Understanding the prime rate is not merely an academic exercise for economists; it’s a critical component of personal finance and business strategy that directly influences the cost of borrowing and the availability of credit. As of today, the prime rate stands as a powerful indicator of the broader economic landscape, reflecting the Federal Reserve’s monetary policy and impacting everything from your credit card interest to the terms of a new business loan. For anyone navigating the complexities of modern finance, grasping the prime rate’s definition, its current standing, and its far-reaching implications is essential for informed decision-making.

This comprehensive guide will demystify the prime rate, explore its intricate relationship with the Federal Funds Rate, detail its impact on various financial products for both consumers and businesses, and equip you with the knowledge to understand its current trajectory and future implications.

Understanding the Prime Rate: A Cornerstone of Lending

At its core, the prime rate is the interest rate that commercial banks charge their most creditworthy corporate customers. It serves as a benchmark for a vast array of variable-rate financial products and represents the lowest possible lending rate available to the least risky borrowers. While it’s often quoted as a single number, its influence cascades through the entire financial system, affecting the borrowing costs for millions of individuals and businesses.

Defining the Prime Rate

The prime rate is effectively a baseline. For individual consumers or small businesses, the interest rate they receive on loans will typically be quoted as “prime rate plus X percent.” For example, if the prime rate is 8.50%, a credit card might charge 8.50% + 5% = 13.50% APR. This “X percent” (or spread) reflects the borrower’s creditworthiness, the type of loan, and the lender’s risk assessment. The higher the risk perceived by the lender, the larger that spread will be above the prime rate. It is a dynamic rate, meaning it doesn’t stay constant but adjusts in response to broader economic shifts.

The Federal Funds Rate Connection

The prime rate isn’t arbitrarily set by individual banks; it’s overwhelmingly influenced by the Federal Funds Rate. The Federal Funds Rate is the target rate set by the Federal Open Market Committee (FOMC) of the U.S. Federal Reserve, representing the interest rate at which depository institutions lend balances to each other overnight. When the Fed raises or lowers the Federal Funds Rate, banks’ cost of borrowing from each other changes almost immediately.

Historically, the prime rate has moved in lockstep with the upper bound of the Federal Funds Rate target range, typically maintaining a spread of approximately 300 basis points (3 percentage points) above it. This consistent relationship makes the prime rate a predictable indicator of the Fed’s monetary policy. If the Fed raises the Federal Funds Rate to curb inflation, the prime rate will almost certainly follow suit, making borrowing more expensive across the board. Conversely, a reduction in the Federal Funds Rate, often aimed at stimulating economic growth, will lead to a lower prime rate and cheaper credit.

Who Sets the Prime Rate?

While the Federal Reserve indirectly dictates the prime rate through its Federal Funds Rate decisions, it’s actually individual commercial banks that officially “set” their own prime rates. However, due to market competition and the dominance of major financial institutions, these rates tend to converge very quickly. The Wall Street Journal Prime Rate, for example, is a widely cited benchmark representing the prime rate charged by at least 70% of the nation’s 10 largest banks. This effectively creates a de facto standard that other banks then follow. Therefore, when people ask “what is the prime rate,” they are usually referring to this consensus rate, which faithfully mirrors the Fed’s policy.

The Prime Rate’s Impact on Your Finances

The prime rate’s fluctuations have tangible consequences for both individual consumers and businesses. Its movements can significantly alter the cost of existing variable-rate debt and influence the terms of new loans, demanding attention from anyone managing their financial health.

Variable-Rate Loans: Credit Cards and HELOCs

Perhaps the most direct impact of the prime rate is felt by holders of variable-rate financial products. Credit cards almost universally feature variable annual percentage rates (APRs) tied to the prime rate. If the prime rate increases by 0.25%, your credit card APR will likely increase by the same amount, making your monthly interest payments higher if you carry a balance. Similarly, Home Equity Lines of Credit (HELOCs) are another common financial product with rates directly linked to the prime rate. A rising prime rate means higher interest payments on your HELOC balance, potentially stretching your household budget. For those with substantial balances on these instruments, monitoring the prime rate is crucial for budgeting and debt management strategies.

Business Loans and Lines of Credit

For businesses, especially small and medium-sized enterprises (SMEs), the prime rate is a cornerstone for the cost of capital. Most business loans, particularly revolving lines of credit, are structured with interest rates tied to the prime rate. An increase in the prime rate directly translates to higher interest expenses for businesses relying on these credit lines to manage cash flow, finance operations, or fund expansion. This can squeeze profit margins, reduce investment capacity, and even impact hiring decisions. Conversely, a lower prime rate provides relief, making working capital cheaper and encouraging business investment.

Mortgages and Auto Loans: Indirect Influence

While fixed-rate mortgages and auto loans are not directly tied to the prime rate, its influence is still felt indirectly. Fixed-rate mortgages are more closely linked to bond yields, particularly the 10-year Treasury yield, which often moves in anticipation of or reaction to Federal Reserve actions. Since the Fed’s actions on the Federal Funds Rate (and thus the prime rate) aim to influence the broader economy and inflation, they indirectly affect bond yields and, consequently, fixed mortgage rates. Adjustable-Rate Mortgages (ARMs), however, can have their rates tied to various indexes, some of which may be influenced by the prime rate, or even directly to the prime rate after an initial fixed period. For auto loans, while fixed-rate options are common, the general cost of borrowing in the economy, heavily influenced by the prime rate, can affect the base rates offered by lenders.

