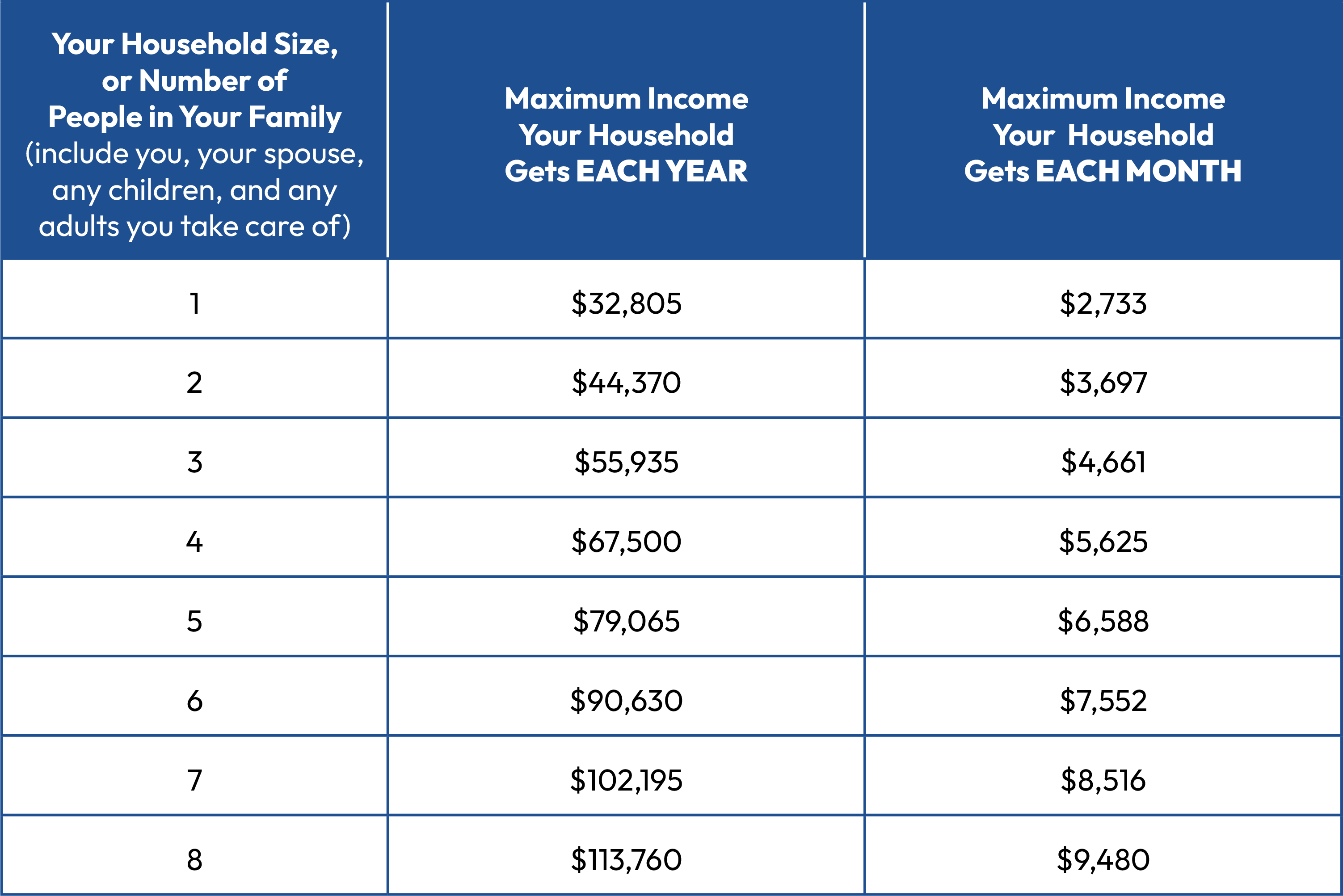

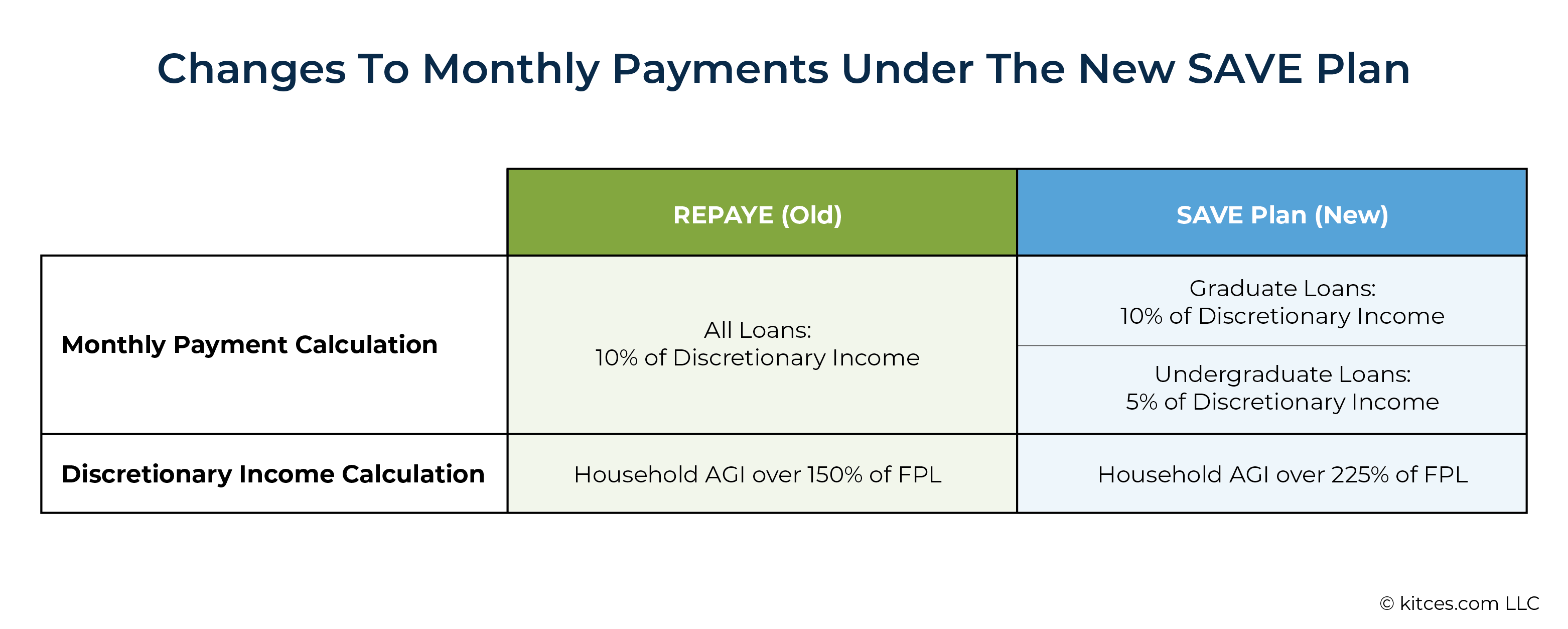

Before the SAVE plan, the REPAYE plan was the standard for most borrowers seeking income-based relief. Under REPAYE, discretionary income was defined as anything earned above 150% of the federal poverty guideline. The SAVE plan increases this threshold to 225%. This means a significantly larger portion of a borrower’s income is protected from loan payments. For a single borrower, this equates to roughly $32,800 of annual income that is completely shielded from repayment calculations. If you earn less than this amount, your monthly payment is effectively $0.

Eligibility and Enrollment Criteria

The SAVE plan is designed to be inclusive. Most borrowers with Direct subsidized and unsubsidized loans, as well as Direct PLUS loans made to graduate or professional students, are eligible. While Parent PLUS loans do not qualify directly, they may become eligible through a “double consolidation” loophole, though this requires careful financial maneuvering. For most young professionals and mid-career borrowers, the transition is seamless; those already enrolled in the REPAYE plan were automatically transitioned into the SAVE plan.

The Calculation of Monthly Payments

The SAVE plan distinguishes between undergraduate and graduate debt. For undergraduate loans, the payment is capped at 5% of discretionary income. For graduate loans, the cap is 10%. Borrowers with a mix of both pay a weighted average between 5% and 10%. This distinction is vital for financial planning, as it allows undergraduate borrowers to retain a larger share of their take-home pay for other wealth-building activities.

Unprecedented Benefits: Beyond Low Monthly Payments

The SAVE plan offers more than just lower monthly bills; it addresses the “interest trap” that has plagued borrowers for decades. Historically, many borrowers on IDR plans saw their balances grow even while making payments because their monthly installments didn’t cover the accruing interest. The SAVE plan eliminates this phenomenon.

The End of Negative Amortization

The most revolutionary feature of the SAVE plan is the interest subsidy. If a borrower’s calculated monthly payment is less than the interest that accrued that month, the government waives the remaining interest. For example, if $100 in interest accumulates but your SAVE payment is only $40, the remaining $60 is not added to your balance. This ensures that as long as you remain current on your SAVE payments, your loan balance will never grow. From a personal finance perspective, this is a massive win, as it prevents debt from spiraling out of control.

