Navigating the complexities of the United States Social Security system can often feel like solving a high-stakes puzzle. For millions of American workers, the milestone of “40 credits” is frequently cited as the magic number that unlocks the door to retirement security. However, while 40 credits represent the threshold for eligibility, they do not dictate a specific, uniform dollar amount for every recipient. Understanding what the minimum benefit looks like—and how it is calculated—is essential for any robust personal finance strategy.

In the realm of money management and retirement planning, clarity is power. This guide explores the mechanics of Social Security credits, the reality of the “Special Minimum Benefit,” and how a short work history can impact your financial health in your golden years.

The Fundamentals of Social Security Credits and Eligibility

Before addressing the dollar amounts, it is vital to understand the currency of the Social Security Administration (SSA): the work credit. Unlike a traditional pension that might be based solely on years of service, Social Security relies on a system of earned credits based on your annual taxable income.

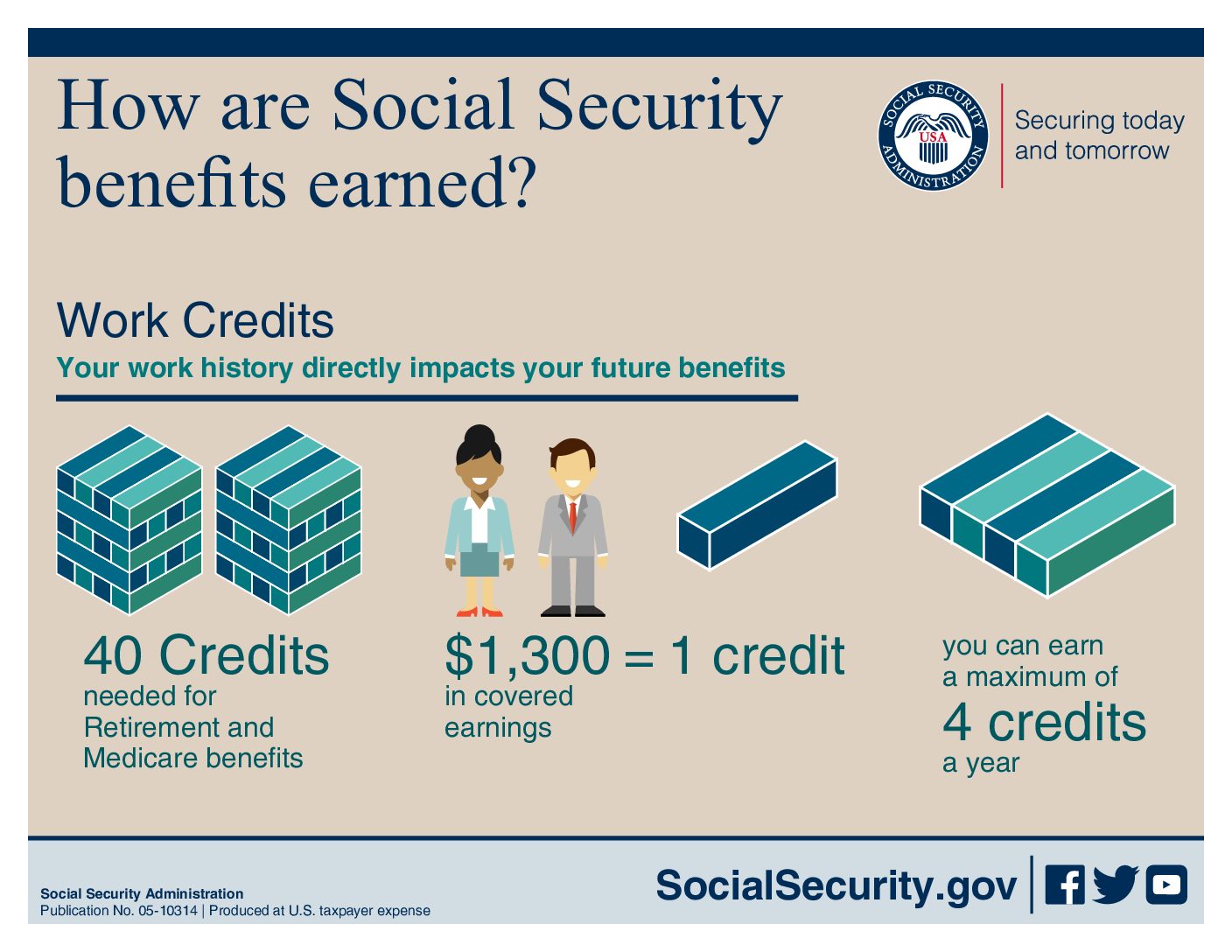

How You Earn Social Security Credits

You earn credits by working and paying Social Security taxes. The amount of earnings required for a credit changes annually to keep pace with inflation. For instance, in 2024, you earn one credit for every $1,730 of earnings. You can earn a maximum of four credits per year. Therefore, once you have earned $6,920 in a calendar year, you have “maxed out” your credits for that period.

It is important to note that you do not earn more “points” for earning $100,000 versus $10,000 in terms of the credit count; both earners receive the same four credits for the year, though their eventual benefit amounts will differ significantly based on the total sum of their contributions.

Why 40 Credits is the Golden Number for Eligibility

For most workers born after 1929, the SSA requires 40 credits to be “fully insured” for retirement benefits. Since you can only earn four credits per year, this effectively means you must work for at least ten years in a job where you pay into the Social Security system.