Why Small Businesses are Particularly Sensitive

Small businesses often operate with tighter margins and less access to diverse financing options compared to large corporations. Their reliance on lines of credit and short-term loans, which are frequently prime rate-indexed, makes them exceptionally sensitive to changes. A sudden increase in the prime rate can significantly escalate their operating costs, making it harder to manage inventory, make payroll, or invest in growth. This sensitivity underscores why small business owners must stay acutely aware of prime rate movements and factor them into their financial planning and risk management strategies.

Where to Find the Current Prime Rate and What It Means Now

Knowing the current prime rate is essential for making informed financial decisions. Fortunately, this information is readily accessible, and understanding its current context is key to interpreting its implications.

Real-Time Information Sources

The most reliable and frequently updated source for the prime rate is the Wall Street Journal Prime Rate. Major financial news outlets, bank websites, and financial data providers also widely publish this rate. Typically, when the Federal Reserve makes a decision on the Federal Funds Rate, the prime rate adjusts within a day or two, reflecting the new monetary policy stance. It’s crucial to check current sources, as the rate can change multiple times within a year depending on the Fed’s schedule of FOMC meetings and any ad-hoc policy adjustments. For instance, a quick search on a reputable financial news site or your bank’s lending page will typically display the most up-to-date prime rate.

Analyzing the Current Economic Climate

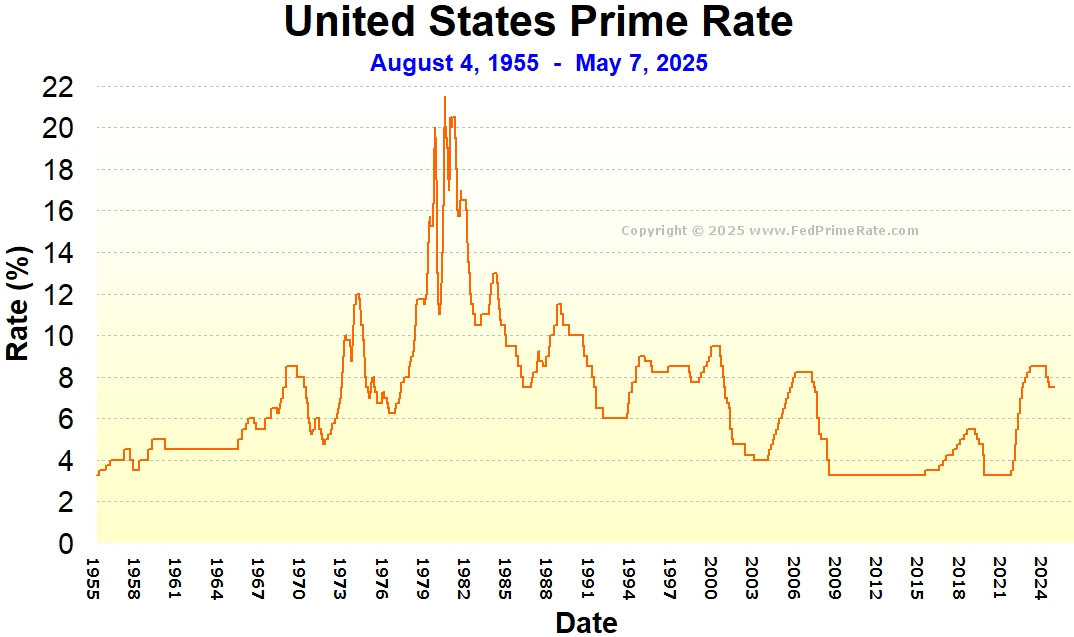

As of today, the prime rate reflects the Federal Reserve’s ongoing efforts to manage inflation and maintain economic stability. After a period of historically low rates, the Fed embarked on an aggressive series of rate hikes to combat elevated inflation. This has led to a significantly higher prime rate compared to recent years. The current elevated prime rate signals a “tight” monetary policy environment, where the cost of borrowing is intentionally higher to cool down economic activity and bring inflation back to the Fed’s target. This means that borrowing money for homes, cars, or business expansion is more expensive than it was just a few years ago.

Recent Trends and Federal Reserve Actions

Over the past two years, we have seen the Federal Funds Rate (and consequently the prime rate) rise substantially from near-zero levels. This period marked one of the most rapid tightening cycles in decades. The Fed’s strategy has been to incrementally increase rates, assess the economic impact, and then decide on further adjustments. While the pace of rate hikes has slowed, or even paused, in recent months, the current elevated level of the prime rate reflects the cumulative effect of these actions. The market is constantly speculating on whether the Fed will hold rates steady, implement further hikes, or begin to cut rates in the future, all of which will directly influence the prime rate’s trajectory. These decisions are heavily dependent on incoming economic data, particularly inflation reports, employment figures, and broader economic growth indicators.

