The prime rate is a foundational metric in the financial world, serving as the benchmark interest rate that commercial banks charge their most creditworthy corporate customers. Its movements ripple through the economy, influencing everything from the cost of a home equity line of credit (HELOC) to a business’s capacity for expansion. Understanding the prime rate, how it’s determined, and its current trajectory is crucial for consumers, investors, and businesses alike to make informed financial decisions. In an ever-evolving economic landscape, staying attuned to this key indicator provides a powerful lens through which to view personal and corporate financial health.

The current prime rate is a dynamic figure, directly influenced by the Federal Reserve’s monetary policy decisions, specifically the federal funds rate. As of the time of this writing and based on the most recent trends, the prime rate is typically 7.00% or 8.50% (acknowledging that this rate can fluctuate and is best confirmed with real-time financial news sources or bank statements, as it usually sits 3% above the lower end of the federal funds target range, which has been in flux over the past year). This rate reflects the culmination of economic data, inflation targets, and the Fed’s ongoing efforts to manage economic growth and stability. To truly grasp its significance, we must deconstruct its components, trace its historical path, and project its potential future impacts.

Deconstructing the Prime Rate: Definition and Determination

The prime rate isn’t an arbitrary number; it’s a carefully calculated figure that underpins a vast array of lending products. Its definition and the mechanism by which it’s determined are fundamental to appreciating its economic power.

The Fundamental Definition

At its core, the prime rate is the interest rate that commercial banks in the U.S. extend to their most creditworthy customers. These are typically large corporations with excellent financial standing and minimal risk of default. While not directly accessible to the average consumer, the prime rate acts as a foundational index for many consumer and small business loans. It’s often used as the base rate for variable-rate loans, meaning your interest rate could be expressed as “prime rate plus X percent” or “prime rate minus Y percent.” This direct linkage makes the prime rate a critical figure for anyone with existing variable-rate debt or considering new financing.

The Federal Funds Rate Connection

The most significant factor influencing the prime rate is the federal funds rate, set by the Federal Open Market Committee (FOMC) of the Federal Reserve. The federal funds rate is the target interest rate at which commercial banks borrow and lend their excess reserves to each other overnight. When the Fed raises or lowers this target rate, banks’ borrowing costs change, which in turn influences the rates they charge their own customers. Historically, the prime rate has maintained a spread of approximately 3 percentage points above the federal funds rate. For instance, if the federal funds rate target is between 5.25% and 5.50%, the prime rate will typically be 8.50%. This consistent relationship highlights the Fed’s dominant role in dictating the overall cost of borrowing in the economy.

How Banks Set Their Prime Rate

While the federal funds rate provides the primary guide, individual banks may slightly adjust their prime rate based on their own cost of funds, competitive pressures, and risk assessment. However, for practical purposes, most major banks in the U.S. tend to move in lockstep, announcing identical prime rate changes shortly after the Federal Reserve adjusts the federal funds rate. This uniformity ensures a relatively consistent lending environment across the banking sector, although slight variations might exist in how banks apply this rate to specific loan products or customer segments. Other factors, such as the overall economic outlook, inflation expectations, and the demand for credit, can also subtly influence banks’ internal decisions regarding their lending rates.

Understanding the Current Prime Rate Landscape

To truly appreciate “what is the prime rate currently,” we must look beyond just the number itself and understand the broader economic context that shapes it. This involves examining the latest figures, the key drivers behind them, and a brief historical perspective.

The Latest Figures and Their Immediate Implications

As previously noted, the current prime rate has largely settled into a range directly reflecting the Federal Reserve’s aggressive rate-hiking cycle that began in early 2022 to combat surging inflation. Following multiple successive increases in the federal funds rate, the prime rate has seen a significant ascent from its historically low levels witnessed during the pandemic. For example, if the federal funds target range is between 5.25% and 5.50%, the prime rate would be 8.50%. This higher rate translates directly to increased borrowing costs for a wide array of variable-rate loans, impacting everything from mortgage payments for HELOCs to credit card interest and business lines of credit. Borrowers with existing variable-rate debt are feeling the pinch of higher monthly payments, while those seeking new credit face a more expensive lending environment than in recent years.

Key Factors Driving Current Rates

The current prime rate is primarily driven by the Federal Reserve’s monetary policy, which is itself a response to prevailing economic conditions. High inflation has been the paramount concern, prompting the Fed to raise rates to cool demand and bring price increases back toward its 2% target. Other crucial factors include:

- Inflation Data: Persistent high inflation figures signal the need for tighter monetary policy, pushing rates higher.

- Employment Figures: A robust labor market, characterized by low unemployment and strong wage growth, can also contribute to inflationary pressures and support higher rates.