Accelerated Paths to Forgiveness

The SAVE plan also introduces a faster timeline for debt discharge for those with smaller initial balances. Borrowers who originally took out $12,000 or less can have their remaining debt forgiven after just 10 years of payments, rather than the standard 20 or 25 years. For every $1,000 borrowed above $12,000, one additional year of payments is required, up to a maximum cap. This creates a significant incentive for community college students and those who utilized smaller loans to enter the workforce without a thirty-year debt shadow.

Protection During Economic Volatility

Because the SAVE plan is tied directly to income, it serves as a built-in financial safety net. In the event of job loss or a reduction in hours, a borrower’s payment can drop to $0 automatically upon recertification. These $0 “payments” still count toward the total number of months required for eventual loan forgiveness, providing both immediate cash flow relief and long-term progress toward debt elimination.

Strategic Financial Planning with the SAVE Plan

In the niche of “Money,” the SAVE plan is more than a debt-repayment tool—it is a capital allocation tool. By reducing the outflow of cash toward low-interest or subsidized federal debt, borrowers can redirect their capital toward higher-yield opportunities.

Leveraging Discretionary Savings for Investing

When a borrower switches to the SAVE plan and reduces their monthly payment from $400 to $100, they have “found” $300 in monthly cash flow. In a high-inflation or high-interest-rate environment, that $300 might be better served in a High-Yield Savings Account (HYSA) or a diversified index fund. By paying the minimum on student loans (without the fear of the balance growing), a borrower can effectively use the government’s subsidy to fund their own retirement accounts, such as a Roth IRA or 401(k).

Comparing SAVE with Standard Repayment

While SAVE is beneficial for many, it is not a “one size fits all” solution. High-income earners with relatively low debt might find that the 10% discretionary income calculation actually results in a higher payment than the 10-year Standard Repayment Plan. Furthermore, those who wish to be debt-free as quickly as possible may still choose to overpay. However, from a mathematical standpoint, if your loan interest is being subsidized and you can earn 5% in a savings account, there is a strong “Money” logic for staying on the SAVE plan and keeping your cash liquid.

Tax Implications and Long-Term Forgiveness

One must consider the “tax bomb”—the potential tax liability on the forgiven amount at the end of the 20- or 25-year period. While current federal law (under the American Rescue Plan) exempts student loan forgiveness from federal taxes through 2025, it is unclear if this will be extended. Financial planning within the SAVE niche requires preparing for a potential tax bill decades down the line by setting aside a small “tax sinking fund” today.

Enrollment, Recertification, and Portfolio Management

Managing your student loans is an integral part of managing your total financial portfolio. The SAVE plan requires active management to ensure the benefits remain in place.

The Application and Recertification Process

Borrowers can apply for the SAVE plan through the Federal Student Aid website. A critical component of the plan is annual recertification. You must provide updated income and family size documentation every year. Failure to recertify can result in being moved out of the plan, which could cause unpaid interest to capitalize (be added to the principal), significantly increasing the total cost of the loan.

Integrating SAVE with Public Service Loan Forgiveness (PSLF)

For those working in non-profits, nursing, teaching, or government roles, the SAVE plan is an ideal companion to Public Service Loan Forgiveness (PSLF). Since PSLF forgives the remaining balance after 120 qualifying payments, the goal for these borrowers is to keep their monthly payments as low as possible. The SAVE plan’s generous discretionary income threshold makes it the most effective vehicle for maximizing the amount forgiven under the PSLF program.

The Impact on Credit Scores and Debt-to-Income (DTI)

Mortgage lenders look closely at Debt-to-Income ratios. Because the SAVE plan lowers the required monthly payment, it effectively lowers a borrower’s DTI. This can be the deciding factor in qualifying for a home loan. By lowering the “official” monthly debt obligation, the SAVE plan increases a borrower’s purchasing power in the real estate market, illustrating how student loan policy directly impacts broader economic participation.

Conclusion: A New Standard for Financial Stability

The SAVE plan represents a landmark shift in how personal finance is structured for the modern borrower. By shielding more income, halting interest growth, and shortening the path to forgiveness, it provides a level of financial flexibility previously unavailable. For the savvy investor or the budget-conscious professional, the SAVE plan is not just about paying back a loan; it is about optimizing cash flow, protecting against economic downturns, and building a foundation for long-term wealth. As with any financial tool, its effectiveness depends on the borrower’s ability to integrate it into a comprehensive strategy that balances debt management with aggressive saving and investment.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.