In the intricate world of finance, few indicators hold as much sway over the average consumer and multinational corporation alike as the prime rate. Often mentioned in economic reports and lending agreements, this seemingly esoteric figure is, in fact, a foundational benchmark that influences everything from the interest on your credit card to the cost of capital for a burgeoning startup. Understanding the prime rate isn’t just for economists or financial professionals; it’s a critical piece of financial literacy that empowers individuals and businesses to make informed decisions about borrowing, saving, and investing.

At its core, the prime rate represents the interest rate that commercial banks charge their most creditworthy corporate customers. While this definition might sound exclusive, its ripple effects permeate the entire financial ecosystem. It acts as a baseline from which many other variable interest rates are derived, making its current value a pertinent question for anyone navigating the financial landscape. As central banks adjust monetary policy to steer economic conditions, the prime rate responds, reflecting the broader cost of money in the economy. This article will delve into the mechanisms behind the prime rate, its far-reaching impact, and how you can strategically respond to its fluctuations in the current financial climate.

Understanding the Prime Rate: The Foundation of Lending

The prime rate is not an arbitrary figure plucked from thin air; rather, it is a dynamic benchmark intricately linked to the broader monetary policy set by a nation’s central bank. In the United States, for instance, this role is played by the Federal Reserve, and its influence on the prime rate is paramount. Grasping the definition and calculation of this rate is the first step toward understanding its significance.

Definition and Calculation

The prime rate is formally defined as the interest rate that commercial banks charge their most creditworthy corporate clients. While this specific charge is typically for short-term loans, the prime rate effectively serves as a crucial reference point for a wide array of other lending products. It’s not set by a single entity daily but is instead heavily influenced by the federal funds rate – the target rate set by the Federal Reserve for interbank lending.

Typically, the prime rate is approximately three percentage points above the federal funds rate. For example, if the federal funds rate target range is between 5.25% and 5.50%, the prime rate would likely be 8.50%. This spread accounts for the banks’ operational costs, risk assessment, and profit margins. Banks monitor the federal funds rate and adjust their prime rates accordingly, often within a day or two of a Fed policy change. This means that while individual banks might have slight variations, there is a strong consensus among major financial institutions on what the prevailing prime rate is at any given time. Publications like The Wall Street Journal commonly publish the consensus prime rate, making it a widely accessible piece of financial information.

Key Lenders and Its Application

While the definition points to corporate clients, the prime rate’s real impact stretches far beyond the largest businesses. It serves as the foundational rate for numerous consumer and small business lending products. For consumers, this includes variable-rate products such as:

- Credit Cards: The annual percentage rates (APRs) on most credit cards are directly tied to the prime rate, plus a margin determined by the issuer and the cardholder’s creditworthiness.

- Home Equity Lines of Credit (HELOCs): These revolving lines of credit, secured by a borrower’s home equity, almost always have variable interest rates indexed to the prime rate.

- Adjustable-Rate Mortgages (ARMs): While less common as a direct index than other rates, some ARMs might have components or caps tied indirectly to prime rate movements.

- Personal Loans: Certain variable-rate personal loans can also be indexed to the prime rate.

For small businesses, the prime rate is crucial for:

- Lines of Credit: Many business lines of credit are offered at prime plus a certain percentage, reflecting the business’s risk profile.

- Term Loans: Variable-rate business term loans also frequently use the prime rate as their benchmark.

In essence, if you have a loan with an interest rate that can change over time, there’s a high probability that its fluctuations are a direct consequence of changes in the prime rate. This widespread application makes monitoring the prime rate an essential aspect of managing both personal and business finances effectively.

The Federal Reserve’s Influence: The Architect of Money Costs

To truly grasp the prime rate, one must understand the pivotal role of the Federal Reserve (or equivalent central bank in other nations). The Fed isn’t just an observer; it’s the primary architect of the financial conditions that dictate the cost of money in the economy, and by extension, the prime rate.

