In the contemporary landscape of personal finance and business management, few terms carry as much weight—or cause as much debate—as the “living wage.” While often discussed in political spheres, the living wage is, at its core, a fundamental concept of personal finance. It represents the baseline income required for an individual or family to meet their basic needs without relying on external subsidies or falling into the cycle of predatory debt. Understanding what constitutes a living wage is essential for workers planning their careers, entrepreneurs building sustainable businesses, and investors evaluating the social impact of their portfolios.

Defining the Living Wage: More Than Just a Minimum

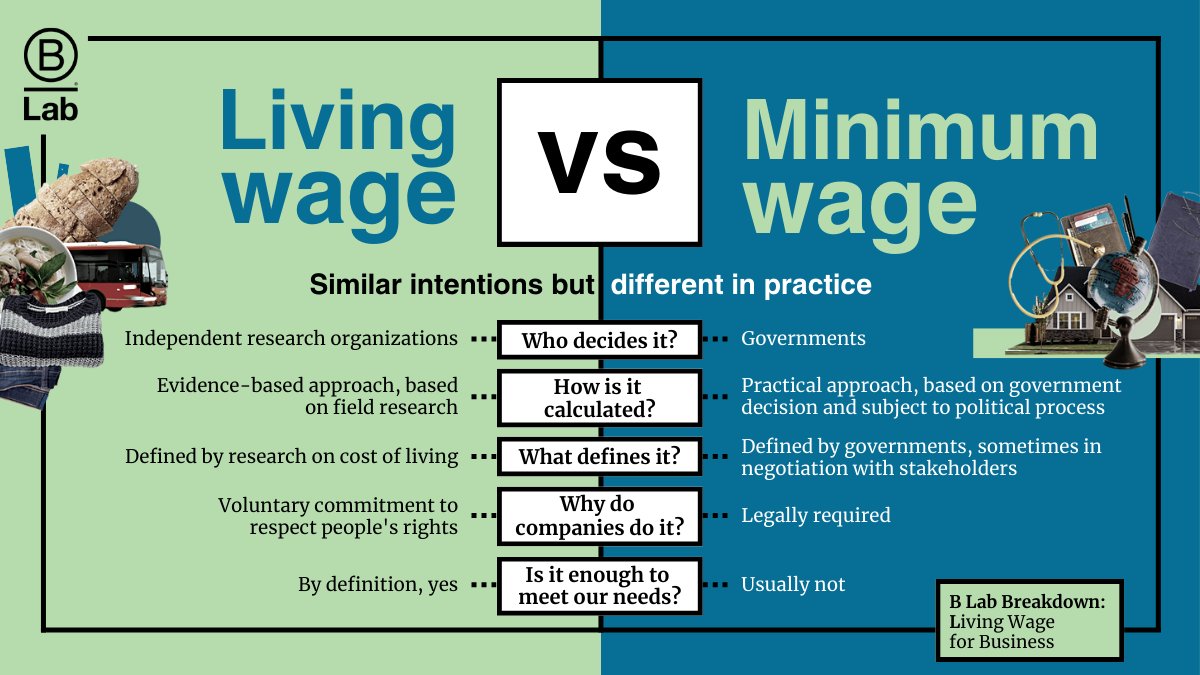

To understand the living wage, one must first distinguish it from other financial benchmarks. While the term is often used interchangeably with “minimum wage,” they represent two very different economic realities.

The Critical Difference Between Living Wage and Minimum Wage

The minimum wage is a legal mandate—a price floor set by government authorities that dictates the lowest amount an employer can legally pay a worker. Historically, minimum wages were designed to prevent the exploitation of workers, but in many jurisdictions, these rates have failed to keep pace with inflation and the rising costs of essential goods.

In contrast, a living wage is a market-based calculation. It is not defined by law but by the actual cost of living in a specific geographic area. A living wage ensures that a full-time worker can afford the basics: nutritious food, safe housing, healthcare, transportation, and perhaps a small margin for emergencies. While the minimum wage is a political compromise, the living wage is a financial necessity.