Reaching 40 credits is a binary switch: once you hit this number, you are eligible to receive a monthly check starting as early as age 62. If you have 39 credits, you generally receive nothing. However, being eligible for a benefit does not mean the benefit will be substantial. The 40-credit mark is merely the entry fee to the system; the actual payout is determined by a much more rigorous mathematical formula.

Calculating Your Benefit: Why 40 Credits Doesn’t Guarantee a High Payout

A common misconception in personal finance is that reaching the 40-credit milestone guarantees a specific “minimum” floor of income. In reality, Social Security benefits are progressive, meaning they are designed to replace a larger percentage of income for low earners than for high earners, but they are still tied directly to your lifetime earnings average.

The 35-Year Average Formula

To determine your monthly benefit, the SSA looks at your “Average Indexed Monthly Earnings” (AIME). They take your top 35 years of earnings, adjust them for inflation (indexing), and then divide the total by 420 (the number of months in 35 years).

This is where the “40 credits” minimum can become a financial pitfall. If you have exactly 40 credits—meaning you worked for only 10 years—the SSA still uses a 35-year divisor. In this scenario, the formula would include 10 years of earnings and 25 years of zeros.

The Impact of “Zero” Years on Your Monthly Check

When 25 years of zero income are averaged into your calculation, your AIME drops precipitously. This results in a very low Primary Insurance Amount (PIA). For someone who worked the bare minimum of 10 years at a modest wage, the resulting monthly benefit might be only a few hundred dollars—far below what is required to cover basic living expenses.

From a money management perspective, this highlights the importance of working beyond the 10-year mark. Every year you work past 40 credits replaces a “zero” year in the 35-year calculation, which can significantly boost your monthly check.

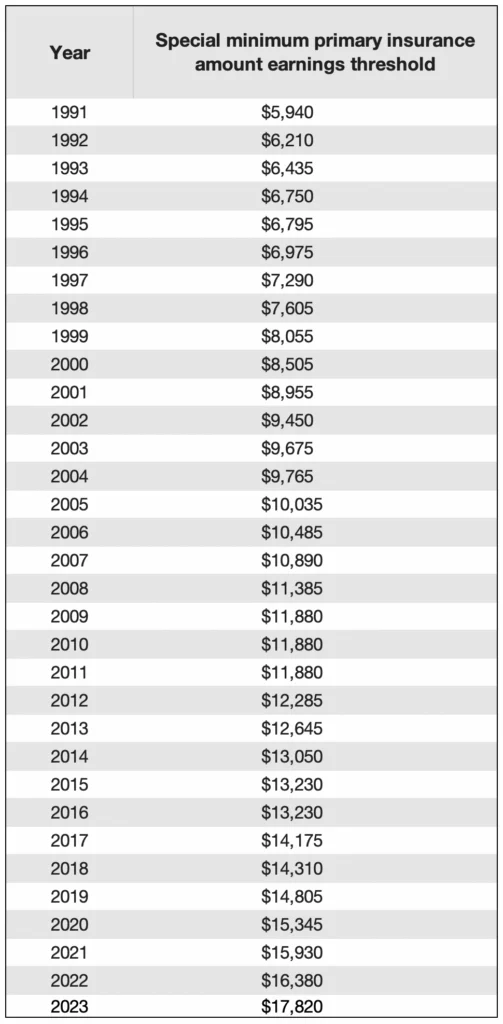

The Special Minimum Benefit vs. Standard Retirement Insurance

There is often confusion between the “regular” benefit and something called the “Special Minimum Benefit.” While the standard formula can result in a benefit that is technically very low (even under $100 for some), the Special Minimum Benefit was designed to provide a floor for long-term, low-wage earners.

