In the vast ecosystem of global commerce, businesses take on myriad forms, each structured to suit particular objectives, ownership preferences, and growth trajectories. Among these, the private company stands as a foundational pillar, representing the majority of enterprises worldwide. Far from being a monolithic entity, the private company encompasses a diverse range of organizations, from sole proprietorships and family businesses to venture-backed startups and large, privately-held conglomerates. Understanding “what is the private company” is not merely an academic exercise; it is crucial for investors, entrepreneurs, policymakers, and anyone seeking to comprehend the intricate mechanics of our economies.

At its core, a private company is any business entity whose shares or ownership interests are not publicly traded on a stock exchange. This fundamental distinction from a public company underpins a unique set of characteristics regarding ownership, funding, governance, and operational strategy, all of which have profound financial implications. While often less visible than their publicly-listed counterparts, private companies are powerful engines of innovation, employment, and economic growth, shaping industries and communities with their distinct approach to business.

Defining the Private Company: Ownership and Control

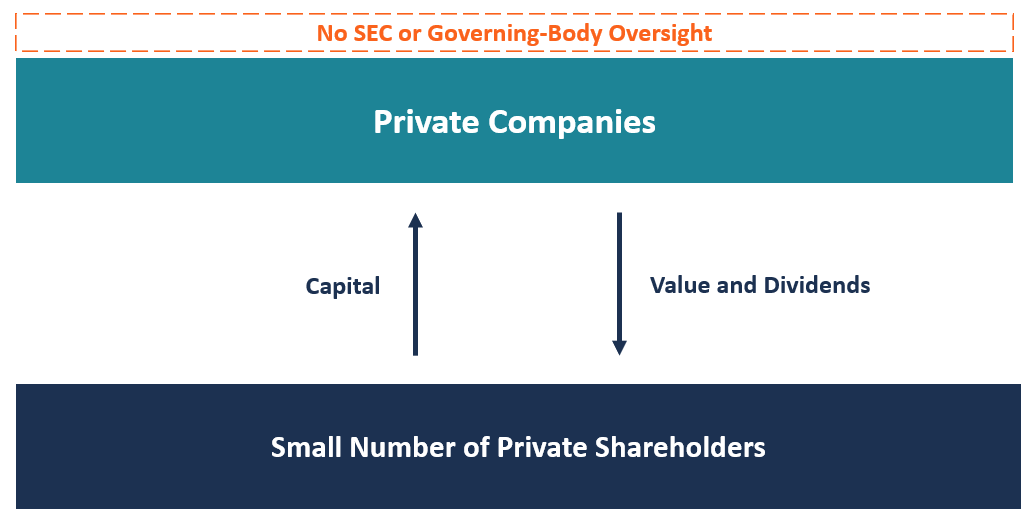

The defining characteristic of a private company lies in its ownership structure and the control exerted over its operations. Unlike public companies, which offer their shares to the general public, private companies restrict ownership to a select group of individuals, families, employees, or private investors. This concentrated ownership model has significant ramifications for how these companies are run and financed.

Key Characteristics of Private Ownership

Private companies are typically characterized by a limited number of shareholders, who often have a direct and substantial involvement in the company’s management and strategic direction. Ownership is not widely dispersed; instead, it is held by founders, family members, private equity firms, venture capitalists, or a small group of accredited investors. This tight-knit ownership structure fosters a culture of deep commitment and long-term vision, as shareholders are often personally invested in the company’s success, both financially and emotionally.

Crucially, the shares of a private company are not freely transferable on open markets. Any transaction involving the sale or transfer of ownership interests typically requires approval from existing shareholders or adherence to specific contractual agreements, such as buy-sell agreements or rights of first refusal. This illiquidity is a defining trait, influencing how investors value their stakes and plan for future exits.

Distinction from Public Companies

The contrast between private and public companies is stark, particularly from a financial and regulatory perspective. Public companies, having raised capital by selling shares to the public, are subject to stringent regulatory oversight from bodies like the Securities and Exchange Commission (SEC) in the United States. They are mandated to disclose extensive financial and operational information to the public on a regular basis, including quarterly and annual reports, to ensure transparency for public shareholders. This level of disclosure comes with significant compliance costs and can expose strategic initiatives to competitors.

Private companies, by virtue of not being publicly traded, are exempt from most of these reporting requirements. While they must still adhere to accounting standards and tax regulations, their financial affairs remain largely confidential. This privacy offers a competitive advantage, allowing companies to maintain secrecy around product development, financial performance, and strategic decisions, fostering an environment where long-term plans can be executed without short-term market pressures.

