In the high-stakes world of medical education, the Medical College Admission Test (MCAT) is often viewed as a purely academic hurdle. However, for the savvy pre-medical student, the MCAT is less of a biology exam and more of a critical financial instrument. When we ask, “What is the perfect MCAT score?” the answer isn’t simply 528—the theoretical maximum. Instead, the “perfect” score is the one that maximizes your Return on Investment (ROI), minimizes student debt, and secures a seat in a program that aligns with your long-term wealth-building goals.

In this analysis, we will treat the MCAT as a capital investment. By understanding the financial implications of your score, from scholarship eligibility to future specialty access, you can approach the exam with the mindset of a financial strategist rather than just a student.

The ROI of a High MCAT Score: Beyond the Percentile

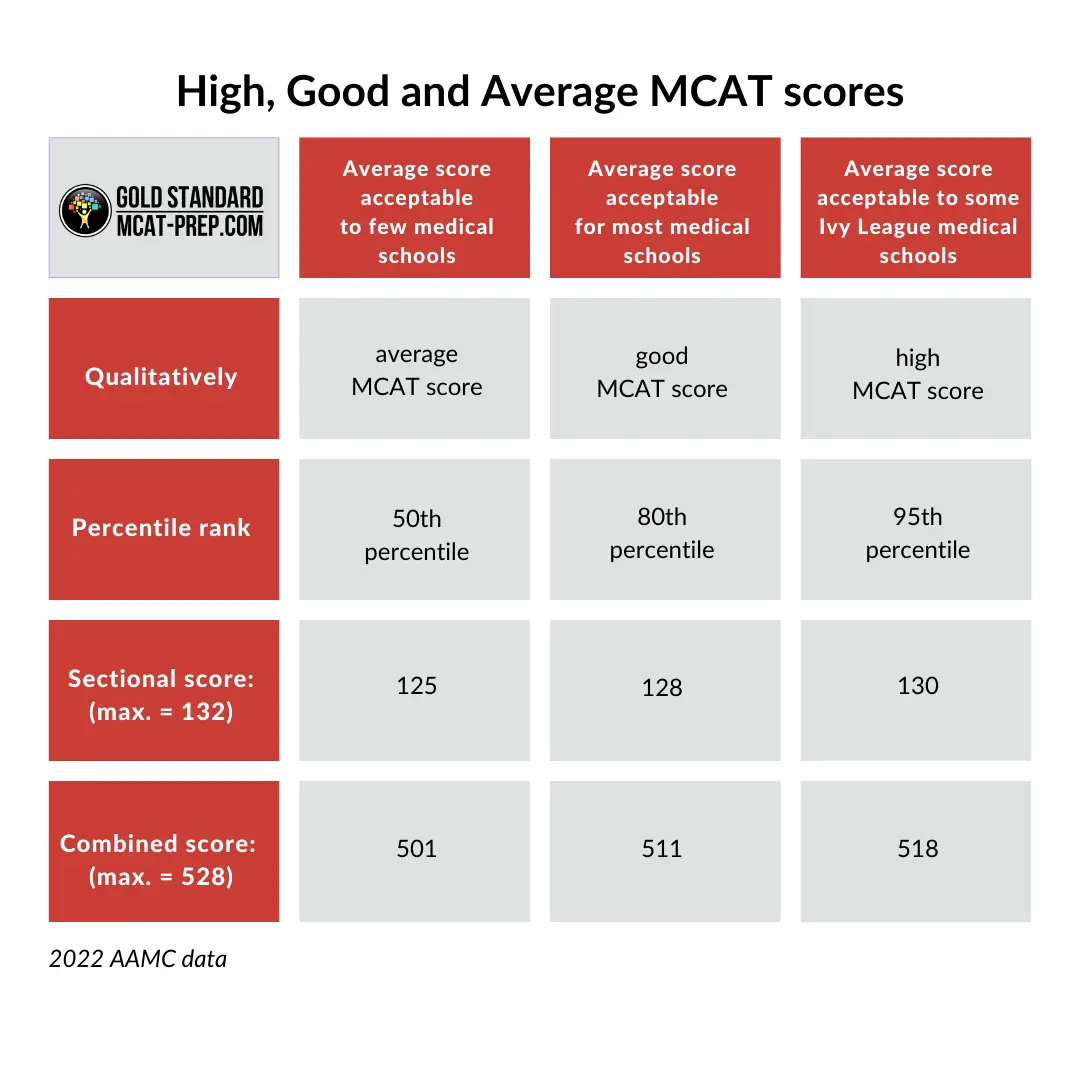

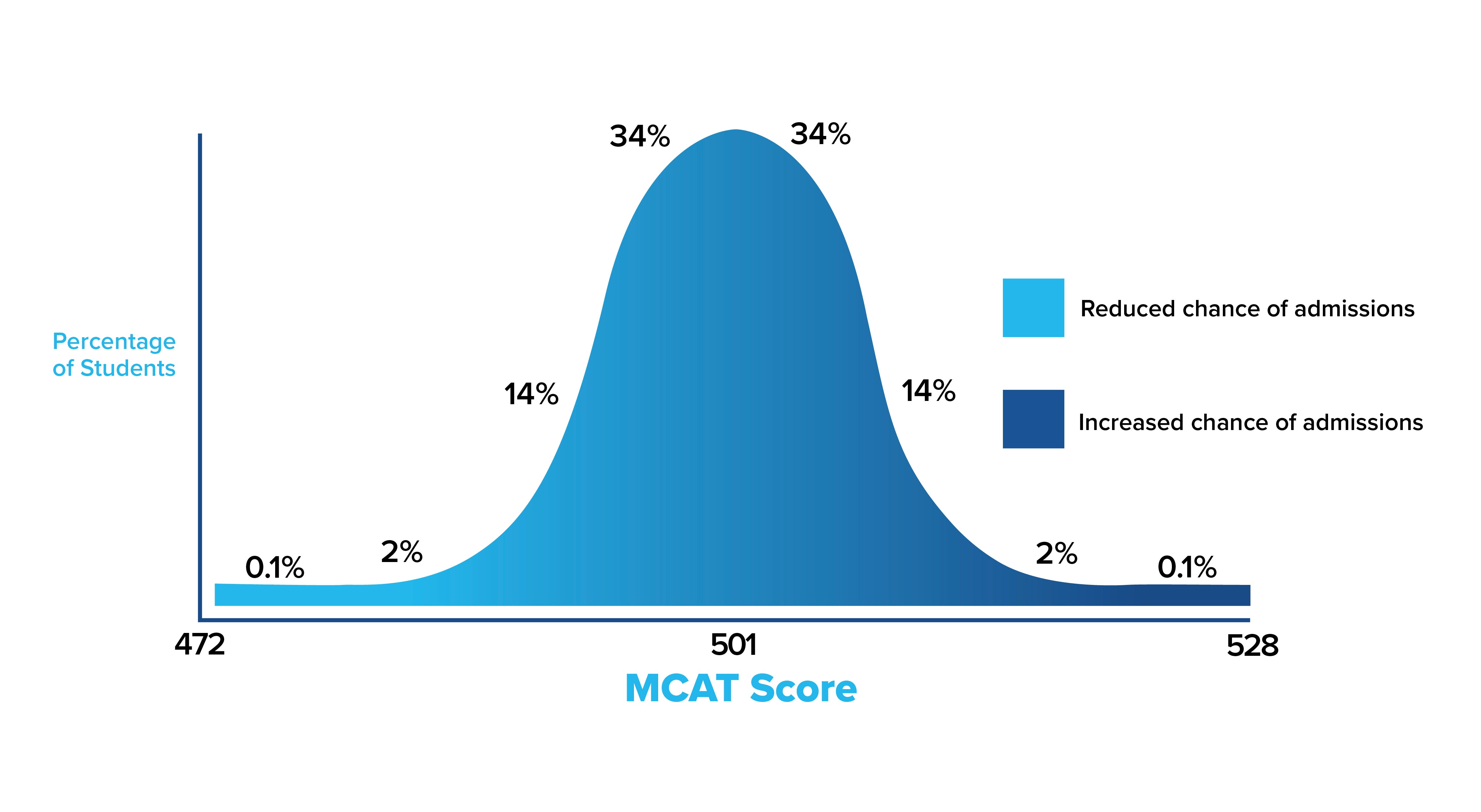

To a statistician, a 528 is perfect. To a financial planner, the “perfect” score is the threshold at which the marginal benefit of additional studying begins to diminish relative to the financial rewards. In the current medical school landscape, a score in the 95th percentile or higher (roughly 518+) acts as a massive leverage point for your personal balance sheet.

Merit-Based Scholarships and Debt Reduction

The average medical student graduates with over $200,000 in debt. At current interest rates, this can balloon into a half-million-dollar liability over the course of a career. However, a “perfect” MCAT score serves as the primary key to merit-based institutional scholarships. Many top-tier private medical schools and several state institutions use MCAT scores as a primary filter for full-tuition or partial-tuition waivers.

If an additional 100 hours of studying raises your score from a 510 to a 520, and that 520 secures a $150,000 scholarship, your “hourly rate” for studying is $1,500 per hour. From a personal finance perspective, there is no side hustle or entry-level job on earth that offers a better tax-free return on your time.

The Cost of Retaking vs. the Value of a First-Time High Score

Every time a student sits for the MCAT, they incur direct costs (registration fees, travel, and materials) and indirect costs (opportunity costs of lost wages). A “perfect” score on the first attempt is a massive cost-saving measure. Retaking the exam not only doubles your direct expenses but can delay your application cycle by an entire year. In the world of physician earnings, a one-year delay represents the loss of a year of attending-level salary—anywhere from $250,000 to $600,000 depending on the specialty. Therefore, the perfect score is the one that allows you to apply early and enter the workforce as soon as possible.