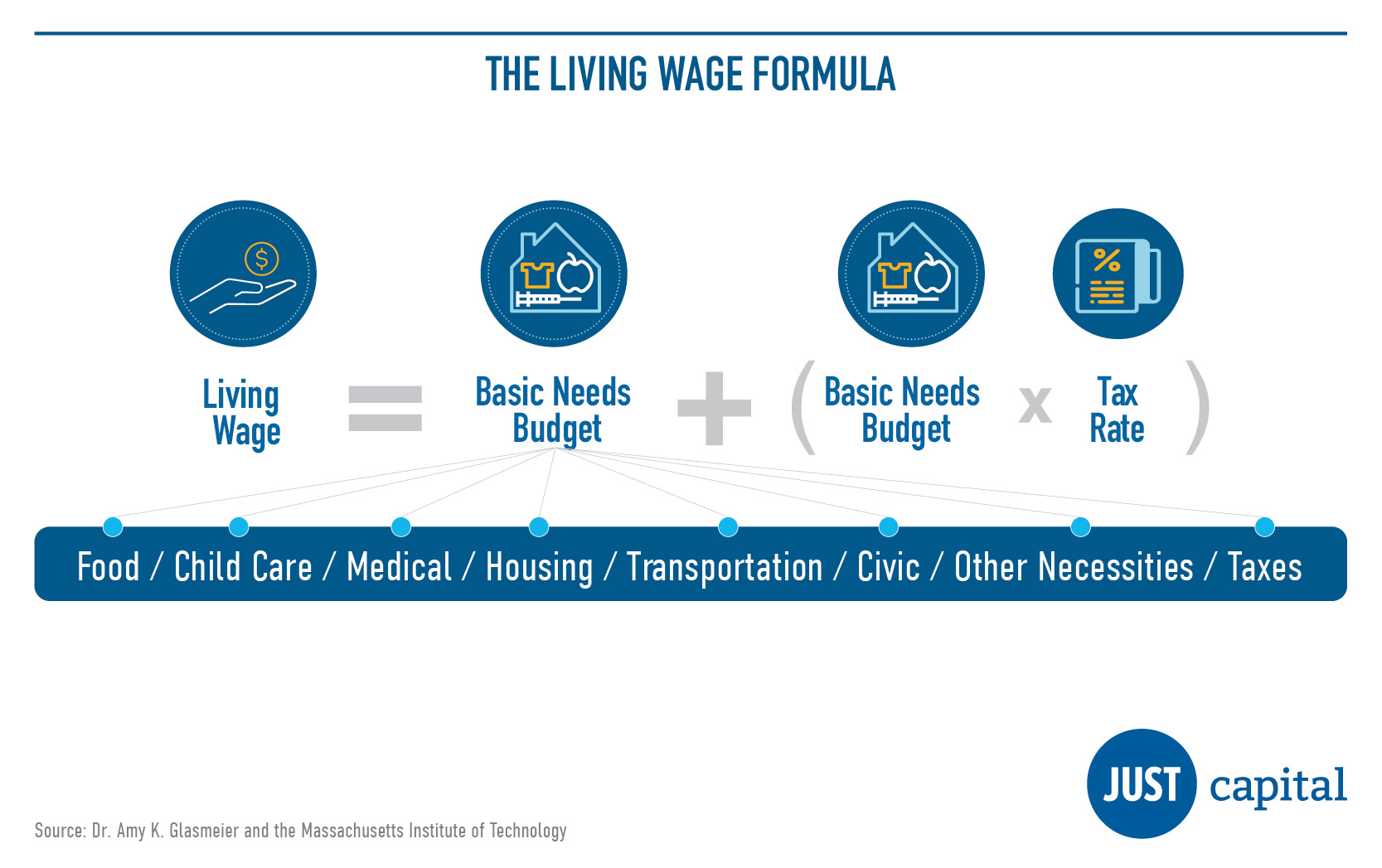

The Calculation Methodology: Basic Needs vs. Discretionary Income

How do economists and financial planners determine a living wage? Most models, such as the widely respected MIT Living Wage Calculator, use a “market basket” approach. This involves totaling the annual costs of essential expenses for different household compositions.

The primary components of a living wage budget typically include:

- Housing: Often the largest expense, usually capped at 30% of gross income for it to be considered “affordable.”

- Food: Based on low-cost food plans that meet nutritional requirements.

- Healthcare: Including insurance premiums and out-of-pocket costs.

- Transportation: The cost of maintaining a vehicle or utilizing public transit to commute to work.

- Taxes: Net income must be high enough that the “take-home” pay covers all the above after federal, state, and local taxes are deducted.

Crucially, a true living wage should also include a small buffer for “miscellaneous” expenses—clothing, basic personal care items, and minimal savings—to prevent a single unexpected expense from causing a total financial collapse.

Why the Living Wage Matters for Personal Finance and Business Growth

The gap between a worker’s actual earnings and a living wage has profound implications for both individual financial health and the broader economy. For those in the “Money” niche, understanding these implications is key to sound financial planning and responsible business ownership.

Economic Benefits for Households and Personal Resilience

From a personal finance perspective, earning a living wage is the prerequisite for moving from a state of “financial survival” to “financial stability.” When individuals earn a living wage, they are less likely to rely on high-interest credit cards or payday loans to cover monthly shortfalls.

This stability allows for the beginning of wealth accumulation. Once basic needs are met, individuals can start contributing to an emergency fund, participating in employer-sponsored retirement plans, or investing in the stock market. In short, the living wage is the foundation upon which all other personal finance goals—such as homeownership or debt-free living—are built.

