In the modern landscape of digital banking, where peer-to-peer transfers and mobile wallets dominate daily transactions, the humble paper check might seem like a relic of a bygone era. Yet, millions of these documents are processed daily by financial institutions worldwide. At the heart of this enduring system lies a string of numbers printed along the bottom edge of every check: the MICR line. Understanding this specialized technology is essential for anyone managing business finance or personal accounts, as it remains the primary mechanism for automated check clearing.

Decoding the Anatomy of the MICR Line

The term MICR stands for Magnetic Ink Character Recognition. It is a proprietary technology used primarily by the banking industry to streamline the processing and clearance of checks. Unlike standard ink, MICR characters are printed using an iron-oxide ink or toner that can be easily magnetized and read by high-speed processing equipment.

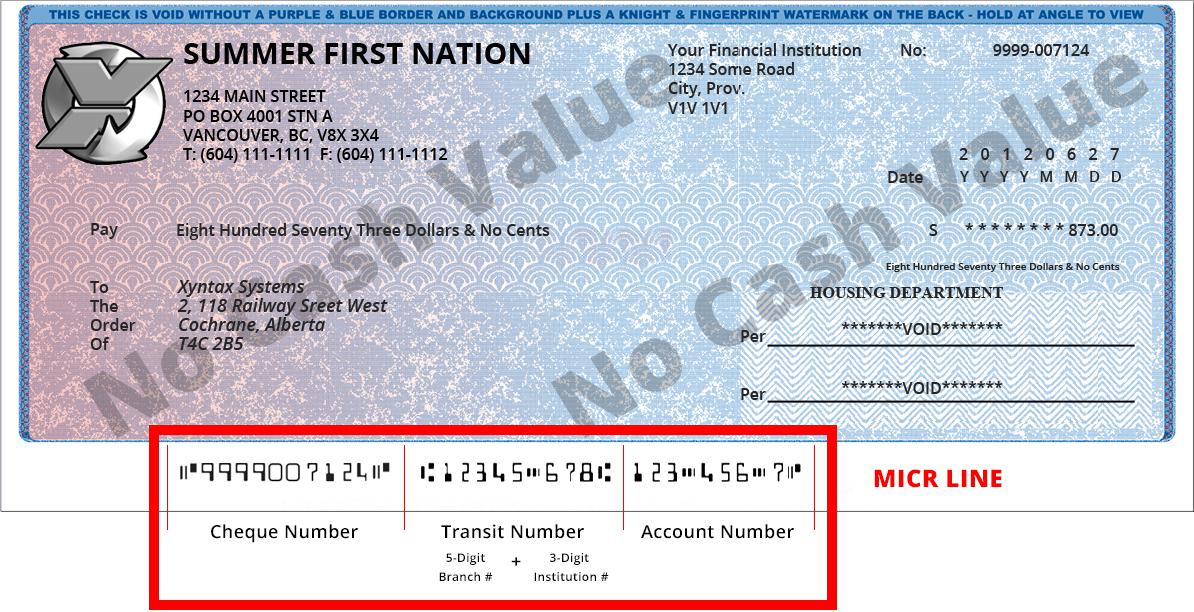

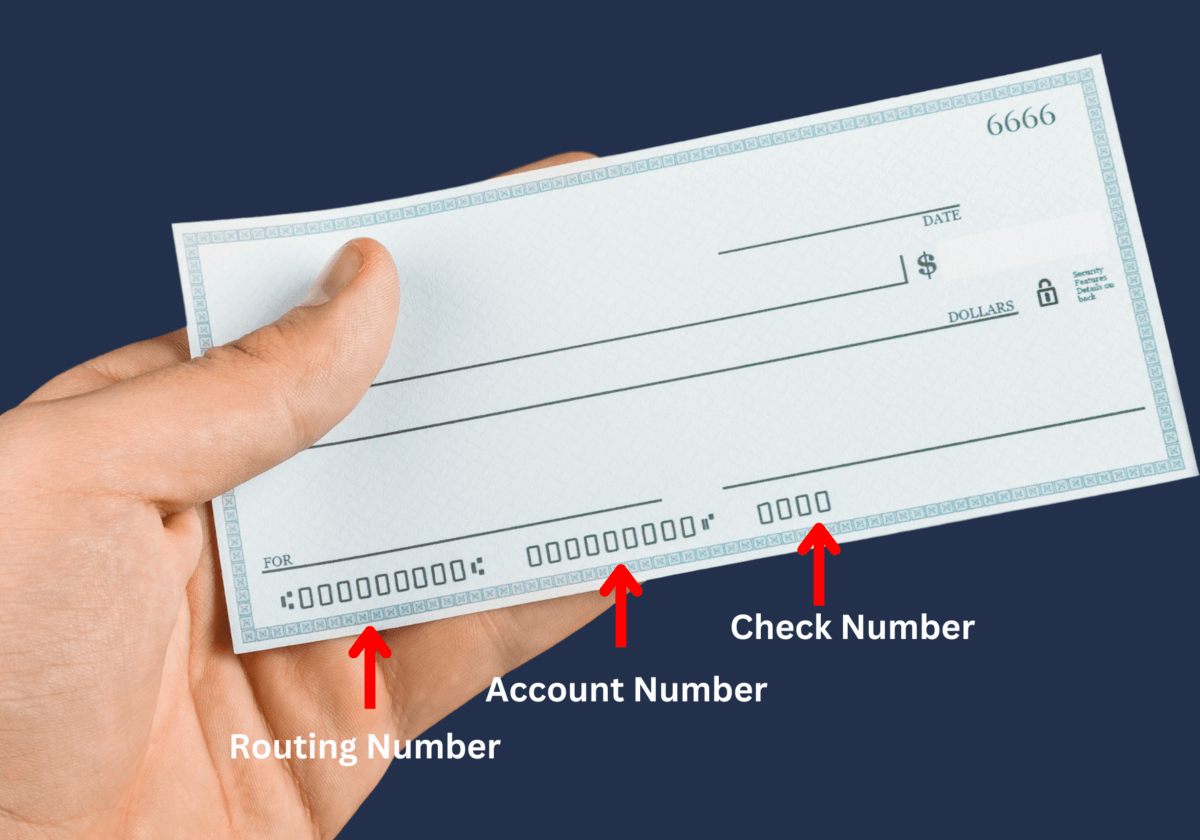

The MICR line is located at the bottom of a check and is composed of three distinct segments separated by specific symbols. These symbols—often looking like brackets, dashes, or unique geometric shapes—act as delimiters for the bank’s sorting machines.

The Routing Transit Number

The first set of numbers, typically found on the far left, is the nine-digit Routing Transit Number (RTN). This code serves as the geographic and institutional address for the bank where the account is held. The first two digits signify the Federal Reserve District where the bank is located, while the remaining digits provide the specific routing information for the financial institution. Without this number, the banking system would have no roadmap to determine where the funds should be withdrawn from.

The Account Number

Following the routing number is the customer’s specific Account Number. This set of digits identifies the individual or business entity associated with the funds. The length of this number can vary depending on the bank’s internal systems, and it is crucial for ensuring that the debit is applied to the correct ledger.

The Check Number

The final segment of the MICR line, usually located on the far right, is the Check Number. This number corresponds to the number printed in the top right corner of the check. It serves as a record-keeping tool for the account holder and a security verification tool for the bank. When banks process large volumes of checks, this number helps in identifying duplicate submissions or gaps in a check register.

How Magnetic Ink Character Recognition Works

The brilliance of the MICR system lies in its tolerance for physical wear and tear. Paper checks pass through high-speed sorting machines that move at incredible velocities. During this process, the checks often become wrinkled, stained, or smudged with other inks. Standard optical character recognition (OCR) might fail if a smudge obscures a letter or number. MICR, however, is impervious to these issues.

The Role of Magnetism

When a check enters a reader-sorter machine, it passes through a magnetic head. The iron oxide within the MICR ink becomes magnetized, creating a unique signal wave for each character. Because the ink is magnetic, the machine can “read” the numbers even if they are covered by stamps, dirt, or other non-magnetic marks. This ensures that the bank can reconcile the transaction accurately without human intervention.

Standardized Typography

To facilitate this reading process, all MICR characters are printed using specific, standardized fonts known as E-13B or CMC-7. These fonts were designed with precise geometric proportions, allowing the magnetic readers to distinguish between a “3” and an “8,” or a “0” and an “O,” with near-perfect accuracy. Any deviation from these font standards can cause a check to be rejected by the automated clearinghouse, resulting in manual processing fees or delays.