Strategic Investment: The Budgeting Side of MCAT Preparation

Achieving a high score requires capital. Just as a business requires R&D spending to launch a successful product, a pre-med student must view MCAT prep as a capital expenditure. The challenge lies in optimizing this spend to ensure the highest possible “yield” on the score.

Analyzing the Cost-Benefit of Premium Prep Courses

The market for MCAT preparation is worth hundreds of millions of dollars. With courses ranging from $1,500 to $10,000 (for private tutoring), students must perform a cost-benefit analysis. A “perfect” score doesn’t necessarily require the most expensive course, but it does require the most effective tools.

Investing in high-quality question banks (like UWorld) and official AAMC practice materials is non-negotiable for those seeking a top-tier score. These resources are high-yield assets. Conversely, expensive “guaranteed” classroom courses often provide diminishing returns for self-motivated learners. To manage your budget, treat your prep materials as a diversified portfolio: allocate the bulk of your funds to high-utility practice questions and a smaller portion to content review.

Opportunity Costs of Study Time

One of the most overlooked financial aspects of the MCAT is the opportunity cost. If you are a full-time student or a working professional, the three to six months spent studying for a “perfect” score are months where your earning potential is limited.

For those in the “Money” mindset, it is often more efficient to work fewer hours and take on a small amount of “good debt” (or use savings) to focus entirely on the exam. If focused study leads to a score that saves you $100k in future loans, the $5,000 in lost wages during your study months is a negligible expense. The “perfect” score is achieved when you find the equilibrium between your current income needs and your future net worth.

Institutional Prestige and Future Earning Potential

While all MDs and DOs are legally allowed to practice medicine, the “prestige” of the institution you attend can have a measurable impact on your career’s financial trajectory. A “perfect” MCAT score is the currency used to “buy” your way into elite institutions.

Top-Tier Schools and Specialty Access

High-scoring students have a statistically higher chance of matching into “competitive” (read: high-paying) specialties. Specialties like Orthopedic Surgery, Dermatology, and Cardiology often have high income floors and ceilings. These residencies frequently filter applicants based on the prestige of their medical school and their standardized test-taking history.

While a high MCAT score doesn’t guarantee a $500,000 salary, it opens the door to the institutions that provide the best networking, research opportunities, and residency placement statistics. In this sense, the perfect MCAT score is an investment in “career optionality.” It gives you the widest range of choices, allowing you to choose a career path based on passion or profit, rather than being limited by your academic standing.

Long-term Financial Planning for Physicians

The financial life of a physician is back-loaded. Most doctors do not begin earning a significant income until their early 30s. A high MCAT score that leads to a debt-free medical education allows a physician to begin investing in their 20s or early 30s rather than spending a decade “digging out of a hole.” Using the power of compound interest, a student who graduates debt-free because of a 99th-percentile MCAT score could end up with millions of dollars more in retirement savings than a peer who carries heavy debt into their middle age.

Navigating the Financial Barriers to Entry

It is a harsh reality that the road to a “perfect” score is paved with financial barriers. However, identifying these barriers and utilizing available financial tools can help students from all economic backgrounds achieve their goals.

Fee Assistance Programs and Resource Optimization

The AAMC offers a Fee Assistance Program (FAP) for students who meet certain income requirements. This program significantly reduces the cost of the exam and provides free prep materials. From a financial management perspective, applying for FAP is the first “win” a student can achieve. It reduces the “barrier to entry” and increases the net profit of the endeavor.

For those who do not qualify for FAP, resource optimization is key. Using “open-source” or low-cost materials, such as Khan Academy or used prep books from previous years, can help maintain a lean budget while striving for a top score. The goal is to minimize the “cost of goods sold” (the cost of the score) while maximizing the “sale price” (the scholarship or school placement).

Crowdfunding and Alternative Financing for Test Takers

In recent years, we have seen an increase in students using platforms like GoFundMe or seeking private “educational investors” (often family members or community organizations) to fund their MCAT journey. While unconventional, this represents a sophisticated understanding of capital raising. If a student can pitch their potential as a future physician to secure $3,000 for a prep course that results in a $200,000 scholarship, they have successfully navigated a complex financial transaction.

Conclusion: Redefining “Perfect” for Your Personal Ledger

So, what is the perfect MCAT score?

In the world of finance and wealth building, the perfect MCAT score is the one that facilitates your entry into medical school with the lowest possible debt load and the highest possible future earnings ceiling.

For some, a 512 is “perfect” because it secures a spot in a state school with low tuition, allowing for a high lifestyle-to-debt ratio. For others, only a 522+ will do, as it serves as the prerequisite for the merit-based full rides at elite private universities.

When you sit down to study, don’t just think about amino acids and physics equations. Think about your future net worth. Think about the hundreds of thousands of dollars in interest you can avoid. Treat your MCAT preparation as the most important financial investment of your young life. If you do, you won’t just earn a high score—you’ll secure a foundation for lifelong financial independence.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.