The Role of the Federal Funds Rate

The linchpin of the Federal Reserve’s influence is the federal funds rate. This is the target interest rate that commercial banks charge each other for overnight loans of their excess reserves held at the Federal Reserve. While the Fed doesn’t directly set the federal funds rate, it influences it through open market operations – buying or selling government securities – to either add or drain reserves from the banking system. When the Fed raises the target federal funds rate, it signals to banks that borrowing reserves has become more expensive. Banks then pass this increased cost on, primarily by raising their prime rates. Conversely, when the Fed lowers the federal funds rate, banks reduce their prime rates.

The Federal Open Market Committee (FOMC), the Fed’s primary monetary policymaking body, meets eight times a year to assess economic conditions and determine the appropriate target range for the federal funds rate. Their decisions are heavily scrutinized by financial markets worldwide, as they have direct implications for borrowing costs across the economy. The direct relationship between the federal funds rate and the prime rate—typically a 300 basis point (3 percentage point) spread—is one of the most consistent aspects of U.S. monetary policy transmission.

Monetary Policy and Economic Stability

The Fed’s decisions regarding the federal funds rate are not arbitrary; they are carefully calibrated responses to broader economic conditions, all aimed at achieving its dual mandate: maximum sustainable employment and stable prices (i.e., controlling inflation).

- Combating Inflation: When inflation is high, the Fed often raises the federal funds rate. This makes borrowing more expensive, which can cool down economic activity, reduce demand, and thereby help bring inflation under control. A higher federal funds rate translates to a higher prime rate, increasing the cost of loans for consumers and businesses, which can curb spending and investment.

- Stimulating Economic Growth: In times of economic slowdown or recession, the Fed might lower the federal funds rate. This makes borrowing cheaper, encouraging consumers to spend and businesses to invest and expand, thereby stimulating economic growth and job creation. A lower federal funds rate leads to a lower prime rate, reducing the cost of debt and making financial resources more accessible.

Through these adjustments, the Fed attempts to navigate the delicate balance of promoting economic expansion without igniting runaway inflation. The prime rate, as a direct derivative of the federal funds rate, serves as a crucial tool in this monetary policy transmission mechanism, ensuring that the Fed’s directives filter down to the everyday financial lives of Americans.

Who is Affected by Changes in the Prime Rate?

Changes in the prime rate are not merely abstract economic shifts; they have tangible, real-world consequences for a broad spectrum of financial participants. From individual consumers managing household budgets to businesses planning expansion, the prime rate’s movements dictate the cost of capital and influence financial decisions.

Consumer Lending: Credit Cards and HELOCs

For the average consumer, the most immediate and noticeable impact of prime rate changes is often felt through variable-rate debt.

- Credit Cards: The vast majority of credit cards carry variable APRs that are directly tied to the prime rate. When the prime rate increases, the interest rate on your outstanding credit card balances will rise, making it more expensive to carry debt. Conversely, a falling prime rate can provide some relief by reducing interest payments. For those with significant credit card debt, even small changes in the prime rate can translate into noticeable differences in monthly minimum payments and the total cost of borrowing.

- Home Equity Lines of Credit (HELOCs): HELOCs are another significant area of impact. These popular lending products typically have variable interest rates that adjust with the prime rate. Homeowners using HELOCs for renovations, debt consolidation, or other expenses will see their monthly interest payments fluctuate. A rising prime rate means higher payments, which can strain household budgets, while a falling prime rate offers potential savings. Understanding this link is crucial for homeowners considering or already utilizing a HELOC.

Business Loans and Lines of Credit

Businesses, particularly small and medium-sized enterprises (SMEs), are profoundly affected by prime rate changes, as these rates directly impact their operational costs and investment decisions.

- Business Lines of Credit: Many businesses rely on lines of credit for working capital, inventory purchases, or to bridge cash flow gaps. These are almost universally variable-rate products tied to the prime rate. An increase in the prime rate directly raises the cost of borrowing for these essential operational funds, potentially squeezing profit margins and making it more expensive to manage day-to-day operations.

