The allure of the Powerball jackpot is a central fixture in the American financial imagination. For many, the dream of transitioning from a standard salary to generational wealth rests on the selection of five white balls and one red Powerball. While the lottery is fundamentally a game of chance, the quest to identify the “most winning numbers” is more than just a pursuit of luck—it is an exercise in data analysis, probability, and financial behavior.

When we discuss the most frequent numbers in Powerball, we are looking at historical frequency. However, from a professional financial perspective, it is equally important to understand how these numbers interact with the laws of probability and how the “lottery mindset” fits into a broader personal finance strategy. In this article, we will break down the statistical leaders in the Powerball history books and examine the economic realities of chasing the jackpot.

The Statistical Leaders: Decoding the Most Frequent Draws

To identify the most winning numbers, one must look at the data provided by the Multi-State Lottery Association (MUSL). It is important to note that Powerball underwent a significant rule change in October 2015, which altered the number pool (moving to 69 white balls and 26 red Powerballs). For the most accurate and relevant financial data, analysts typically focus on draws from this modern era.

The Most Frequent White Balls

Statistically, certain numbers have appeared with a higher frequency than others due to the natural variance of random selection. In recent years, numbers such as 61, 32, 63, 21, and 36 have surfaced as some of the most frequently drawn white balls. While every number technically has the same mathematical probability of being drawn in any single event, these “hot numbers” often become the focus of players looking for a perceived edge.

The Most Frequent Powerballs

The red Powerball is the ultimate multiplier of wealth. Historically, the number 18 has appeared more frequently than others, followed closely by numbers like 24, 6, and 20. Because the Powerball pool is smaller (1 to 26) than the white ball pool (1 to 69), the frequency of these numbers is more concentrated, making the statistical outliers appear more significant to the casual observer.

The Law of Large Numbers and “Cold” Numbers

In financial modeling, we often refer to the “Law of Large Numbers,” which suggests that as a sample size grows, the actual results will converge on the expected probability. In the context of the lottery, this means that over thousands of years of draws, every number would eventually be drawn roughly the same number of times. Players who avoid “hot” numbers often pivot to “cold” numbers—those that haven’t appeared in a long time—betting on the idea that they are “due” for a win. From a strict financial and mathematical standpoint, however, each draw is an independent event with no memory of past results.

Probability vs. Strategy: Why Numbers Alone Don’t Guarantee Wealth

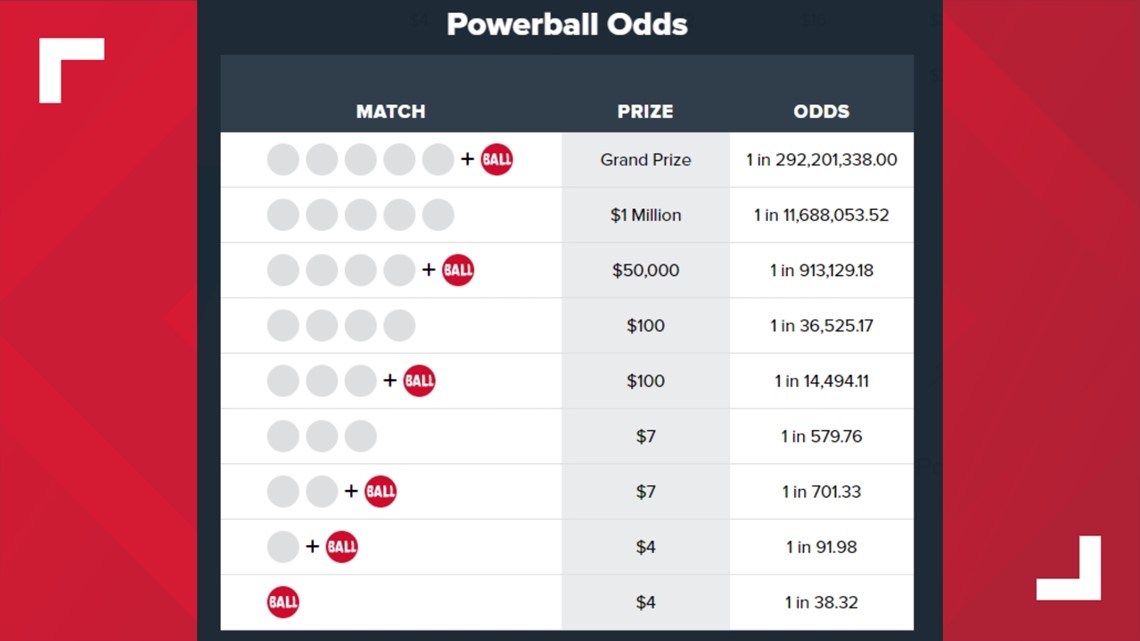

While tracking winning numbers is an interesting statistical exercise, a sophisticated approach to personal finance requires an understanding of the odds. The probability of winning the Powerball jackpot is approximately 1 in 292.2 million. To put this into a financial perspective, you are significantly more likely to become a billionaire through traditional entrepreneurship or to be hit by a meteorite than you are to hold the winning ticket.

