When we discuss the “last stage of dementia,” the conversation is frequently confined to the clinical and emotional realms. However, for families, caregivers, and financial planners, the final phase of cognitive decline represents a significant financial milestone. From a wealth management perspective, the last stage of dementia is characterized by the total transition of fiscal responsibility and the peak of medical expenditure. It is the point where long-term care insurance triggers are fully met, estate plans are executed, and the “burn rate” of a portfolio often reaches its highest velocity.

Understanding the financial architecture of this stage is essential for preserving a legacy and ensuring the dignity of the individual. This guide explores the economic implications of late-stage dementia, focusing on personal finance, estate management, and strategic asset protection.

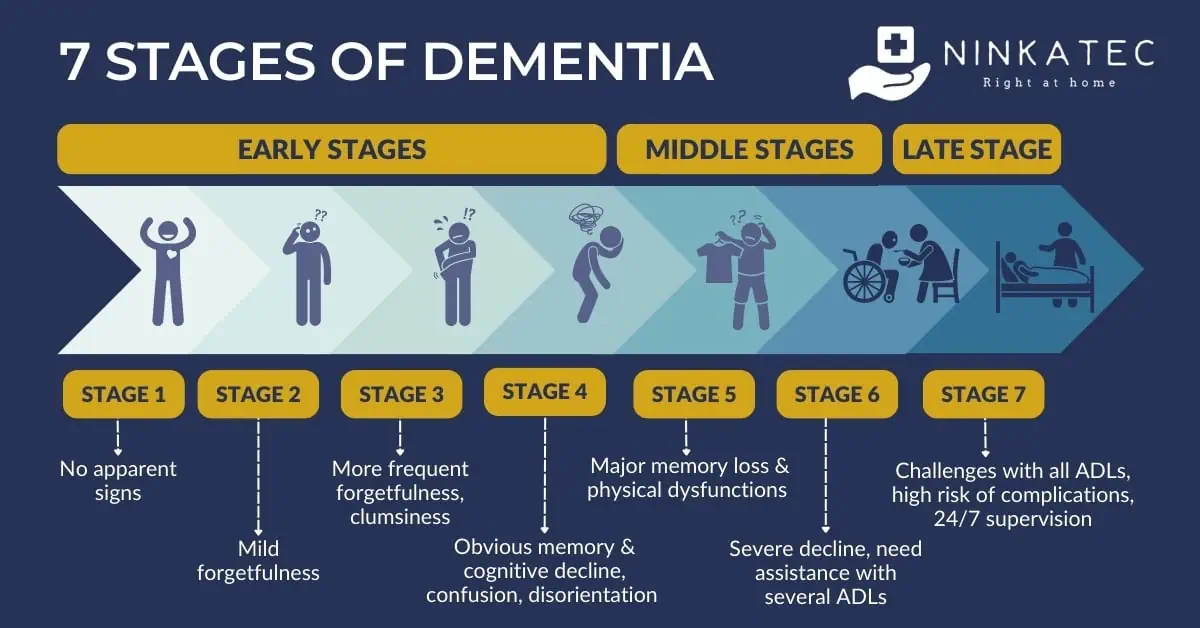

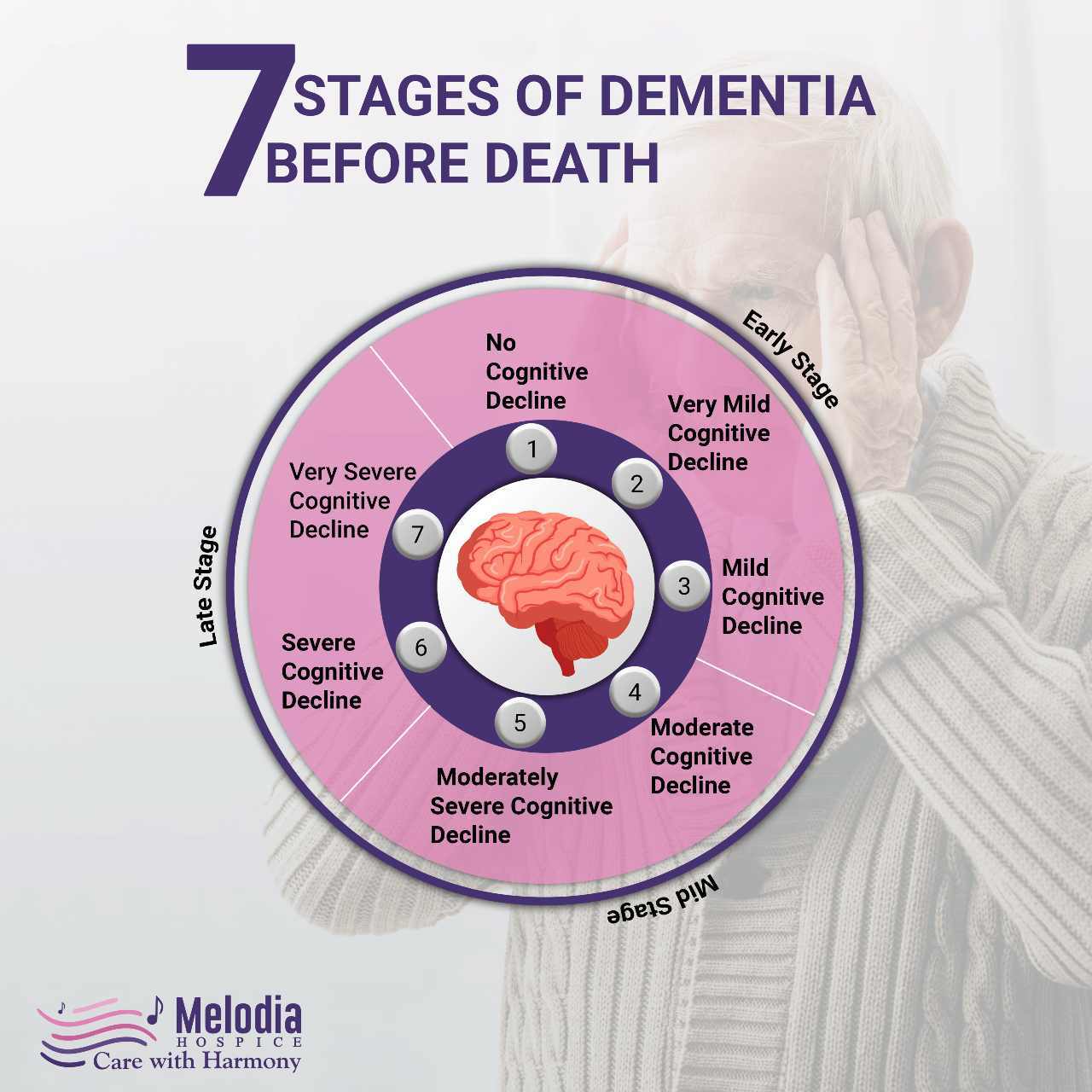

The Economic Definition of the Last Stage: Escalating Costs and Care Transitions

In financial terms, the last stage of dementia is defined by the necessity of 24-hour skilled nursing care. While earlier stages may involve part-time assistance or adult day programs, the final stage almost always requires a specialized memory care facility or round-the-clock in-home medical support.

The Peak of Medical Expenditure

The financial “last stage” is marked by a dramatic shift in the cost of care. According to recent industry benchmarks, the average cost of a private room in a nursing home can exceed $100,000 annually, while specialized memory care units often command a premium. This stage represents the most intensive drain on liquid assets. For many families, this is the period where “spend-down” strategies become the primary focus of their financial strategy.

Identifying the Transition from Home Care to Skilled Nursing

From a budgetary perspective, there is a clear demarcation when home-based care is no longer fiscally or practically viable. When an individual reaches the last stage of dementia, their medical needs often outpace the capabilities of family caregivers or non-medical home aides. Financially, this transition requires a re-evaluation of the monthly budget, shifting from hourly wage expenses to all-inclusive facility fees. Navigating this shift requires a deep understanding of the individual’s cash flow and the liquidity of their investment portfolio.

Essential Financial Tools for End-of-Life Management

Navigating the last stage of dementia requires more than just a savings account; it requires a sophisticated array of financial instruments designed to manage high-burn-rate scenarios.

Long-Term Care Insurance and Benefit Triggers

For those who had the foresight to invest in Long-Term Care (LTC) insurance, the last stage of dementia is when these policies become most critical. Most LTC policies are triggered when the insured cannot perform a specific number of “Activities of Daily Living” (ADLs), such as eating, bathing, or dressing. In the last stage, these triggers are almost universally met. However, managing the claim process requires meticulous record-keeping. Financial advisors must ensure that the “elimination period”—the out-of-pocket waiting period—is accounted for in the short-term liquidity plan.