- Economic Growth (GDP): Strong GDP growth might indicate an economy running hot, potentially requiring higher rates to prevent overheating.

- Global Economic Conditions: International events, geopolitical tensions, and global supply chain dynamics can influence domestic inflation and economic stability, indirectly affecting the Fed’s stance.

- Market Expectations: The financial markets’ anticipation of future Fed moves also plays a role, as bond yields and other rates adjust in advance of official announcements.

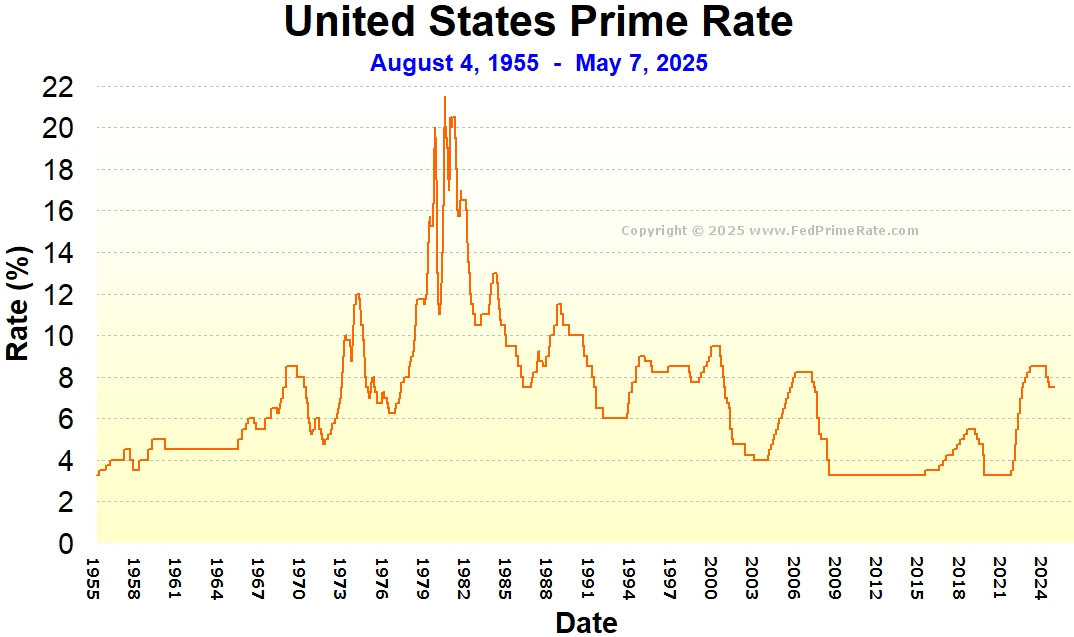

Historical Context: A Brief Look Back

Understanding the current rate requires acknowledging its historical journey. For much of the 2010s, following the 2008 financial crisis, the prime rate remained historically low, hovering near 3.25% as the Fed pursued quantitative easing and near-zero interest rates to stimulate economic recovery. It began a gradual ascent in late 2015 but remained relatively subdued until the COVID-19 pandemic prompted another steep cut back to 3.25%. The rapid increases seen since early 2022 represent one of the most aggressive rate-hiking cycles in decades, contrasting sharply with the long period of low rates. This historical context underscores the cyclical nature of interest rates and highlights the dramatic shift in monetary policy aimed at tackling current economic challenges, particularly inflation.

The Far-Reaching Impact on Your Finances

The prime rate is more than just a number; it’s a pivotal economic lever with tangible consequences for individuals, businesses, and the broader financial system. Its fluctuations directly translate into changes in borrowing costs and, indirectly, influence saving and investment opportunities.

Implications for Borrowers: Variable-Rate Loans and Credit

For the average consumer, the most immediate and significant impact of a changing prime rate is felt through variable-rate loans. These include:

- Home Equity Lines of Credit (HELOCs): These are perhaps the most directly tied to the prime rate. As the prime rate rises, the interest rate on your HELOC increases, leading to higher monthly payments. Conversely, a falling prime rate reduces these payments.

- Credit Cards: While many credit cards have fixed rates for purchases, those with variable annual percentage rates (APRs) are often tied to the prime rate. Even fixed-rate cards can see rate adjustments over time if the prime rate environment shifts significantly, especially for penalty APRs.

- Adjustable-Rate Mortgages (ARMs): The adjustable interest rate component of an ARM is often indexed to the prime rate or another short-term benchmark closely correlated with it. During their adjustment periods, ARMs can see their rates reset higher or lower based on prime rate movements.

- Personal Loans and Auto Loans: While many of these are fixed-rate, some may have variable components or be influenced by the prevailing prime rate environment at the time of origination. Higher prime rates generally mean higher initial interest rates on new loans.

