Navigating the complexities of state taxation is a cornerstone of sound financial management. For residents, business owners, and investors in North Carolina, the tax landscape has undergone a radical transformation over the last decade. Once known for having some of the highest personal and corporate income tax rates in the Southeast, North Carolina has shifted toward a simplified, flat-tax model designed to spur economic growth and simplify compliance.

Understanding “what is the NC state tax” requires looking beyond a single number. It involves a holistic view of individual income tax, corporate obligations, sales and use taxes, and local property levies. This guide provides an in-depth analysis of the North Carolina tax structure, offering the professional insights necessary for effective personal finance and business planning.

The North Carolina Individual Income Tax Landscape

For the majority of North Carolinians, the most direct interaction they have with the state’s fiscal policy is through the individual income tax. Unlike the federal government, which uses a progressive tax bracket system, North Carolina utilizes a flat tax rate. This means that regardless of whether you earn $50,000 or $500,000, your state tax rate remains the same.

The Shift to a Flat Tax Rate

The hallmark of North Carolina’s 2013 tax reform was the elimination of the multi-tiered progressive system in favor of a flat tax. As of 2024, the individual income tax rate is 4.5%. However, it is important for taxpayers to note that legislative triggers are in place to reduce this rate further over the coming years, provided the state meets certain revenue targets. This downward trajectory is a key component of the state’s strategy to attract high-net-worth individuals and skilled professionals.

From a personal finance perspective, a flat tax simplifies withholding and quarterly estimated payments. Taxpayers no longer have to worry about “bracket creep,” where a raise or a bonus pushes them into a higher tax percentage.

Standard Deductions and Personal Exemptions

While the tax rate is flat, the North Carolina Department of Revenue (NCDOR) allows for a significant standard deduction, which reduces the portion of income subject to taxation. For the 2024 tax year, the standard deduction is $12,750 for single filers and $25,500 for those married filing jointly.

It is vital to note that North Carolina does not allow most itemized deductions found on federal returns, such as charitable contributions or medical expenses, with very limited exceptions for home mortgage interest and real estate taxes (capped at certain levels). Furthermore, North Carolina does not offer a personal exemption for the taxpayer, their spouse, or dependents, having replaced these with the increased standard deduction and a specific child tax credit.

Corporate and Business Tax Obligations in North Carolina

For entrepreneurs and corporate executives, North Carolina’s business tax climate is often cited as one of the most competitive in the United States. The state’s fiscal policy is explicitly designed to incentivize capital investment and job creation through the systematic reduction of corporate burdens.

The Phase-Out of Corporate Income Tax

North Carolina currently maintains a corporate income tax rate of 2.5%, which is among the lowest in the nation for states that levy such a tax. However, the most striking aspect of the state’s business finance policy is the planned total elimination of this tax. According to current legislation, the corporate income tax is scheduled to be phased out entirely by 2030.

This transition has profound implications for business strategy. For C-Corporations, this means a significant increase in net profitability over the long term. For S-Corporations and LLCs, where income “flows through” to the individual owners, the benefits are realized through the lowering individual flat tax rates discussed previously.

The Franchise Tax and its Impact

While the income tax is being phased out, businesses must still navigate the North Carolina Franchise Tax. This is an “excise” tax imposed on corporations for the privilege of doing business or for the privilege of existing as a corporation in the state.

The tax is generally calculated based on the greatest of three bases:

- The corporation’s net worth.

- 55% of the appraised value of all real and tangible personal property in the state.

- The corporation’s actual investment in tangible property in the state.

For many small to mid-sized businesses, the Franchise Tax can feel more burdensome than the income tax because it is levied even if the company does not turn a profit. Business owners must work closely with financial advisors to ensure they are optimizing their balance sheets to manage this specific liability.

Sales and Use Taxes in the Tar Heel State

Sales and use taxes represent a major revenue stream for both the state and local governments. From a consumer’s standpoint, these are the taxes paid at the point of sale; from a business perspective, they represent a significant compliance and collection responsibility.