Legal Structures for Private Entities

The term “private company” is an umbrella that covers various legal structures, each with its own implications for liability, taxation, and ownership. Common forms include:

- Sole Proprietorship: Owned and run by one individual, with no legal distinction between the owner and the business. The owner is personally liable for all business debts.

- Partnership: Owned by two or more individuals who share in profits, losses, and management. Like sole proprietorships, partners typically have unlimited personal liability, though limited partnerships (LPs) and limited liability partnerships (LLPs) offer some protections.

- Limited Liability Company (LLC): A hybrid structure combining the pass-through taxation of a partnership or sole proprietorship with the limited liability of a corporation. Members (owners) are not personally liable for the company’s debts.

- S Corporation (S-Corp): A special IRS tax election for corporations that allows profits and losses to be passed directly to the owner’s personal income without being subject to corporate tax rates. Limits apply to the number and type of shareholders.

- C Corporation (C-Corp): The most common form for larger private companies, and the standard for public companies. Offers limited liability to shareholders but is subject to “double taxation” (corporate profits taxed at the corporate level, and dividends taxed again at the shareholder level).

The choice of legal structure is a critical financial decision, impacting everything from tax obligations and personal liability protection to fundraising capabilities and exit strategies.

Financial Implications and Capital Generation

The private nature of a company fundamentally alters its approach to fundraising, valuation, and investor relations. Without access to public stock markets, private companies must rely on alternative avenues for capital, which shapes their growth trajectory and financial strategy.

Funding Mechanisms for Private Companies

Private companies employ a range of funding mechanisms tailored to their stage of development and capital requirements. Early-stage startups often secure seed funding from angel investors or friends and family. As they grow, they may turn to venture capital (VC) firms, which invest in high-growth potential companies in exchange for equity, often taking a significant stake and providing strategic guidance. Mid-market and mature private companies might attract private equity (PE) firms, which typically acquire controlling stakes in established businesses with the goal of improving operations and eventually selling them for a profit.

Other significant funding sources include debt financing from banks and other financial institutions, bootstrapping (funding growth through internal cash flow), and convertible notes or SAFEs (Simple Agreement for Future Equity), particularly common in the startup ecosystem, allowing investors to convert their investment into equity at a later valuation event. Each of these mechanisms comes with distinct terms, risks, and implications for company control and future dilution, requiring careful financial planning and negotiation.

Valuation and Investor Relations in Private Markets

Valuing a private company is inherently more complex than valuing a public one, given the lack of readily available market prices and public financial data. Valuation often relies on methods like discounted cash flow (DCF) analysis, comparable company analysis (using public or private transactions as benchmarks), or asset-based valuations. The valuation process is often subjective and can be heavily influenced by negotiation between the company and potential investors.

Investor relations in private companies are typically more direct and personalized. Founders and management often maintain close communication with their limited group of shareholders, holding regular board meetings and providing detailed financial updates. This direct engagement fosters stronger relationships but also places a significant burden on management to manage diverse investor expectations, especially when multiple rounds of funding bring in different types of investors with varying timelines and objectives.

Exit Strategies and Liquidity Events

For many private investors, particularly venture capitalists and private equity firms, the ultimate goal is a “liquidity event”—an opportunity to convert their illiquid equity stake into cash. Common exit strategies for private companies include:

- Initial Public Offering (IPO): The company sells shares to the public for the first time, becoming a publicly traded entity. This is often the most lucrative exit for founders and early investors but is complex, costly, and highly regulated.

- Acquisition (Merger & Acquisition – M&A): The company is bought by another company, either public or private. This is a common exit strategy, offering a clear payout to shareholders.

- Secondary Sale: Existing shareholders sell their shares to new private investors, often occurring during later-stage funding rounds.

- Recapitalization: The company alters its capital structure, often involving issuing new debt or equity to distribute cash to existing shareholders, without selling the entire company.

Planning for an exit strategy is a critical financial consideration from the outset, influencing how a company structures its ownership, manages its growth, and makes strategic decisions to maximize shareholder value upon exit.

Operational Advantages and Strategic Flexibility

Beyond financial structures, the private nature of a company bestows several operational advantages that contribute to its unique strategic flexibility and potential for long-term value creation.

