In the intricate world of modern finance, where funds traverse digital pathways with remarkable speed, certain fundamental identifiers ensure every transaction reaches its intended destination. Among these, the routing number stands as a cornerstone of the U.S. banking system. For millions of customers of JPMorgan Chase Bank, understanding this nine-digit code is not merely a technical detail but a crucial component of seamless personal finance management, from direct deposits to bill payments and everything in between.

This comprehensive guide delves into what a routing number is, why it’s indispensable, how to locate your specific Chase routing number, and its myriad applications in your financial life. Whether you’re setting up payroll, transferring funds, or connecting new financial tools, mastering this small but mighty number is key to navigating your financial landscape with confidence and efficiency.

Demystifying Routing Numbers: The Foundation of Digital Transactions

At its core, a routing number is a set of instructions, a digital address for your bank within the vast network of financial institutions. Without it, the sophisticated system of electronic fund transfers that underpins today’s economy would grind to a halt.

What Exactly is a Routing Number?

A routing number, officially known as an ABA (American Bankers Association) routing transit number (RTN), is a nine-digit code that identifies the financial institution processing a transaction. It acts like a street address for your bank, ensuring that when money is sent electronically, it goes to the correct bank, credit union, or other financial services provider. These numbers are unique to each institution, though larger banks with a national presence, like Chase, often have multiple routing numbers assigned based on the geographic region where an account was opened.

The system was originally developed in 1910 by the American Bankers Association to facilitate the sorting and routing of paper checks. While checks have largely gone digital, the underlying principle of the routing number remains vital for electronic transactions.

Why Routing Numbers Are Indispensable

The necessity of routing numbers extends across almost every aspect of electronic banking. They are the silent workhorses that ensure the accuracy and security of billions of transactions daily.

- Ensuring Accuracy: Without a unique identifier for each bank, electronic funds could easily be misdirected, leading to significant delays and potential loss. The routing number funnels funds precisely to the intended financial institution.

- Facilitating Efficiency: Routing numbers are critical for Automated Clearing House (ACH) transactions, which include direct deposits, automatic bill payments, and electronic transfers between banks. They streamline the process, allowing for bulk processing and rapid movement of funds.

- Preventing Errors: By providing a clear destination for funds, routing numbers minimize the chances of errors that could arise from manual processing or ambiguous addressing. This reduces the administrative burden on banks and enhances customer confidence.

- Enabling Digital Finance: From mobile banking apps to online payment platforms and investment tools, nearly every digital financial service relies on routing numbers to link your bank account for deposits, withdrawals, and transfers.

Routing Numbers vs. Account Numbers vs. SWIFT Codes

It’s easy to confuse routing numbers with other financial identifiers, but each serves a distinct purpose. Understanding the differences is crucial for accurate transactions.

- Routing Number (ABA RTN): Identifies your bank within the U.S. banking system. It tells other banks where to send the money.

- Account Number: Identifies your specific account at your bank. Once the money reaches the correct bank (identified by the routing number), the account number directs it to your individual checking, savings, or other account.

- SWIFT Code (Society for Worldwide Interbank Financial Telecommunication): Also known as a BIC (Bank Identifier Code), a SWIFT code is used for international wire transfers. It identifies a specific bank globally, allowing funds to be routed across borders. While a U.S. routing number is sufficient for domestic transfers, international transactions require a SWIFT code for the recipient’s bank. Chase, for instance, has a specific SWIFT code for its international operations.

Navigating Chase Bank’s Routing Numbers

Given Chase’s expansive national presence, it’s a common misconception that there’s a single routing number for all Chase accounts. In reality, Chase, like other large banks, utilizes multiple routing numbers, primarily determined by the state or region where your account was originally opened.

Common Chase Routing Numbers (and why there isn’t just one)

Chase operates across virtually all 50 states, and its vast network necessitated a system to efficiently manage transactions regionally. Therefore, the routing number assigned to your Chase account will depend on the geographical location of the branch where your account was first established, or sometimes the state of residence provided during account opening. This regionalization helps in processing local transactions more quickly and accurately.

For example, a customer who opened an account in New York might have a different routing number than someone who opened an account in California, even if both are Chase customers. It is paramount to use the correct routing number associated with your specific account to avoid delays or rejections of your financial transactions.