Navigating a Shifting Prime Rate Environment

A dynamic prime rate environment demands proactive financial management. Both consumers and businesses need strategies to mitigate risks and capitalize on opportunities presented by changing borrowing costs.

Strategies for Consumers

For consumers, understanding the current prime rate is the first step. If you have variable-rate debt like credit card balances or HELOCs, evaluate the impact of the current and potentially future prime rate increases on your budget. Consider strategies such as:

- Aggressive Debt Paydown: Prioritize paying down high-interest variable-rate debt while rates are high or expected to rise further.

- Debt Consolidation/Refinancing: Explore options to consolidate variable-rate debt into a fixed-rate personal loan, or if applicable, refinance a HELOC into a fixed-rate home equity loan, if rates appear to be peaking.

- Building an Emergency Fund: A robust emergency fund can reduce reliance on credit cards or HELOCs for unexpected expenses, insulating you from rising interest costs.

- Negotiating Rates: Don’t hesitate to contact your credit card company or lender to inquire about lower rates, especially if you have an excellent credit history.

Business Planning in Volatile Times

Businesses face similar, but often more complex, challenges. A rising prime rate directly impacts operational costs and strategic planning. Key strategies include:

- Cash Flow Management: Optimize cash flow to reduce reliance on lines of credit, which become more expensive as the prime rate rises.

- Fixed-Rate Financing: Explore fixed-rate loan options for long-term investments or significant capital expenditures to lock in predictable interest payments.

- Hedging Strategies: Larger businesses might consider interest rate swaps or other hedging instruments to mitigate the risk of rising rates on existing variable-rate debt.

- Pricing Adjustments: Review pricing strategies for products and services to ensure they adequately cover increased borrowing costs, without alienating customers.

- Scenario Planning: Model different interest rate scenarios to understand their potential impact on profitability and liquidity, preparing for various economic outcomes.

The Role of Financial Advisors

Navigating a complex interest rate environment can be daunting. Engaging with a qualified financial advisor or business consultant can provide invaluable guidance. They can help you assess your current debt portfolio, identify potential risks, and develop tailored strategies for debt management, investment, and financial planning that align with your goals and risk tolerance, taking into account the current and projected prime rate environment.

Looking Ahead: The Future of the Prime Rate and Its Implications

Predicting the future path of the prime rate requires careful attention to economic indicators and the Federal Reserve’s communications. While no one can forecast with absolute certainty, understanding the factors at play allows for better preparation.

Economic Indicators to Watch

The prime rate’s future trajectory will primarily hinge on the Federal Reserve’s assessment of:

- Inflation Data: The Consumer Price Index (CPI) and Personal Consumption Expenditures (PCE) price index are key measures. If inflation remains stubbornly high, the Fed may maintain elevated rates or even consider further hikes.

- Employment Data: Job growth, unemployment rates, and wage growth influence the Fed’s view on economic strength and potential inflationary pressures. A strong labor market might allow the Fed to keep rates higher for longer.

- GDP Growth: Overall economic expansion or contraction helps the Fed gauge the impact of its monetary policy on real economic activity.

- Geopolitical Events: Global events can introduce uncertainty, impact supply chains, and influence energy prices, all of which can affect inflation and the Fed’s decisions.

Potential Scenarios and Their Impact

- “Higher for Longer”: If inflation proves persistent, the Fed might keep the prime rate at its current elevated level for an extended period. This implies continued higher borrowing costs, potentially slowing economic growth further and increasing pressure on variable-rate borrowers.

- Rate Cuts: If inflation demonstrably cools and/or the economy shows significant signs of weakening (e.g., recession), the Fed might begin to lower the Federal Funds Rate, leading to a decreasing prime rate. This would offer relief to borrowers, stimulate lending, and potentially boost economic activity.

- Further Hikes: In a less likely but possible scenario of re-accelerating inflation, the Fed could resume rate hikes, pushing the prime rate even higher. This would signal a more challenging economic environment with greater financial strain.

Long-Term Financial Planning Considerations

Regardless of the immediate future, understanding the prime rate’s foundational role in the economy reinforces the importance of long-term financial planning. Building a robust financial foundation means:

- Maintaining a Strong Credit Score: A high credit score will always ensure you qualify for the best possible rates, regardless of where the prime rate stands.

- Diversifying Investments: Don’t put all your eggs in one basket. A diversified investment portfolio can weather different interest rate environments.

- Minimizing Variable-Rate Debt: Where possible, prioritize fixed-rate debt or reduce reliance on variable-rate products to mitigate exposure to interest rate volatility.

- Regular Financial Reviews: Periodically review your budget, debt, and investment strategies to adapt to changing economic conditions, including movements in the prime rate.

In conclusion, the prime rate, as of today and moving forward, is more than just a number; it is a vital barometer of economic health and a direct determinant of the cost of money. By understanding its mechanics, its current status, and its potential future, individuals and businesses can better navigate their financial landscapes, make informed decisions, and secure their financial well-being.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.