The Roth IRA stands as a cornerstone of personal finance for many, celebrated for its unique tax advantages and potential to generate substantial wealth for retirement. Unlike traditional retirement accounts where contributions might be tax-deductible and withdrawals taxed in retirement, the Roth IRA operates on an opposite principle: contributions are made with after-tax dollars, but qualified withdrawals in retirement are entirely tax-free. This fundamental difference shapes the “return” on a Roth IRA, making it a compelling vehicle for long-term financial growth. Understanding this return requires looking beyond mere percentage gains to encompass the powerful interplay of investment performance, tax efficiency, and strategic planning.

Understanding the Core Value Proposition of a Roth IRA

The true “return” on a Roth IRA isn’t just about the raw investment gains; it’s intricately linked to its tax structure and the compounding effect over decades. This makes its value proposition particularly strong for those who anticipate being in a higher tax bracket in retirement than they are today.

Tax-Free Growth and Withdrawals

The most significant benefit, and a crucial component of its effective return, is the tax-free status of qualified withdrawals. This means that every dollar of profit, every dividend reinvested, and every capital gain realized within the Roth IRA grows without being subject to federal income tax (and often state tax, depending on jurisdiction). When you reach retirement age (59½ and have had the account for at least five years), all withdrawals are completely tax-free. This stands in stark contrast to pre-tax retirement accounts, where withdrawals are taxed as ordinary income, effectively reducing your net return. Over several decades, escaping taxes on growth can add a significant percentage to your real return, potentially translating into hundreds of thousands of dollars saved.

The Power of Compounding

Like any investment vehicle, the Roth IRA harnesses the incredible power of compounding. When your initial investments generate returns, those returns themselves begin to earn returns, creating an accelerating growth trajectory. Because the gains within a Roth IRA are shielded from taxes year-to-year, more money remains invested and continues to compound. This uninterrupted compounding, combined with tax-free withdrawals, amplifies the long-term growth potential significantly. An investment earning 7% annually, compounded over 30-40 years within a tax-free wrapper, will yield a dramatically higher net amount than an identical investment exposed to annual taxation on its gains or withdrawals.

Investment Flexibility

A Roth IRA allows investors a wide degree of flexibility in choosing their investments. Unlike some employer-sponsored plans that might have a limited selection of mutual funds, a Roth IRA typically allows you to invest in a broad spectrum of assets, including stocks, bonds, mutual funds, exchange-traded funds (ETFs), and even some alternative investments through various brokerages. This flexibility means you can tailor your portfolio to your risk tolerance, investment goals, and market outlook, directly impacting your potential investment returns. The ability to select investments that align with your strategy is key to optimizing the growth within the account.

Factors Influencing Roth IRA Returns

While the tax-free nature is a constant benefit, the actual monetary return on a Roth IRA is variable and depends on several critical factors.

Asset Allocation and Portfolio Diversification

The types of assets you choose to hold within your Roth IRA significantly influence its returns. A portfolio heavily weighted towards growth stocks or aggressive equity funds might yield higher returns in bull markets but also carry greater risk of loss. Conversely, a more conservative allocation with a higher proportion of bonds or money market funds will typically offer lower returns but also lower volatility. Diversification across different asset classes, industries, and geographies helps mitigate risk and can lead to more consistent long-term returns. A well-constructed asset allocation aligned with your time horizon and risk tolerance is paramount for optimizing Roth IRA performance.

Market Performance and Economic Cycles

The broader market environment plays an undeniable role. When the stock market experiences periods of sustained growth, Roth IRAs invested in equities will naturally see higher returns. Conversely, market downturns can lead to temporary (or sometimes sustained, if poorly managed) reductions in account value. Economic factors such as interest rates, inflation, and global events can all impact asset prices and, by extension, your Roth IRA’s performance. It’s crucial to remember that investment returns are not linear and will fluctuate with market cycles.

Investment Fees and Expenses

Fees can erode returns over time, sometimes subtly but significantly. These include expense ratios for mutual funds and ETFs, trading commissions, and account maintenance fees. Even seemingly small fees of 0.5% or 1% annually can shave tens of thousands of dollars off your final retirement sum over several decades due to the loss of compounded growth. Savvy investors prioritize low-cost index funds or ETFs to minimize these erosive effects, thereby enhancing their net return.

Time Horizon

The length of time your money remains invested is arguably the most powerful determinant of your Roth IRA’s ultimate return. The longer your investment horizon, the more time compounding has to work its magic, and the more likely your portfolio is to recover from market downturns and benefit from long-term market trends. Starting early with even modest contributions can lead to substantially higher returns than starting later with larger contributions, thanks to the exponential nature of compounding.