How to Find Your Chase Routing Number

Fortunately, Chase makes it relatively straightforward to locate your specific routing number through several reliable channels.

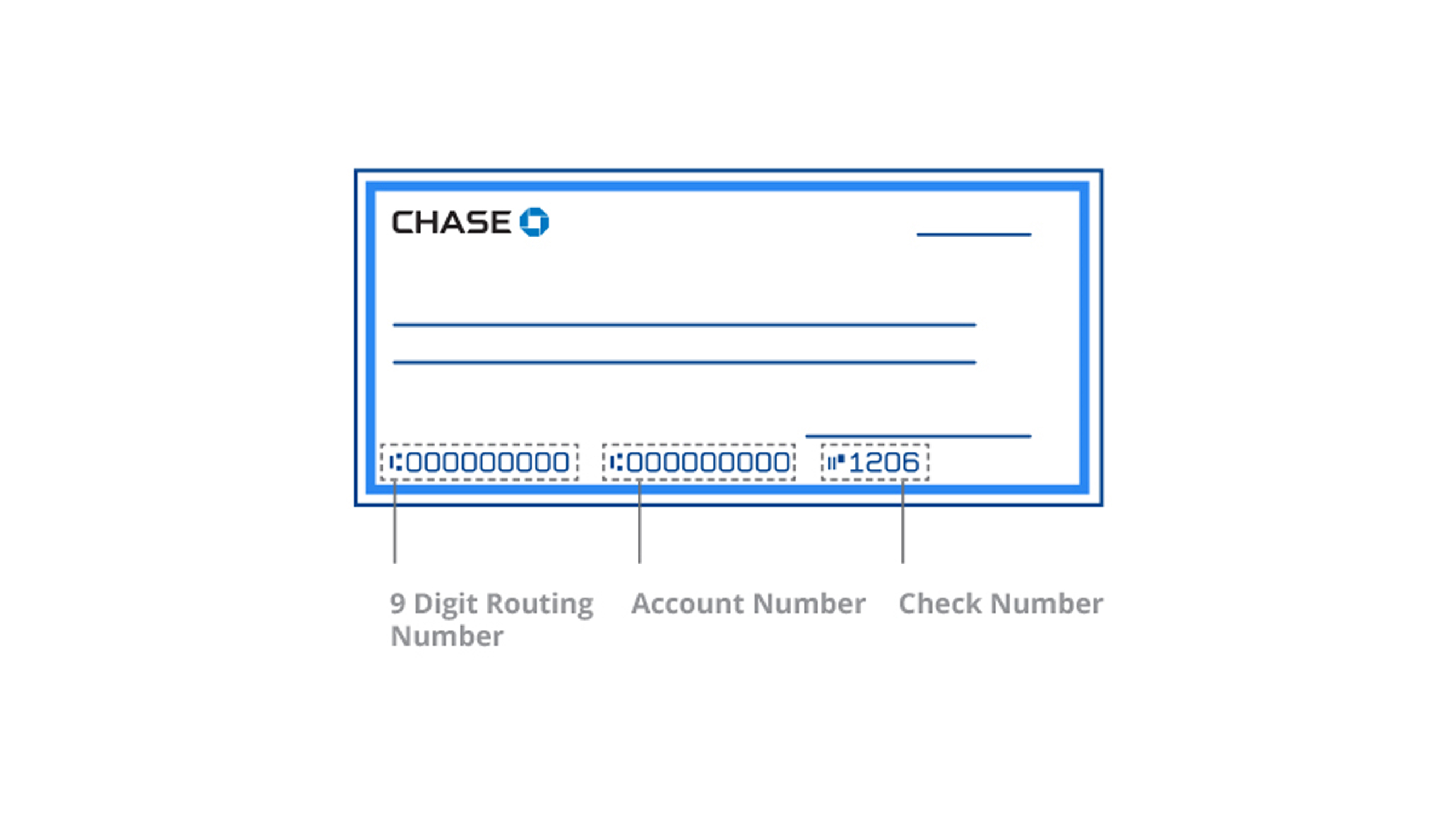

- Check Your Checks: For checking accounts, your routing number is prominently printed on the bottom left-hand corner of your checks. It’s the first nine-digit number, preceding your account number.