- Small Business Loans: Many lines of credit and short-term loans for small businesses are also directly tied to the prime rate, making financing more or less expensive depending on its trajectory.

In a rising rate environment, borrowers with these products face increased financial strain, needing to allocate more of their budget towards interest payments. This can reduce disposable income and impact spending.

Impact on Businesses: Cost of Capital and Growth

For businesses, especially those reliant on borrowing for operations, expansion, or inventory, the prime rate is a critical determinant of their cost of capital.

- Business Loans and Lines of Credit: Similar to consumers, businesses with variable-rate loans or lines of credit see their interest expenses fluctuate directly with the prime rate. Higher rates mean higher operating costs, which can eat into profit margins.

- Investment and Expansion: When borrowing becomes more expensive, businesses may delay or scale back investment in new equipment, facilities, or research and development. This can slow down growth, reduce job creation, and dampen overall economic activity.

- Working Capital: The cost of maintaining working capital through short-term borrowing increases, potentially straining cash flow for businesses, particularly smaller ones with thinner margins.

- Mergers & Acquisitions: The cost of financing M&A deals rises, potentially leading to fewer transactions or less favorable terms for buyers.

In essence, a higher prime rate makes it more expensive for businesses to function and grow, which can have ripple effects throughout supply chains and labor markets.

The Nuance for Savers and Investors

While borrowers feel the immediate squeeze, the impact on savers and investors is more nuanced, often presenting a silver lining.

- Savings Accounts and Certificates of Deposit (CDs): While not directly indexed to the prime rate, the rates offered on savings accounts, money market accounts, and CDs tend to rise in a higher prime rate environment. Banks can afford to pay more to attract deposits when their lending rates are higher. This means savers can earn more interest on their idle cash.

- Bonds and Fixed Income: Higher interest rates generally lead to lower prices for existing bonds (as newly issued bonds offer more attractive yields), but they also mean higher yields for new bond purchases. Investors looking for income can find more attractive opportunities in fixed-income markets during periods of elevated prime rates.

- Stock Market: The relationship between prime rate and the stock market is complex. Higher rates can increase the cost of doing business for companies (impacting earnings) and make bonds more attractive relative to stocks (drawing capital away). However, rising rates often accompany a strong economy, which can be positive for corporate profits. The initial reaction to rate hikes can be negative, but the long-term impact depends on the reason for the rate hikes (e.g., strong growth vs. inflation control).

- Real Estate: Beyond variable-rate mortgages, a higher prime rate environment tends to cool down the housing market as borrowing for new home purchases becomes more expensive, reducing affordability and demand.

For savers, a rising prime rate can be a welcome development, offering better returns on relatively safe investments. For investors, it requires a strategic re-evaluation of portfolios to adjust for shifting valuations and opportunities across different asset classes.

Navigating a Changing Rate Environment

The prime rate’s fluidity necessitates a proactive approach to financial management. Whether rates are rising or falling, specific strategies can help individuals and businesses optimize their financial position.

Strategies for Borrowers in a Rising Rate Climate

When the prime rate is on an upward trajectory, borrowers must act decisively to mitigate increased costs:

- Refinance Variable-Rate Debt: For HELOCs, ARMs, or business lines of credit tied to the prime rate, consider refinancing into a fixed-rate loan if current fixed rates are appealing and you anticipate further rate hikes. This locks in your payments and provides predictability.

- Pay Down High-Interest Debt: Prioritize aggressively paying down variable-rate debt, especially credit card balances and HELOCs. Reducing the principal amount will lessen the impact of higher interest rates.

- Consolidate Debt: Explore debt consolidation options, potentially moving multiple variable-rate debts into a single loan with a lower, fixed interest rate.

- Review Credit Card Terms: Understand if your credit card APR is variable and how it’s indexed. If so, consider transferring balances to cards with fixed rates or lower promotional rates if possible.

- Budget Adjustment: Re-evaluate your household or business budget to account for potentially higher debt service payments. Cut discretionary spending where necessary to free up funds.

- Delay Non-Essential Borrowing: If possible, postpone taking on new variable-rate debt until rates stabilize or begin to decline.

Capitalizing on Falling Rates

While rising rates pose challenges, a declining prime rate environment offers opportunities, especially for borrowers:

- Refinance Fixed-Rate Debt: If you have fixed-rate debt (like a mortgage or personal loan) from a period when rates were higher, a falling prime rate often signals lower overall market rates, making refinancing to a lower fixed rate an attractive option to reduce monthly payments.

- Re-evaluate New Borrowing: If you’re planning a major purchase requiring a loan (e.g., a home, car, or business equipment), falling rates can make financing significantly cheaper. It might be an opportune time to take on new debt for strategic investments.

- Open New Lines of Credit: Businesses may find it advantageous to establish or expand lines of credit when borrowing costs are lower, providing flexible capital at an economical rate for future needs.