The Role of Medicaid and Asset Protection

For many, the cost of the last stage of dementia will eventually exhaust personal savings. This is where Medicaid planning becomes a central pillar of the financial strategy. The “look-back period” (typically five years) is a crucial concept here. If assets were not moved into irrevocable trusts or gifted well in advance of the last stage, the family may face a “spend-down” phase where almost all assets must be exhausted before government assistance begins. Financial professionals focus on “exempt assets,” such as a primary residence or a single vehicle, to ensure that a surviving spouse is not left in a state of penury.

Estate Planning and the Fiduciary Transition

The last stage of dementia is the ultimate test of an estate plan’s durability. It is the period where the “intent” of the individual is replaced by the “action” of the fiduciary.

Power of Attorney and the Final Transition of Control

In the final stage, the individual with dementia no longer has the legal capacity to make financial decisions. This is when a Durable Power of Attorney (POA) for finances becomes the most active document in the portfolio. The fiduciary—whether a family member or a professional trustee—assumes total control over bank accounts, investment portfolios, and real estate. The financial challenge here is ensuring a seamless transition that avoids the “frozen account” syndrome, which can occur if the POA is not recognized by specific financial institutions or if it was not drafted with sufficient breadth.

Liquidity Planning and Final Expenses

As the individual approaches the very end of the last stage, the focus of the financial plan shifts toward liquidity for final expenses and estate taxes. It is often a mistake to have all wealth tied up in illiquid real estate or long-term CDs during this phase. A professional wealth manager will suggest maintaining a “liquidity bucket” to cover funeral costs, legal fees for probate, and any outstanding medical bills. This prevents the “fire sale” of assets at suboptimal prices during a time of familial grief.

Mitigation Strategies for the “Sandwich Generation”

The financial burden of the last stage of dementia often falls on the “Sandwich Generation”—adult children who are simultaneously funding their children’s education and their own retirement.

Balancing Elder Care Costs with Retirement Savings

One of the most significant risks during the last stage of dementia is the “wealth transfer in reverse,” where adult children use their own retirement contributions to fund a parent’s care. To mitigate this, families should explore “Life Insurance with Living Benefits” or “Asset-Based LTC” products. These hybrid tools allow for the death benefit to be accelerated to pay for care during the last stage of dementia, thereby protecting the adult children’s personal savings and ensuring the parent receives high-quality care without compromising the next generation’s financial security.

Tax Deductions and Credits for Medical Expenses

The silver lining of the high costs associated with the last stage of dementia lies in the tax code. Medical expenses that exceed a certain percentage of Adjusted Gross Income (AGI) are often deductible. This includes the cost of a nursing home if the primary reason for being there is medical care. For a family in a high tax bracket, these deductions can provide a significant “rebate” on the cost of care. Additionally, the “Dependent Care Credit” may apply if the individual with dementia lives with their children and meets certain IRS criteria. Utilizing these tax strategies is a proactive way to recoup some of the capital lost to care costs.

Wealth Preservation and Legacy Management

The final stage of dementia does not have to mean the total erosion of a family’s legacy. Through strategic planning, wealth can still be preserved for the next generation.

The Use of Irrevocable Trusts

To protect assets from being entirely consumed by the “last stage” costs, many families utilize Irrevocable Trusts. By placing assets into a trust years before the onset of the final stage, those assets are technically no longer owned by the individual and are therefore protected from Medicaid spend-down requirements and certain creditors. While this requires a loss of control, it is often the only way to ensure that a family business or a long-held family home survives the financial gauntlet of dementia care.

Charitable Giving and Tax-Efficient Transfers

For high-net-worth individuals, the last stage of dementia may trigger the activation of charitable remainder trusts or other philanthropic vehicles. These tools allow the individual to receive an income stream to pay for care while ensuring that the remaining principal goes to a chosen cause, often resulting in significant estate tax savings. In the niche of “Money,” the last stage is viewed as a complex puzzle of moving parts—balancing the immediate, heavy costs of healthcare with the long-term goal of generational wealth transfer.

Conclusion: The Financial Reality of the Final Stage

What is the last stage of dementia? In the world of finance, it is a period of peak expenditure, fiduciary responsibility, and complex tax maneuvering. It is the final chapter of a lifelong financial journey. While the medical reality is one of decline, the financial reality should be one of stability and prepared execution. By treating the last stage as a foreseeable financial event rather than an unpredictable crisis, families can protect their assets, honor their loved ones, and ensure that the legacy built over a lifetime is not erased in its final years. Professional financial planning is the bridge that carries a family through the last stage of dementia, providing the resources necessary for quality care while guarding the wealth meant for the future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.