- Online Banking (Chase.com):

- Log in to your Chase online banking account.

- Navigate to your account summary or details page.

- Typically, your routing number (and account number) will be displayed clearly here, sometimes under “Account Details” or “Show Details.”

- Chase Mobile App:

- Open and log in to the Chase Mobile app on your smartphone or tablet.

- Select the specific account you need the routing number for.

- Tap on “Show Details” or a similar option, and your routing number will be visible.

- Bank Statement: Your monthly Chase bank statement, whether paper or electronic, will list your routing number along with your account number and other financial details.

- Contact Chase Customer Service: If you’re unable to find it through the digital channels or checks, a quick call to Chase’s customer service can provide you with the correct routing number after verifying your identity.

- Chase Website Routing Number Lookup Tool: Chase often provides a dedicated tool on its official website where you can input your state to find the correct routing number for your region. Always ensure you are on the official Chase website (chase.com) when using such tools.

Key Considerations When Using Chase Routing Numbers

While finding your routing number is simple, applying it correctly requires awareness of a few important nuances.

- Transaction Type Matters: Be aware that Chase, like some other banks, may use different routing numbers for specific transaction types. For instance, a routing number for ACH transfers (like direct deposits) might differ from the one used for wire transfers. Always double-check which number is required for the specific transaction you’re initiating.

- Location, Location, Location: Reiterate that the routing number is tied to where your account was opened or primarily serviced. If you move states, your routing number typically remains the same as the originating branch unless you explicitly open a new account in the new state.

- Verify Before Transacting: The golden rule of financial transactions: always verify the routing number (and account number) before initiating any transfer, especially for significant sums. A small error can lead to substantial headaches.

The Financial Applications of Your Chase Routing Number

Once you’ve identified your correct Chase routing number, a multitude of financial doors open, enabling you to participate fully in the digital economy. It is a vital piece of information for almost every electronic interaction with your bank.

Direct Deposits and Automated Payments

The most common and arguably most impactful use of your routing number is facilitating regular, automated inflows and outflows of money.

- Payroll: For employees, providing your Chase routing number and account number to your employer is how your paycheck gets directly deposited into your account each pay period. This eliminates paper checks and provides immediate access to your funds.

- Government Benefits: Social Security benefits, veterans’ benefits, tax refunds, and other government payments are typically routed directly to your bank account using your routing number.

- Utility Bills and Rent: Many individuals set up automatic bill payments for utilities, rent, mortgage, and other recurring expenses. Your routing number ensures these payments are debited from your Chase account and sent to the correct service provider’s bank.

- Investment Contributions: Linking your Chase checking or savings account to brokerage accounts, 401(k)s, IRAs, or other investment platforms for automated contributions or withdrawals requires your routing number.

Electronic Fund Transfers (EFTs)

Beyond automated recurring payments, your routing number is essential for various types of electronic transfers.

- ACH Transfers: These are the backbone of electronic banking, allowing you to move money between your own accounts at different banks, pay individuals, or receive payments. ACH transfers are generally free or low-cost and typically take 1-3 business days to process. For example, transferring money from your Chase checking account to a savings account at an online-only bank will require Chase’s routing number.

- Wire Transfers: While ACH transfers are suitable for most domestic transactions, wire transfers are often preferred for their speed (same-day processing) and for large, time-sensitive sums. Wire transfers typically incur higher fees. You’ll need your Chase routing number, and sometimes a specific wire transfer routing number (if different from the ACH one), to send or receive funds via wire.

- Peer-to-Peer (P2P) Payment Apps: While apps like Venmo, PayPal, and Zelle often abstract the routing number from the user’s direct view during transactions, they rely on it internally to link your bank account for sending and receiving funds. When you initially connect your Chase account to these services, you’ll often be prompted for your routing and account numbers.

Setting Up New Financial Tools and Services

The proliferation of financial technology (fintech) has led to an ecosystem of apps and platforms designed to help manage, save, invest, and spend money more efficiently. Your Chase routing number is often the bridge connecting these tools to your bank account.

- Budgeting Apps: Apps like Mint or YNAB connect to your bank accounts to track spending and categorize transactions, which typically involves providing your routing and account numbers.

- Investment Platforms: Whether you’re using robo-advisors, traditional brokerage accounts, or micro-investing apps, linking your Chase account for funding purposes will require your routing information.