Estimating Potential Roth IRA Returns

While past performance is not indicative of future results, historical data and reasonable assumptions can help estimate potential Roth IRA returns.

Historical Market Averages

Over the long term, the U.S. stock market (as measured by indices like the S&P 500) has historically delivered an average annual return of approximately 10-12% before inflation, or about 7-8% after inflation. This is a common benchmark used for projecting long-term growth. However, individual portfolio returns will vary based on their specific asset allocation and investment choices. It’s important to use a realistic, conservative estimate for financial planning, perhaps in the range of 5-8% net of inflation and fees, especially for a diversified portfolio.

Realistic Growth Expectations

It’s wise to project returns using a range rather than a single fixed number. For example, some financial planners might use a 6% assumption for a moderately conservative portfolio and an 8% assumption for a more aggressive, equity-heavy portfolio. The key is to be realistic and understand that market cycles will lead to periods of higher and lower returns. The benefit of the Roth IRA is that all of this growth, whatever its magnitude, will be tax-free upon withdrawal.

The Role of Personal Contributions

While market returns are crucial, the consistent addition of personal contributions forms the bedrock of a Roth IRA’s total return. Regular contributions, especially if they maximize the annual limit, significantly increase the principal upon which investment gains can compound. A Roth IRA with an average annual return of 7% will accumulate far more wealth if $6,500 (2023 limit) is contributed each year compared to only $1,000. The total value is a function of both the investment return percentage and the total dollars invested.

Comparing Roth IRA Returns with Other Retirement Vehicles

Understanding the Roth IRA’s return also involves contextualizing it against other common retirement accounts, particularly concerning tax implications.

Traditional IRA vs. Roth IRA (Tax Treatment Impact)

The primary difference lies in tax timing. Traditional IRA contributions are often tax-deductible in the year they are made, leading to tax savings upfront. However, withdrawals in retirement are taxed as ordinary income. A Roth IRA offers no upfront deduction, but qualified withdrawals are tax-free. The “return” can be higher in a Roth IRA if you anticipate being in a higher tax bracket in retirement or if tax rates generally increase in the future. The tax-free growth and withdrawals can effectively mean a higher net return on your investment dollars compared to a traditional IRA where those gains would eventually be taxed.