- Variable-Rate Term Loans: While fixed-rate business loans are common, many businesses also utilize variable-rate term loans for equipment purchases, expansion projects, or acquisitions. As the prime rate shifts, the interest payments on these loans will adjust, impacting the company’s financial planning and profitability forecasts. For businesses highly leveraged with variable-rate debt, significant prime rate hikes can pose substantial financial challenges.

Indirect Impacts on Mortgages and Investments

While fixed-rate mortgages are not directly indexed to the prime rate, there are indirect effects and implications for other investment vehicles.

- Mortgages: The prime rate itself doesn’t directly influence 30-year fixed-rate mortgages, which are typically tied to long-term bond yields. However, adjustable-rate mortgages (ARMs) can be indirectly affected. More broadly, when the Fed raises the federal funds rate (and thus the prime rate) to combat inflation, it often leads to a general increase in interest rates across the board, including those for fixed-rate mortgages, albeit through different market mechanisms.

- Savings Accounts and CDs: On the flip side, a rising prime rate often signals a period of higher interest rates across the financial system. This can be beneficial for savers, as banks may offer higher interest rates on savings accounts, money market accounts, and Certificates of Deposit (CDs), making it more attractive to save.

- Investment Markets: Changes in the prime rate (and underlying Fed policy) can significantly impact investment markets. Higher rates can make bonds more attractive relative to stocks, potentially leading to shifts in portfolio allocations. Businesses might also face higher borrowing costs for expansion, which could affect their earnings and stock valuations.

In summary, the prime rate is a critical barometer for the cost of borrowing, shaping financial decisions for individuals and businesses across the economic spectrum.

Current Prime Rate Landscape: Navigating Economic Headwinds

The journey of the prime rate is a reflection of the broader economic environment, heavily influenced by inflation, economic growth, and the Federal Reserve’s response to these forces. To understand “what is the prime rate now,” one must consider the recent past and the prevailing economic narratives.