Agile Decision-Making and Long-Term Vision

One of the most significant benefits of being a private company is the ability to make swift decisions without the constant scrutiny and short-term pressures of public markets. Public companies are often compelled to focus on quarterly earnings targets and market reactions, which can sometimes deter long-term investments or risky but potentially transformative strategies. Private companies, with fewer shareholders and often a unified vision among ownership, can pursue multi-year projects, invest heavily in R&D, or pivot their business model without fear of immediate stock price repercussions. This agility fosters innovation and allows for a more patient approach to growth, prioritizing sustainable value over immediate profits.

Privacy in Financial Reporting and Operations

As mentioned, private companies are not required to disclose their financial results to the public. This privacy extends beyond balance sheets and income statements to operational details, strategic plans, and proprietary technologies. This confidentiality is a substantial competitive advantage, preventing rivals from gaining insights into pricing strategies, customer bases, or product roadmaps. It also allows companies to experiment and even fail discreetly, learning valuable lessons without public backlash or damage to market reputation that a public company might face. This protective shield enables a more focused and unburdened pursuit of business objectives.

Focus on Core Business and Stakeholder Value

Private companies can often maintain a stronger focus on their core business, customers, and employees, rather than being primarily driven by shareholder returns in the short term. While shareholder value is always important, the concentrated ownership structure allows for a broader definition of success, which might include employee satisfaction, community impact, or product excellence, alongside financial metrics. This can lead to more stable employment, deeper customer relationships, and a stronger company culture, which in turn can contribute to long-term financial resilience and growth. Family-owned businesses, for instance, frequently prioritize multi-generational legacy over quarterly profits.

Challenges and Considerations for Private Ventures

While offering distinct advantages, operating as a private company also comes with its own set of challenges that require careful navigation, particularly from a financial management perspective.

Access to Capital and Growth Limitations

One of the most significant drawbacks for private companies is the limited access to vast pools of capital available through public stock markets. While venture capital and private equity can provide substantial funding, these sources are often selective and come with high expectations for returns, sometimes leading to significant dilution of founder equity. Without the ability to issue new shares to the public, rapidly scaling private companies may face constraints on growth if they cannot secure sufficient private investment or debt financing. This limitation necessitates creative financial planning and a strategic approach to capital raising.

Governance and Succession Planning

Effective governance in a private company can be complex, especially as the company grows and brings in external investors. Balancing the interests of founders, family members, and various investor groups (angel, VC, PE) requires robust governance structures, clear shareholder agreements, and transparent decision-making processes. Succession planning is another critical financial and operational challenge, particularly for family-owned businesses or founder-led companies. Ensuring a smooth transition of leadership and ownership can be vital for the company’s long-term survival and value preservation, often requiring intricate estate planning and buy-sell agreements to manage equity transfers.

Perceived Lack of Transparency

Despite the advantages of privacy, the lack of public disclosure can sometimes be perceived as a negative by certain stakeholders. For potential business partners, customers, or even employees, the absence of public financial data might make it harder to assess a private company’s stability or long-term viability. This can occasionally hinder opportunities for partnerships, talent acquisition, or even securing favorable credit terms, as lenders might demand more extensive due diligence due to the lack of publicly vetted information. Private companies often counteract this by building strong reputations, demonstrating consistent performance, and providing selective disclosures to key partners when necessary.

The Broader Economic Impact of Private Companies

The aggregate contribution of private companies to the global economy is immense and often underestimated. They are the backbone of most national economies, performing functions that range from local services to cutting-edge research and development.

Driving Innovation and Job Creation

Private companies, especially small and medium-sized enterprises (SMEs) and startups, are disproportionately responsible for innovation and job creation. Free from public market pressures, they can take greater risks, experiment with new technologies, and disrupt established industries. Many revolutionary products and services originate within private ventures before they ever consider going public or being acquired. This continuous cycle of innovation fuels economic dynamism and provides new employment opportunities across various sectors, from technology to traditional manufacturing.

Role in Local and Global Economies

From local main street businesses that anchor communities to multinational private conglomerates that operate across borders, private companies play a vital role in both local and global economies. They provide essential goods and services, contribute to tax revenues, and form complex supply chains that link industries worldwide. Their resilience and adaptability, particularly during economic downturns, can be crucial for maintaining stability. Understanding and supporting the private company ecosystem is therefore paramount for fostering sustained economic prosperity and growth.

In conclusion, the private company is a multifaceted entity defined by its restricted ownership, confidential operations, and often long-term strategic outlook. While facing unique challenges in capital generation and governance, its advantages in agility, privacy, and focused stakeholder value make it an indispensable component of the financial and economic landscape. As the world continues to evolve, the enduring strength and adaptability of private companies will undoubtedly remain central to innovation, wealth creation, and sustainable growth across industries.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.