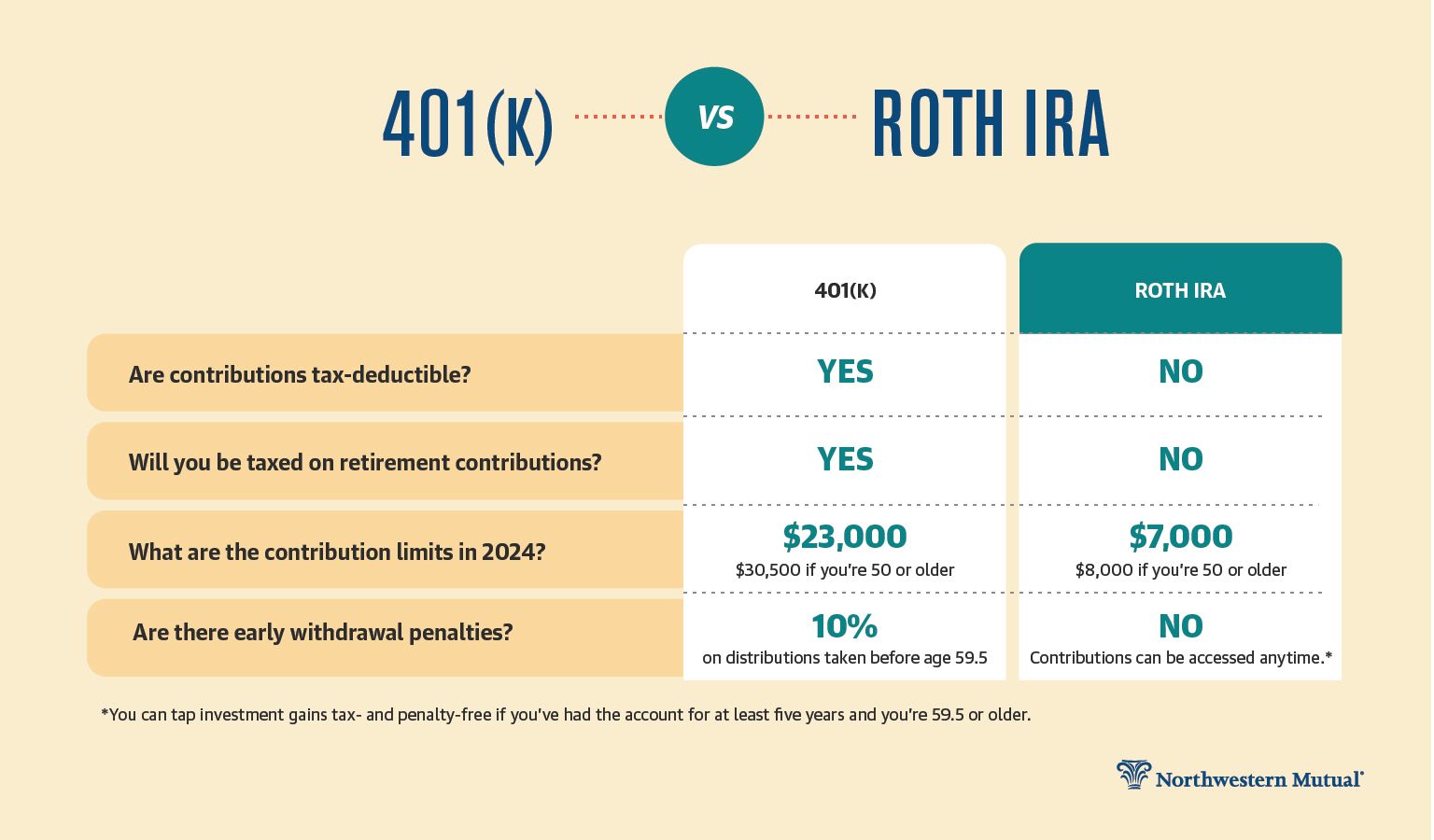

401(k) vs. Roth IRA

Many employers offer 401(k)s, which are similar to Traditional IRAs in that contributions are typically pre-tax, and withdrawals are taxed in retirement. Some employers also offer Roth 401(k)s, which mirror the Roth IRA’s tax structure (after-tax contributions, tax-free withdrawals). The main advantage of a 401(k) is often a higher contribution limit and potential employer matching contributions, which are an immediate 100% return on your contribution up to the match limit. While an employer match is undeniably valuable, the Roth IRA still offers the unparalleled benefit of entirely tax-free growth and withdrawals, making it a powerful complement or alternative, especially for those who max out their 401(k) contributions.

Taxable Investment Accounts

Investing in a standard brokerage account, while offering liquidity, does not provide the same tax advantages. Capital gains and dividends are generally taxed annually or upon sale. This means less money remains invested to compound, and your net return is significantly reduced by taxes. A Roth IRA’s tax-free growth environment offers a substantial advantage, allowing for far greater long-term accumulation compared to an identically performing taxable account.

Maximizing Your Roth IRA’s Return Potential

Achieving a high return on your Roth IRA involves more than just opening an account; it requires strategic engagement and consistent effort.

Consistent Contributions

Regularly contributing to your Roth IRA, ideally maxing out the annual contribution limit, is the single most effective way to leverage its power. Consistent contributions, whether monthly or annually, ensure that more of your money is working for you, compounding tax-free over the long haul. Even during market downturns, consistent contributions allow you to buy assets at lower prices, a strategy known as dollar-cost averaging, which can enhance returns when the market recovers.

Strategic Investment Choices

Selecting appropriate investments is critical. Focus on a diversified portfolio that aligns with your risk tolerance and time horizon. For younger investors with a long time until retirement, a growth-oriented portfolio heavily weighted towards equities might be suitable. As retirement approaches, a gradual shift towards more conservative assets might be prudent. Utilizing low-cost index funds or ETFs that track broad market indices can be an efficient way to achieve market-like returns without incurring high fees.

Regular Portfolio Review and Rebalancing

Markets shift, and so should your portfolio, to some extent. Periodically reviewing your Roth IRA investments (e.g., annually) ensures they still align with your goals and risk tolerance. Rebalancing involves adjusting your asset allocation back to your target percentages. For example, if equities have performed exceptionally well, you might sell some to buy bonds, bringing your portfolio back into balance and locking in some gains while managing risk.

Avoiding Common Pitfalls

To maximize returns, avoid common mistakes such as market timing (trying to buy low and sell high), excessive trading (which incurs fees and often underperforms), reacting emotionally to market volatility, and neglecting diversification. The long-term, buy-and-hold strategy, coupled with consistent contributions and tax-free growth, is typically the most reliable path to a high return on a Roth IRA. Remember, the true “return” is not just the growth percentage but the net amount you can withdraw tax-free in retirement.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.