The Business Case: Retention, Productivity, and Reputation

For business owners and managers, paying a living wage is often viewed as a cost burden, but data suggests it is a strategic investment. In the world of business finance, the “efficiency wage theory” argues that paying employees more than the market minimum yields significant returns.

- Reduced Turnover: Replacing an employee is expensive, often costing between 1.5 to 2 times the employee’s annual salary when accounting for recruiting, onboarding, and lost productivity. Paying a living wage increases loyalty and reduces these “hidden” costs.

- Higher Productivity: Workers who are not stressed about how they will pay for their next meal or rent payment are more focused, have higher morale, and perform better.

- Brand Value: In an era of conscious consumerism, companies that commit to being “Living Wage Employers” often see an increase in brand equity, attracting both customers and high-quality talent who value ethical business practices.

How Geographic Location and Household Composition Shape Financial Needs

One of the most complex aspects of the living wage is its variability. A “one size fits all” approach to income is impossible because the cost of capital and commodities varies wildly depending on where you live and who you support.

The Urban vs. Rural Divide

The financial requirements of a worker in New York City or San Francisco are vastly different from those in rural Mississippi or Nebraska. Housing is the primary driver of this disparity. In major metropolitan hubs, the living wage must account for skyrocketing rents and property taxes. Conversely, in rural areas, while housing might be cheaper, transportation costs are often higher due to the lack of public infrastructure and the need for longer commutes.

For someone pursuing “online income” or “side hustles,” this geographic variance creates an opportunity known as “geo-arbitrage.” By earning a salary calibrated for a high-cost area while living in a low-cost area, individuals can significantly increase their discretionary income and investment potential.

Impact of Family Structure on Financial Needs

A living wage is not a single number for everyone in a city; it scales with the size of the family. A single adult with no children has a much lower financial threshold than a single parent or a dual-income household with three children.

Childcare is often the “X-factor” in living wage calculations. In many parts of the United States, for example, the cost of childcare for two children can exceed the cost of housing. Therefore, when evaluating “business finance” or “personal income” targets, one must look at the specific household demographic to determine if the income is truly sustainable.

Strategies for Bridging the Gap: Moving Toward Financial Security

If your current income falls below the living wage for your area, or if you are a business owner looking to transition to a living wage model, several financial strategies can help bridge the gap.

Negotiating for Better Pay and Career Development

In the realm of personal finance, your “human capital”—your skills and experience—is your greatest asset. If your salary is not meeting the living wage threshold, the first step is often a strategic review of your market value.

- Upskilling: Using online tools and certifications to move into high-demand sectors like tech or finance.

- Negotiation: Armed with data from living wage calculators, individuals can approach employers for raises, highlighting their contributions and the economic reality of their location.

- Job Hopping: Statistically, individuals who change jobs every 2–3 years see higher wage growth than those who stay with a single employer, as new-hire budgets are often higher than retention budgets.

Leveraging Technology and Side Hustles for Income Diversification

For many, the path to a living wage is paved with multiple income streams. The “gig economy” and “online income” sectors have provided new ways to supplement a primary salary.

- Side Hustles: Whether it is freelance writing, digital marketing, or e-commerce, side hustles can provide the “buffer” that transforms a survival wage into a living wage.

- Financial Tools: Utilizing budgeting apps and automated savings tools can help individuals maximize the utility of every dollar earned. By optimizing expenses, one can effectively lower their personal “living wage” requirement without sacrificing quality of life.

The Future of the Living Wage in a Globalized Economy

As we look toward the future of money and work, the living wage will remain a central pillar of economic discussion. The rise of automation, the shift toward remote work, and fluctuating inflation rates all impact what it takes to live a dignified life.

Policy Trends and Corporate Social Responsibility

There is a growing movement toward “ESG” (Environmental, Social, and Governance) investing. Institutional investors are increasingly looking at whether companies pay a living wage as a metric for long-term sustainability. Businesses that ignore the living wage may find themselves at a disadvantage when seeking capital or trying to maintain a stable workforce in a competitive market.

Long-term Wealth Building Beyond Basic Subsistence

Ultimately, the goal of understanding the living wage is to move beyond it. A living wage is the floor, not the ceiling. The true objective of personal finance is to reach a point of “financial independence,” where passive income from investments, real estate, or business ventures covers your living expenses.

By first securing a living wage, individuals gain the breathing room necessary to educate themselves on investing and compound interest. Understanding the living wage is the first step in a lifelong journey of financial literacy, ensuring that money serves as a tool for freedom rather than a source of constant stress. In the end, a living wage is about more than just numbers on a paycheck—it is about the stability required to build a prosperous and secure future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.