- Reconsider Variable-Rate Products: While caution is generally advised, in a clearly falling rate environment, some borrowers might consider variable-rate products if they believe rates will continue to decline, benefiting from lower payments. However, this carries the inherent risk of future rate reversals.

- Optimize Savings: While falling rates mean lower returns on new savings accounts and CDs, existing CDs might still offer competitive rates. It’s a good time to review your overall savings strategy and potentially explore higher-yielding, though potentially riskier, investment options if your risk tolerance allows.

The Role of Financial Planning

Regardless of the rate environment, sound financial planning is paramount. This involves:

- Regular Review: Periodically review your debt portfolio, savings accounts, and investment strategy in light of current economic conditions and prime rate movements.

- Stress Testing: Consider how your finances would fare under different rate scenarios (e.g., if rates rose by another 1-2%).

- Professional Advice: Consult with a financial advisor to develop a personalized strategy that aligns with your financial goals and risk tolerance, especially in volatile rate environments.

- Building an Emergency Fund: A robust emergency fund provides a buffer against unexpected expenses and allows you to avoid high-interest borrowing if income streams are disrupted or debt payments rise.

By anticipating and adapting to changes in the prime rate, individuals and businesses can protect their financial well-being and leverage opportunities for growth.

Staying Informed and Preparing for the Future

In a financial world characterized by constant change, staying informed about the prime rate and its underlying economic drivers is not just prudent; it’s essential. The future trajectory of the prime rate will continue to shape financial decisions and economic outcomes for years to come.

Reliable Sources for Rate Information

Accessing timely and accurate information is the first step in effective financial management related to the prime rate. Reliable sources include:

- The Federal Reserve: The official website of the Federal Reserve (federalreserve.gov) publishes the target range for the federal funds rate and provides detailed minutes and transcripts of FOMC meetings, offering insights into their decision-making process.

- Major Financial News Outlets: Reputable financial news organizations like The Wall Street Journal, Bloomberg, Reuters, and the Financial Times consistently report on Fed decisions and analyze their implications for the prime rate and broader markets.

- Major Bank Websites: Large commercial banks often publish their prime rate directly on their websites, typically updating it immediately after the Fed’s announcements.

- Financial Data Providers: Services like FRED (Federal Reserve Economic Data) by the Federal Reserve Bank of St. Louis offer historical data and charts for various interest rates, including the prime rate.

Regularly consulting these sources will ensure you have the most up-to-date information to guide your financial planning.

Long-Term Economic Outlook and Projections

Looking ahead, the prime rate’s future will be dictated by the Federal Reserve’s ongoing battle against inflation, economic growth figures, and the health of the labor market. While predictions are inherently uncertain, economists and central bankers generally project potential scenarios:

- Inflation Control: If inflation continues to moderate and moves closer to the Fed’s 2% target, the pressure for further rate hikes would diminish. This could lead to a period of rate stability or even eventual rate cuts.

- Economic Slowdown/Recession: A significant economic downturn or recession could prompt the Fed to lower rates to stimulate growth, thereby reducing the prime rate.

- Sustained Growth: Conversely, if the economy remains robust without triggering excessive inflation, the Fed might maintain rates at a higher level for longer to ensure price stability.

- Global Factors: Geopolitical events, shifts in global trade, and economic conditions in other major economies can also influence the Fed’s decisions and, by extension, the prime rate.

Financial analysts widely debate the timing and magnitude of any future rate changes. Some anticipate a “higher for longer” scenario, where rates remain elevated for an extended period, while others foresee rate cuts later in the year or the following year as inflation cools. Keeping an eye on these projections from various reputable sources can help shape your long-term financial strategies.

Proactive Financial Management

Ultimately, an informed understanding of the prime rate empowers proactive financial management. This involves:

- Regular Portfolio Review: Periodically assess your investments and debt structure to ensure they remain aligned with the current rate environment and your financial goals.

- Contingency Planning: Develop a financial plan that considers various interest rate scenarios. What if rates unexpectedly rise further? What if they fall rapidly?

- Debt Prioritization: Continue to prioritize paying down high-interest, variable-rate debt, which always offers a guaranteed return equal to the interest rate saved.

- Savings Optimization: Seek out the best available rates for your savings vehicles, adjusting as the market shifts.

- Professional Consultation: Engage with financial advisors or banking professionals to discuss how prime rate movements specifically impact your unique financial situation and to explore tailored strategies.

By continuously monitoring the prime rate, understanding its economic underpinnings, and adopting a proactive stance, you can effectively navigate the complexities of the financial landscape and ensure your money works optimally for you, irrespective of economic shifts. The prime rate is a powerful signal, and knowing how to read it is a key skill for financial success.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.