Who Qualifies for the Special Minimum Benefit?

The Special Minimum Benefit is not based on the 40-credit rule alone. Instead, it is based on “Years of Coverage” (YOC). To qualify for even the lowest tier of the Special Minimum Benefit, a worker must have more than 10 years of coverage.

As of 2024, the Special Minimum Benefit has become largely obsolete for new retirees. This is because the standard benefit (calculated via the AIME/PIA formula) has grown faster due to wage indexing than the Special Minimum Benefit, which is indexed to price inflation. Consequently, most people find that their “regular” benefit is already higher than the Special Minimum floor.

The Difference Between “Years of Coverage” and “Credits”

It is a crucial distinction: a “credit” is earned with relatively low earnings ($1,730 in 2024), but a “Year of Coverage” for the Special Minimum Benefit requires a much higher threshold of earnings. Because of this, it is possible to have 40 credits but zero “years of coverage” for the purpose of the Special Minimum Benefit. For those relying on this as a safety net, it is often a shock to realize that the “minimum” benefit is not a guaranteed living wage.

Strategies to Increase Your Social Security Benefit Beyond the Minimum

If you find yourself approaching retirement with only the minimum 40 credits, or if your earnings history is spotty, there are tactical financial moves you can make to improve your outcome.

The Power of Delaying Benefits Until Age 70

The age at which you claim Social Security is the single biggest factor you can control. While you can claim at 62, your benefit will be reduced by up to 30% compared to your Full Retirement Age (FRA). Conversely, if you delay claiming past your FRA, your benefit increases by approximately 8% for every year you wait, up to age 70.

For a low-earner with 40 credits, delaying from age 62 to 70 can nearly double the monthly check. In the context of personal finance, this is a “guaranteed” return that is virtually impossible to find in the private market.

Maximizing Earnings During Your Peak Working Years

Because Social Security is based on your 35 highest-earning years, your current income matters. If you have already reached your 40 credits but have many “zero” or low-earning years on your record, staying in the workforce for even three to five additional years can have a disproportionate impact. By replacing years where you earned nothing with years of even moderate income, you raise the floor of your AIME and, by extension, your monthly PIA.

Navigating the Future of Your Retirement Income

Relying solely on the minimum Social Security benefit is a precarious financial position. As costs for healthcare and housing continue to rise, those with a limited work history must look toward supplemental strategies to ensure a dignified retirement.

Supplemental Income Sources

For those who qualify for only a minimal Social Security benefit due to low lifetime earnings or disability, the Social Security Administration also manages Supplemental Security Income (SSI). Unlike Social Security retirement benefits, SSI is a needs-based program funded by general tax revenues, not Social Security taxes. It is designed for aged, blind, or disabled individuals with limited income and resources. In many cases, if your Social Security retirement benefit is exceptionally low, SSI may “top off” your income to a baseline level set by the federal government.

Financial Planning for Low-Benefit Recipients

The reality of the 40-credit rule is that it represents a beginning, not an end. True financial security requires a multi-pillared approach:

- Personal Savings: Even small contributions to a Roth IRA can provide tax-free growth that supplements a small Social Security check.

- Debt Management: Entering retirement with a low Social Security benefit is significantly easier if high-interest debt and housing costs are minimized.

- Part-Time Work: Many retirees with 40 credits choose to work part-time. If you are over your Full Retirement Age, you can earn an unlimited amount of money without your Social Security benefits being reduced.

In conclusion, the “minimum Social Security benefit” for someone with 40 credits is not a fixed number, but a variable result of a complex 35-year calculation. While 40 credits makes you eligible, the quality of your retirement depends on the consistency and level of your earnings over your entire career. By understanding these mechanics, you can better position yourself to maximize your benefits and build a more stable financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.