Recent Movements and Market Expectations

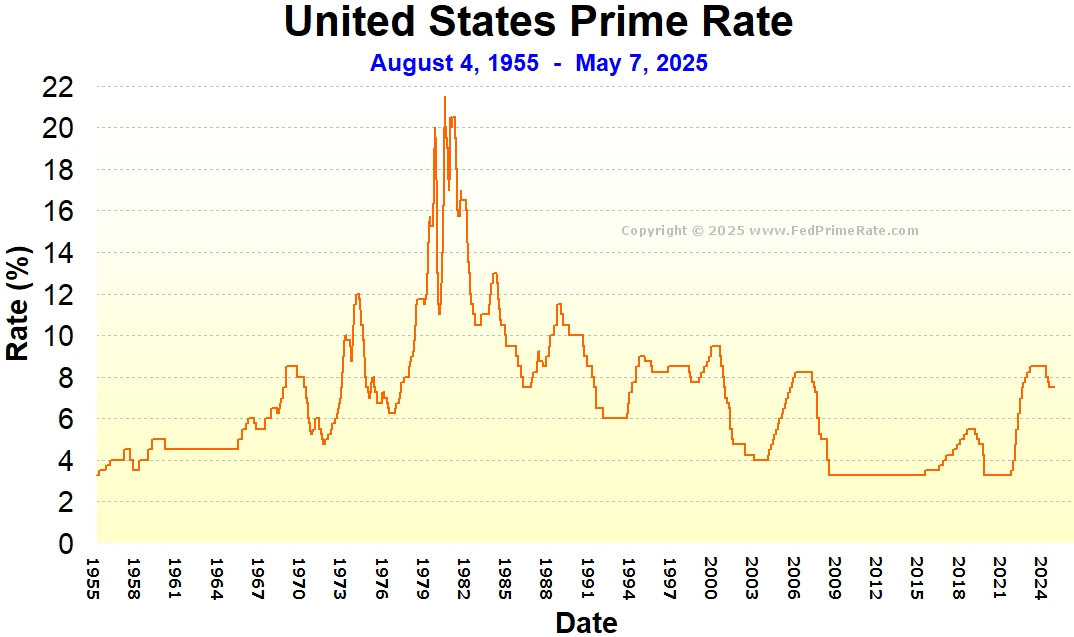

In recent periods, the world has witnessed significant volatility in the prime rate. Following a prolonged period of historically low interest rates in the aftermath of the 2008 financial crisis and further reductions during the COVID-19 pandemic, central banks globally, including the Federal Reserve, embarked on an aggressive path of rate hikes. This began in earnest in 2022 and continued through 2023, primarily as a response to surging inflation. Each increase in the federal funds rate was swiftly mirrored by an equivalent rise in the prime rate, leading to a substantial increase in borrowing costs across the economy.

For example, if the federal funds rate was near 0% for an extended period, the prime rate hovered around 3.25%. A series of rapid 25-basis-point or even 50-basis-point hikes by the Fed could push the federal funds rate significantly higher, causing the prime rate to follow suit, potentially reaching levels not seen in over a decade.

Market expectations are constantly shifting, driven by new economic data, geopolitical events, and forward guidance from central bankers. Investors and analysts closely watch inflation reports (Consumer Price Index, Personal Consumption Expenditures), employment figures, and GDP growth to anticipate the Fed’s next moves. The consensus regarding future rate changes (whether hikes, holds, or cuts) directly influences market sentiment and plays a crucial role in determining the outlook for the prime rate. Currently, the discourse often revolves around the ‘peak’ of the rate hike cycle and the timing of potential future rate cuts, reflecting a belief that inflation may be moderating.

Economic Indicators Driving Decisions

The Federal Reserve’s decisions, which directly impact the prime rate, are data-dependent. Several key economic indicators are scrutinized:

- Inflation: This is arguably the most critical factor. If inflation remains stubbornly high above the Fed’s 2% target, the central bank will likely maintain a restrictive monetary policy, keeping the federal funds rate (and thus the prime rate) elevated. Conversely, sustained evidence of disinflation could open the door for rate cuts.

- Employment Data: The strength of the labor market, reflected in unemployment rates, job growth figures, and wage growth, is another vital indicator. A robust labor market can support higher rates without fear of causing a severe recession, while a weakening job market might prompt the Fed to consider rate cuts to stimulate economic activity.

- Gross Domestic Product (GDP): GDP growth figures provide a broad measure of economic health. Strong economic growth might allow the Fed to maintain higher rates, while signs of a slowdown or recession could necessitate a more accommodative stance.

- Consumer Spending and Business Investment: These indicators reflect demand within the economy. Healthy consumer spending and business investment can be inflationary, influencing the Fed to keep rates higher, whereas a slowdown might push them towards lower rates.

The Fed’s challenge is to balance these often-conflicting indicators to achieve its dual mandate. Each data release contributes to the ongoing debate about the appropriate path for monetary policy, which in turn dictates the trajectory of the prime rate. Staying informed about these economic indicators is key to understanding the prevailing prime rate and anticipating its future direction.

Navigating Prime Rate Fluctuations: Strategies for Financial Resilience

In an environment where the prime rate can shift, often rapidly, financial resilience becomes paramount. Both individuals and businesses must adopt proactive strategies to manage debt and optimize financial resources in response to these changes.

For Personal Finance: Debt Management and Refinancing

Fluctuations in the prime rate have direct implications for personal finance, particularly for those with variable-rate debt. Strategic planning can mitigate negative impacts and capitalize on opportunities.

- Prioritize High-Interest, Variable Debt: When the prime rate is rising, focus on paying down high-interest variable debts first, such as credit card balances and HELOCs. Every dollar paid towards principal on these debts reduces exposure to future interest rate hikes. Consider a “debt avalanche” strategy, where you tackle the highest interest rate debt first, regardless of balance size.