The Financial Significance of MICR in Business

For businesses, the MICR line is more than just a sequence of digits; it is a critical component of accounts payable and receivable operations. The automation made possible by MICR allows for the high-volume processing of payroll checks, vendor payments, and dividend distributions.

Streamlining Accounts Payable

Large corporations process thousands of checks weekly. By utilizing MICR-compliant check stock and specialized printers, businesses can print their own checks in-house. This capability reduces the overhead costs associated with ordering pre-printed check stock from traditional vendors and allows for the immediate generation of payments. However, this requires businesses to maintain high standards for their printers, as the magnetic toner must be applied at a specific thickness and density to remain readable by the banking system.

Security and Fraud Prevention

While the MICR line facilitates efficiency, it is also a point of focus for financial security. Because the MICR line contains the routing and account information, it is a primary target for check fraud. Sophisticated criminals sometimes attempt to “wash” checks or create counterfeit checks using the stolen MICR data of legitimate businesses.

To combat this, many companies now employ “Positive Pay” systems. With Positive Pay, a business uploads a file of issued checks—including the check number, amount, and payee information—to their bank’s portal. When a check is presented for payment, the bank’s computer system compares the MICR line and the amount against the provided list. If the details do not match perfectly, the check is flagged for manual review, preventing fraudulent transactions from clearing.

The Future of MICR in a Digital Economy

The emergence of electronic check processing (e-check) and Remote Deposit Capture (RDC) has fundamentally altered how the MICR line is used. Today, when a customer uses a mobile banking app to deposit a check, they are taking a high-resolution photograph of the document.

Conversion to Digital Data

When a mobile deposit is made, the bank’s software uses advanced image analysis to “read” the MICR line from the photo. This data is then converted into an electronic payment file (an Image Replacement Document, or IRD). The paper check itself is no longer physically transported across the country; instead, the digital representation of the MICR line acts as the legal equivalent of the paper document.

The Decline of Paper and the Rise of ACH

Despite its ingenuity, the reliance on MICR-based paper checks is slowly declining. Automated Clearing House (ACH) transfers and real-time payment rails are providing faster, cheaper, and more secure alternatives for moving money. As businesses and consumers move toward digital invoicing and instant bank-to-bank transfers, the physical transit of paper checks becomes less frequent.

However, the MICR line continues to serve as the “legacy bridge.” It provides a standardized data format that connects the physical world of paper banking to the digital world of electronic clearing. As long as paper checks remain a recognized legal instrument for payment, the MICR line will persist as the essential language that banks use to communicate with one another. Whether you are a business owner printing payroll or an individual writing a one-off check, understanding the role of this magnetic line is a vital part of financial literacy in the modern banking age.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.