The Concept of Independent Events

One of the most common pitfalls in financial decision-making is the “gambler’s fallacy.” This is the belief that if something happens more frequently than normal during a given period, it will happen less frequently in the future (or vice versa). In Powerball, the balls do not know they were drawn last week. Whether you pick the “most winning” numbers or a set of random digits, your mathematical chance of success remains identical.

The Danger of Shared Numbers

From a wealth-maximization standpoint, the biggest risk isn’t just losing; it’s winning and having to share the prize. Many people choose numbers based on birthdays or anniversaries, which limits their selection to 1 through 31. If you play the “most frequent” numbers that are publicly listed on various websites, you are likely playing the same numbers as thousands of other people. If those numbers hit, the jackpot is split, significantly reducing your individual net worth gain. Financial strategists often suggest that if one must play, using “Quick Pick” or choosing numbers above 31 may reduce the likelihood of a shared jackpot.

Expected Value in Lottery Participation

In finance, “Expected Value” (EV) is a calculation of the average outcome of a random variable. Most of the time, the EV of a Powerball ticket is negative—meaning for every $2 spent, you expect to lose money. However, when the jackpot exceeds approximately $800 million, the EV can technically turn positive. But even then, the “tax” of probability and the risk of multiple winners usually keep the lottery from being a viable “investment” in any professional portfolio.

The Financial Economics of the Lottery

The lottery is often described by economists as a “regressive tax” or a “tax on math.” Understanding where the lottery fits into the national and individual economy is crucial for maintaining a healthy relationship with money.

Opportunity Cost: Tickets vs. Index Funds

The most significant financial concept related to the lottery is opportunity cost—the benefit you give up by choosing one alternative over another. If an individual spends $10 a week on Powerball tickets, that equates to roughly $520 a year. If that same $520 were invested in a low-cost S&P 500 index fund with an average annual return of 8%, over 30 years, that “lottery fund” would grow to over $60,000. For a consistent player, the “most winning” strategy isn’t picking the right numbers; it’s picking the right asset class.

The “Hidden Tax” and State Revenue

From a corporate and government finance perspective, Powerball is a massive revenue generator. A significant portion of every ticket sale goes back to the state to fund education, infrastructure, and senior services. While this provides a public good, the financial burden falls disproportionately on lower-income individuals who may view the lottery as their only path to financial mobility.

The Psychology of “Hope Capital”

Despite the dismal odds, people continue to play. In behavioral finance, this is sometimes called “Hope Capital.” The $2 spent on a ticket buys a period of time where the purchaser can psychologically experience the possibility of wealth. While this has an emotional utility, it must be balanced against the reality of one’s long-term financial goals, such as retirement savings or debt reduction.

Wealth Management: What Happens After the Winning Numbers Hit?

If the statistical anomaly occurs and your numbers are drawn, the transition from a “player” to a “high-net-worth individual” requires immediate and rigorous financial planning. Most lottery winners lose their fortune within a few years because they lack a structural framework for managing sudden wealth.

The Lump Sum vs. Annuity Dilemma

The first major financial decision a winner faces is how to receive the money. The “Cash Option” provides a one-time lump sum, while the “Annuity Option” pays out over 30 years.

- The Lump Sum: This is often the choice for those with access to sophisticated financial advisors. It allows for immediate investment and the potential to outpace the annuity’s growth through market returns. However, it also carries the highest risk of “lifestyle creep” and rapid depletion.

- The Annuity: This is essentially a forced budget. It provides a guaranteed income stream, protecting the winner from their own potential mismanagement and ensuring that even if they blow the first few millions, they have a fresh start the following year.

Building a Professional Financial Fortress

Upon winning, the very first step—before claiming the prize—is to assemble a team of professionals. This typically includes:

- A Tax Attorney: To navigate the massive federal and state tax liabilities (which can exceed 40% of the total win).

- A Certified Financial Planner (CFP): To create a diversified portfolio that generates sustainable income.

- An Estate Planner: To protect the wealth for future generations and manage the inevitable influx of requests for money from “friends” and relatives.

The Reality of “Sudden Wealth Syndrome”

In the world of business finance, we see a similar phenomenon with athletes and lottery winners known as Sudden Wealth Syndrome. The psychological pressure of managing a nine-figure sum can lead to poor decision-making and isolation. A professional financial plan doesn’t just manage the numbers; it manages the expectations and the boundaries of the individual.

Conclusion: The Final Tally on Winning Numbers

So, what is the “most winning” number in Powerball? Statistically, it might be 61 or 18. But financially, the most winning “number” is your net savings rate and your investment return over time.

While tracking the frequency of lottery draws is a fascinating hobby and a masterclass in probability theory, it should never be confused with a sound financial strategy. The path to wealth is rarely found in a plastic sphere filled with numbered balls; it is found in the disciplined application of financial principles, the understanding of compound interest, and the avoidance of high-risk, low-reward gambles.

If you choose to play, do so with “fun money” that has already been accounted for in your budget after your 401(k) and emergency funds are topped off. In the grand scheme of personal finance, the only way to “guarantee” a win is to invest in yourself and your portfolio with the same consistency that some reserve for the Saturday night draw.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.