- Consider Debt Consolidation: If you have multiple variable-rate debts, explore consolidating them into a fixed-rate personal loan, a balance transfer credit card with an introductory 0% APR, or a fixed-rate home equity loan (distinct from a HELOC). This locks in your interest rate, providing predictability and potentially lower payments, especially if rates are expected to rise further.

- Refinance Variable-Rate Loans: For existing HELOCs or variable-rate personal loans, investigate refinancing options. If the prime rate has risen significantly, you might consider converting a HELOC into a fixed-rate home equity loan, or refinancing a variable-rate personal loan into a new fixed-rate loan if prevailing fixed rates are more favorable or offer better payment predictability. Conversely, if the prime rate were to drop significantly, refinancing a high fixed-rate loan into a new variable-rate loan might be an option, though this carries future rate risk.

- Build an Emergency Fund: A robust emergency fund provides a buffer against unexpected increases in debt payments, preventing a scramble for funds when rates rise.

For Businesses: Capital Planning and Risk Mitigation

Businesses face unique challenges and opportunities with prime rate changes, requiring careful capital planning and risk management.

- Assess Debt Portfolio: Regularly review your business’s debt portfolio to understand your exposure to variable-rate loans. Identify which loans are tied to the prime rate and calculate the potential impact of various rate hike scenarios on your cash flow and profitability.

- Hedge Interest Rate Risk: For businesses with significant variable-rate debt, consider hedging strategies. This could involve using interest rate swaps or caps to fix or limit the maximum interest rate paid on a portion of your debt. While these instruments come with costs, they provide certainty in an unpredictable rate environment.

- Optimize Cash Flow and Working Capital: A rising prime rate makes borrowing more expensive, so efficient cash flow management becomes even more critical. Optimize inventory, streamline accounts receivable, and negotiate favorable payment terms with suppliers to reduce reliance on costly short-term borrowing.

- Strategic Borrowing Decisions: When planning new capital expenditures or expansions, carefully weigh the pros and cons of fixed-rate versus variable-rate financing. In a rising rate environment, fixed-rate loans offer stability, albeit potentially at a higher initial cost. In a falling rate environment, variable rates might be attractive, but always consider the potential for future increases.

- Re-evaluate Investment Returns: Higher borrowing costs mean that investment projects need to generate higher returns to justify the expense. Businesses should reassess their internal rates of return (IRRs) and hurdle rates for new projects in light of current and anticipated prime rate levels.

By actively monitoring the prime rate and implementing these strategic financial management practices, individuals and businesses can navigate the complexities of changing interest rate environments, ensuring greater financial stability and preparedness.

Conclusion: The Enduring Relevance of the Prime Rate

The question “what is the prime rate now” is far more than a simple inquiry into a single number; it’s a gateway to understanding the dynamic interplay between central bank policy, economic indicators, and the everyday financial realities of millions. As we’ve explored, the prime rate, heavily influenced by the Federal Reserve’s federal funds rate, acts as a foundational benchmark that dictates the cost of a vast array of lending products, from consumer credit cards and home equity lines to crucial business financing.

Its fluctuations, driven by the central bank’s efforts to balance inflation with economic growth, have profound implications. A rising prime rate signifies higher borrowing costs, challenging those with variable-rate debt and potentially slowing economic activity. Conversely, a falling prime rate can stimulate borrowing and investment, providing relief to debtors and fueling expansion. For consumers, this means vigilant management of credit card balances and HELOCs, while for businesses, it necessitates careful capital planning and risk mitigation strategies.

In an ever-evolving financial landscape, staying informed about the current prime rate and the economic forces that shape it is not just an academic exercise but a practical necessity. By understanding its origins, its impact, and developing proactive financial strategies, individuals and businesses can navigate the currents of monetary policy with greater confidence and secure a stronger financial future. The prime rate, therefore, remains an enduring and essential indicator of financial health and opportunity.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.