State vs. Local Sales Tax Rates

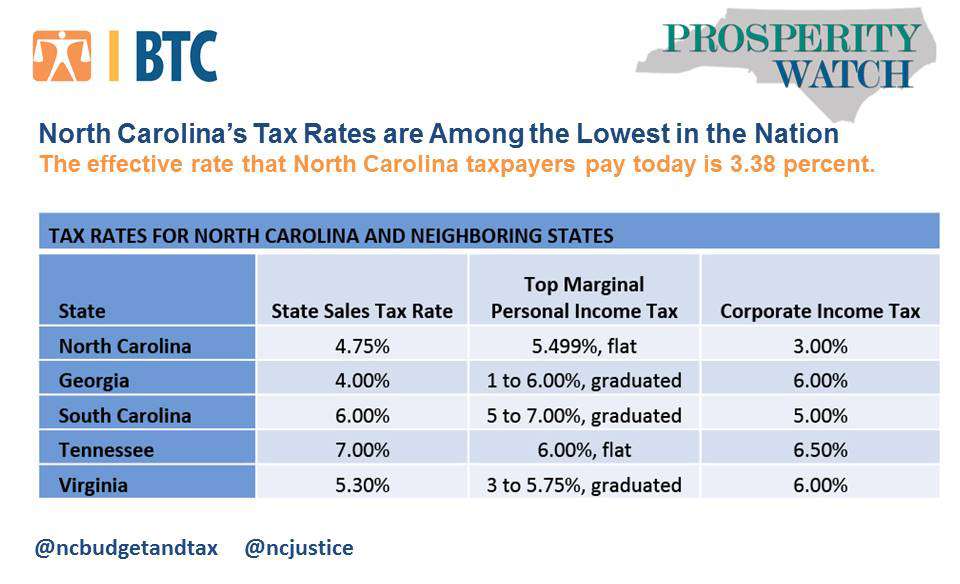

The base North Carolina state sales tax rate is 4.75%. However, every county in the state adds its own local tax on top of the state rate. In most North Carolina counties, the total combined sales tax rate is either 6.75% or 7%. Some counties, particularly those with higher infrastructure needs or transit projects (like Wake, Durham, and Orange), may reach 7.25% or 7.5%.

For businesses, the “Use Tax” is an often-overlooked counterpart to the sales tax. If a business purchases equipment or supplies from an out-of-state vendor that does not collect NC sales tax, the business is legally obligated to report and pay the “use tax” directly to the NCDOR. Failure to do so is a frequent trigger for tax audits.

Exemptions and Tax-Free Scenarios

North Carolina provides exemptions for certain categories of goods. For instance, most grocery items (unprepared food) are exempt from the state sales tax, though they may still be subject to a 2% local tax. Prescription drugs and certain medical devices are also generally exempt.

Unlike some neighboring states, North Carolina has largely moved away from the “Sales Tax Holiday” or “Tax-Free Weekend” for back-to-school shopping. While these were popular in previous decades, the state legislature repealed them in 2014, citing the need for a broader, lower tax rate for everyone throughout the year rather than targeted breaks for specific items.

Property Taxes and Other Local Levies

In North Carolina, the state government does not levy a tax on real property. Property taxes are strictly the domain of local governments—counties and municipalities. However, because these taxes constitute a large portion of an individual’s or business’s total tax burden, they are an essential part of the “NC state tax” conversation.

Real Estate vs. Personal Property Tax

Property tax in North Carolina is divided into two main categories: real property (land and buildings) and personal property (vehicles, boats, and business equipment).

The “Tag & Tax Together” program is a unique feature of North Carolina’s personal property tax system. When residents renew their vehicle registration (the “tag”), they pay the local property tax on that vehicle at the same time. This streamlined approach ensures high collection rates and prevents residents from being surprised by a separate property tax bill for their cars later in the year.

How Property Assessments Work

Property taxes are “ad valorem,” meaning they are based on the assessed value of the property. North Carolina law requires counties to revalue real property at least once every eight years, though many counties choose to do so every four years to keep pace with market fluctuations.

For real estate investors, understanding the “millage rate” (the amount of tax per $1,000 of property value) in specific counties like Mecklenburg or Guilford is crucial for calculating the potential Return on Investment (ROI). Because rates vary significantly by county and city, location is a primary factor in tax-efficient real estate planning.

Strategies for Tax Planning and Optimization in NC

Effective wealth management requires more than just knowing the rates; it requires a proactive strategy to minimize liability and maximize after-tax income.

Leveraging State-Specific Credits and Deductions

While North Carolina has simplified its tax code, a few key credits remain. The most notable is the Credit for Children, which provides a sliding-scale credit for each qualifying child for whom the taxpayer is allowed a federal child tax credit. The amount of the credit depends on the taxpayer’s Adjusted Gross Income (AGI).

For those focused on education savings, North Carolina offers a unique advantage for 529 plans. While there is no longer a state tax deduction for contributions into the NC 529 plan, the earnings grow tax-free, and withdrawals for qualified education expenses are not subject to state income tax. This remains a powerful tool for long-term financial planning.

Retirement Planning and Tax Treatment

North Carolina is often ranked as a tax-friendly state for retirees. The state does not tax Social Security benefits. For other types of retirement income—such as private pensions, 401(k) distributions, and IRA withdrawals—the standard 4.5% flat rate applies.

However, “Bailey Settlement” retirees (certain federal, state, and local government employees who were vested in their retirement systems as of August 12, 1989) may be eligible to receive their retirement benefits completely free of North Carolina state income tax. This is a critical distinction for former government employees planning their retirement in the state.

Conclusion

The North Carolina state tax system reflects a broader trend toward fiscal conservatism and simplicity. By moving to a flat tax for individuals and phasing out the corporate income tax, the state has positioned itself as a destination for both business investment and personal wealth accumulation.

Whether you are a resident calculating your annual take-home pay or a business owner projecting five-year growth, the stability of a flat-tax environment provides a level of predictability that is invaluable in financial planning. As the state continues to lower rates in the coming years, staying informed on legislative changes will be the key to maintaining a competitive financial edge in the Tar Heel State.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.