Taxation is the cornerstone of a functioning society, providing the necessary capital for infrastructure, public services, and national security. However, for some individuals and corporations, the pressure of financial obligations leads to the temptation of tax evasion. While it may seem like a shortcut to preserving wealth in the short term, tax evasion is a serious federal crime with consequences that can dismantle a person’s financial future and personal liberty.

In the realm of personal and business finance, understanding the boundary between legal tax planning and illegal evasion is critical. This article explores the multifaceted punishments associated with tax evasion, the mechanisms tax authorities use for detection, and the long-term implications for your financial health.

Defining Tax Evasion in the Modern Financial Landscape

To understand the punishment, one must first understand the crime. Tax evasion is not a simple mistake on a return; it is the illegal non-payment or underpayment of taxes. This usually involves a deliberate attempt to hide income or misrepresent financial affairs to the authorities.

Tax Avoidance vs. Tax Evasion: The Fine Line

In financial circles, the distinction between avoidance and evasion is paramount. Tax avoidance is the legal utilization of the tax regime to your advantage. This includes contributing to 401(k) plans, claiming legitimate business expenses, or utilizing tax credits. Tax evasion, conversely, involves “willfulness.” If an individual intentionally misstates their income or hides assets offshore to circumvent tax laws, they have crossed into criminal territory. The IRS and other global tax bodies focus heavily on “intent” when deciding whether to pursue criminal charges or civil penalties.

Common Examples of Evasive Actions

Tax evasion manifests in various forms across the financial spectrum. For individuals, it often involves failing to report income from side hustles, “under the table” cash payments, or offshore accounts. For businesses, common tactics include “skimming” (taking cash off the top before recording sales), inflating expenses, or maintaining two sets of books. In the digital age, failing to report cryptocurrency gains has also become a major focus for tax enforcement agencies, as digital assets are now treated as taxable property.

Civil vs. Criminal Penalties: Assessing the Cost

When the IRS or a national tax authority identifies a discrepancy, the consequences generally fall into two categories: civil penalties and criminal prosecution. The severity of the punishment depends largely on the amount of tax owed and the evidence of fraudulent intent.

Monetary Fines and Interest Accumulation

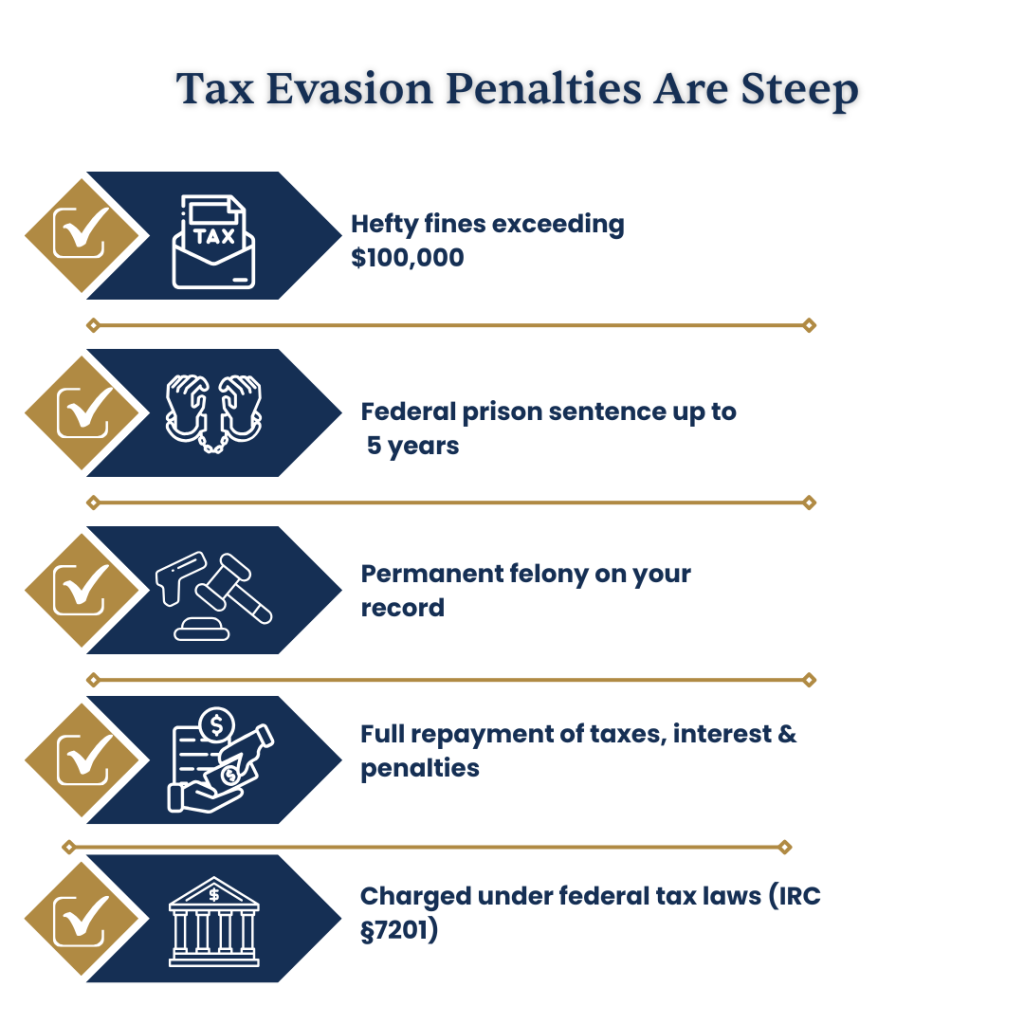

Even if the government chooses not to pursue jail time, the financial penalties for tax evasion are designed to be ruinous. In the United States, for example, the civil fraud penalty is 75% of the underpayment attributable to fraud. This is in addition to the original taxes owed.