- Loan Applications: When applying for a loan (personal loan, auto loan, mortgage), lenders may ask for your bank’s routing number to facilitate funding or repayment setups.

- Payment Processors for Businesses: For small business owners, your Chase routing number is critical for setting up payment processing services to accept customer payments and for managing payroll and vendor payments. It’s a foundational element of effective business finance.

Security Best Practices and Common Pitfalls

While routing numbers are widely known and generally considered less sensitive than an account number, exercising caution is always prudent in financial matters. Misuse or incorrect application can lead to inconvenience and potential financial implications.

Protecting Your Financial Information

Although your routing number is publicly available (in the sense that it identifies a bank, not your personal account), it’s part of your complete banking identity.

- Share Judiciously: Only provide your routing and account numbers to trusted entities for legitimate financial transactions (e.g., employers, government agencies, reputable financial institutions, established bill payees).

- Use Secure Platforms: Always use Chase’s official online banking portal or mobile app for managing your accounts and finding your routing number. Avoid clicking on suspicious links or providing information through unsecured websites.

- Beware of Phishing: Be highly suspicious of unsolicited emails, texts, or calls asking for your banking details, including routing numbers. Chase will never ask for this information in an unverified manner.

What Happens If You Use the Wrong Routing Number?

Mistakes happen, but using an incorrect routing number can cause various issues, ranging from minor inconveniences to significant delays.

- Transaction Delays: The most common outcome is that the transaction will be delayed or rejected. The automated system will detect a mismatch between the routing number and the intended account number or bank.

- Rejection of Transaction: The funds may simply be returned to the sender’s account. This means your direct deposit won’t go through, your bill won’t be paid, or your transfer will fail.

- Potential Fees: While often not the case for rejections due to incorrect routing numbers, some banks or payment processors might levy fees for failed transactions.

- Funds Sent to Wrong Account (Rare but Possible): In extremely rare instances, if an incorrect routing number and an incorrect account number happen to match a legitimate, active account at a different institution, funds could theoretically be misdirected. However, banking systems have robust checks and balances to prevent this, and typically, if the account number doesn’t match the routing number’s bank, the transaction is rejected. If it does occur, recovering funds can be a complex and lengthy process involving both banks.

When to Seek Professional Guidance

For complex financial situations or when dealing with significant sums, don’t hesitate to consult with financial professionals or directly with Chase.

- Large Sums of Money: For very large transfers, especially if it’s your first time, confirm all details with a Chase representative.

- International Transfers: These always involve SWIFT codes and often additional intermediary bank details. Always verify with Chase for international wire instructions.

- Uncertainty or Complex Setups: If you’re unsure about which routing number to use for a particular service or transaction type, or if you’re setting up intricate financial integrations, a quick call to Chase customer service can save you a lot of trouble.

Looking Ahead: The Evolution of Banking Identifiers

While routing numbers have been a constant for over a century, the landscape of financial technology is in constant flux. The future promises faster, more integrated payment systems, but the underlying need for bank identification remains.

Faster Payments and Real-Time Transactions

The U.S. financial system is moving towards real-time payment (RTP) networks and initiatives like FedNow, which aim to make transactions instantaneous, 24/7. Even with these advancements, routing numbers will continue to play a foundational role in identifying the participating financial institutions, even if the processing layers above them become more sophisticated. They provide the necessary institutional context for instant fund movement.

Global Standards and Interoperability

While SWIFT codes govern international transfers, there’s ongoing discussion about greater global interoperability and potentially more universal identifiers in the long term. However, for domestic U.S. transactions, the ABA routing number remains the established standard.

The Enduring Importance of the Routing Number

Despite the rapid evolution of digital finance, the routing number stands as a testament to effective, albeit foundational, financial infrastructure. For Chase customers, understanding and correctly utilizing their specific routing number is not just a relic of traditional banking but a vital skill for managing their money in the modern age. It underpins nearly every electronic financial interaction, ensuring that your hard-earned money always finds its way home.

By taking the time to know your Chase routing number and understanding its purpose, you empower yourself with the knowledge needed to manage your personal finances effectively, securely, and with complete confidence. In a world of increasingly complex financial tools, sometimes the most basic pieces of information are the most powerful.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.