Furthermore, interest on the unpaid amount begins accruing from the original due date of the return. Because these interest rates are compounded daily, a tax debt can easily double or triple within a few years of an investigation. For a business, these liquidations can lead to immediate insolvency, as the government has the power to seize bank accounts and business assets to satisfy the debt.

Prison Sentences and Criminal Records

When “willfulness” is proven, the case moves into the criminal justice system. Tax evasion is a felony. Under federal law, a person convicted of tax evasion can face up to five years in prison for each count or “tax year” involved.

A criminal conviction also carries a permanent mark. Beyond the loss of physical freedom, a felony conviction for a financial crime makes it nearly impossible to hold fiduciary positions, maintain certain professional licenses (such as in law, medicine, or accounting), or serve as a director of a public company. The social and professional stigma often outweighs the immediate financial loss.

The Long-term Impact on Business and Personal Finance

The repercussions of tax evasion extend far beyond the courtroom and the immediate payment of fines. The secondary effects can cripple an individual’s ability to generate wealth or manage a business for decades.

Asset Forfeiture and Liens

One of the most aggressive tools used by tax authorities is the federal tax lien. A lien is a legal claim against your property—including your home, car, and financial assets—to ensure the government gets paid. Once a lien is filed, it becomes a matter of public record. If the debt remains unpaid, the government may move toward a “levy,” which is the actual seizure of the property. This can include garnishing wages, taking money directly from bank accounts, or selling physical property at auction to cover the tax liability.

Damage to Financial Reputation and Creditworthiness

While tax liens are no longer automatically included on traditional consumer credit reports, they remain visible to lenders during deep-background checks and manual underwriting. For a business owner, a history of tax evasion is a “death knell” for securing venture capital, traditional bank loans, or lines of credit. Investors and financial institutions view tax evaders as high-risk entities who lack integrity. This loss of “financial character” limits an individual’s ability to leverage debt for future growth, effectively capping their potential for wealth accumulation.

How Tax Authorities Detect Discrepancies

Many people underestimate the sophistication of modern tax enforcement. In the past, evasion was easier to hide in paper ledgers; today, the “digital footprint” of financial transactions makes evasion increasingly difficult to sustain.

Digital Audits and Information Sharing

Tax authorities now employ advanced data-mining techniques and AI-driven algorithms to flag returns that deviate from the norm. They use “Information Matching” to cross-reference the income reported on your return with 1099s and W-2s sent by employers and financial institutions.

Furthermore, international cooperation has reached an all-time high. Under the Foreign Account Tax Compliance Act (FATCA) and the Common Reporting Standard (CRS), over 100 countries now share financial data. If a taxpayer hides money in a Swiss or Cayman Islands bank account, there is a high probability that the home country’s tax office will receive a digital report of that account’s existence.

The Role of Whistleblowers and Financial Institutions

Financial institutions are legally required to file Suspicious Activity Reports (SARs) for transactions that seem designed to avoid reporting requirements (a practice known as “structuring”). Additionally, the IRS Whistleblower Office provides significant monetary rewards to individuals who report large-scale tax evasion. Often, disgruntled employees, former business partners, or ex-spouses provide the “smoking gun” evidence that triggers a criminal investigation.

Mitigating Risk and Ensuring Compliance

The best way to avoid the crushing weight of tax evasion penalties is proactive compliance. However, for those who realize they have made past errors, there are legal pathways to rectify the situation before the authorities initiate an audit.

Voluntary Disclosure Programs

Many tax jurisdictions offer “Voluntary Disclosure” programs. These programs are designed for taxpayers who have committed tax-related crimes but want to come clean. By proactively reporting the errors and paying the back taxes and interest, an individual can often avoid criminal prosecution and receive reduced civil penalties. The key requirement is that the disclosure must be “timely”—meaning you must come forward before the tax authority begins an investigation into your affairs.

The Importance of Professional Financial Advisory

Managing complex personal or business finances requires professional oversight. Engaging a Certified Public Accountant (CPA) or a tax attorney ensures that you are utilizing all legal avenues for tax reduction while staying firmly on the right side of the law.

Professional advisors provide “Audit Representation” and can help structure business entities in ways that optimize tax efficiency. In the world of finance, the cost of a high-quality accountant is a fraction of the cost of a tax evasion defense attorney. Staying compliant is not just a legal obligation; it is a fundamental strategy for sustainable financial growth and the preservation of one’s legacy.

In conclusion, the punishment for tax evasion is designed to be comprehensive, targeting an individual’s wealth, freedom, and reputation. By maintaining transparent financial records and seeking professional guidance, you can navigate the complexities of the tax code without risking the severe consequences of evasion.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.