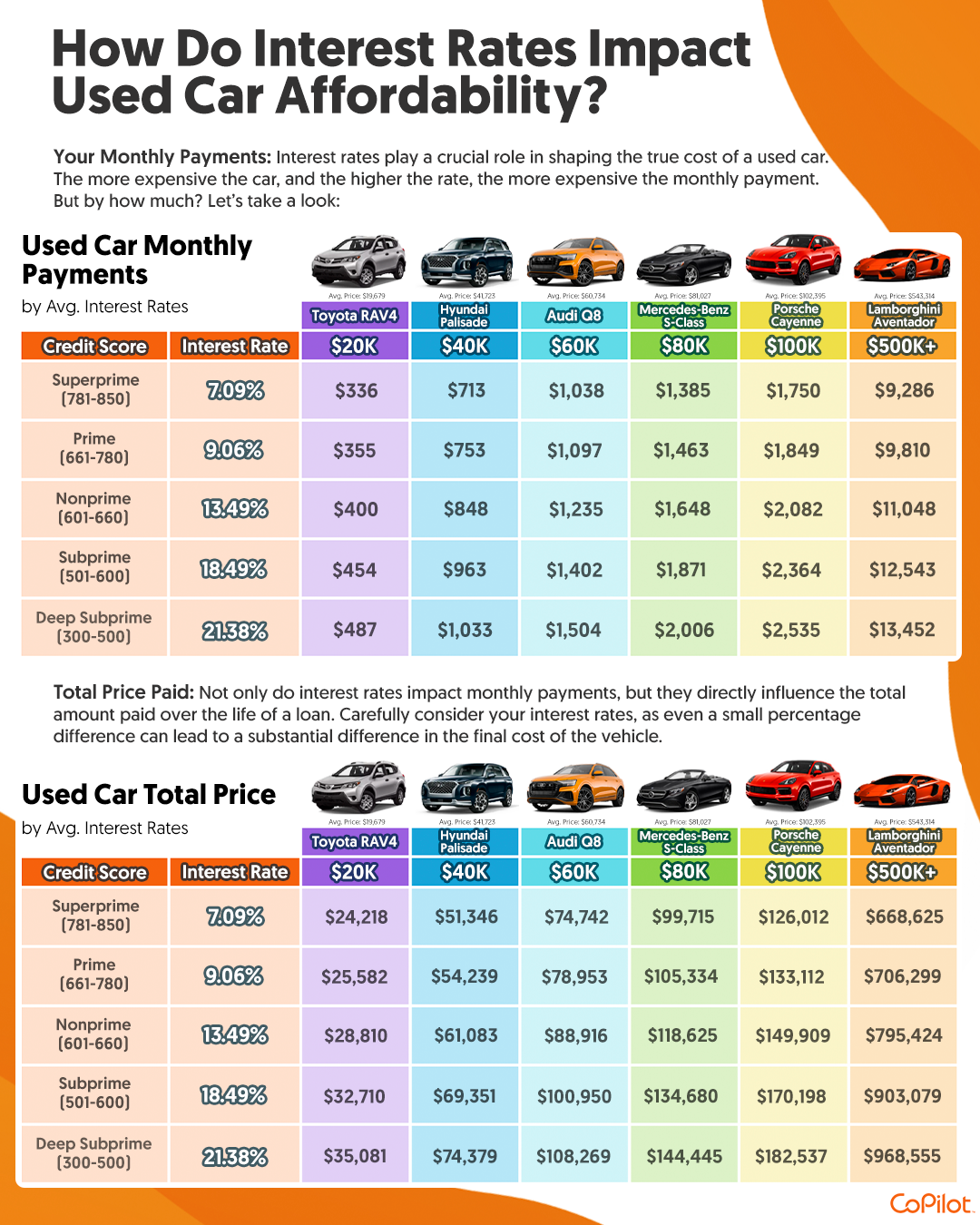

Understanding the interest rate for a car loan is a cornerstone of responsible personal finance, directly impacting the total cost of your vehicle and your monthly budget. Far from a mere percentage, the interest rate represents the cost of borrowing money from a lender. It’s the premium you pay for the convenience of driving a car now and paying for it over time. A seemingly small difference in interest rate can translate into thousands of dollars over the life of a loan, making it imperative for prospective car buyers to grasp its intricacies and learn how to secure the most favorable terms.

Understanding Car Loan Interest Rates

The interest rate is arguably the most critical component of a car loan, dictating how much extra you’ll pay beyond the vehicle’s sticker price. It’s not just a number on your loan agreement; it’s a financial lever that can significantly lighten or burden your wallet.

Definition and Impact

Simply put, the interest rate is the percentage charged by a lender on the principal amount of your car loan. This charge compensates the lender for the risk of lending money and the time value of that money. For instance, if you borrow $20,000 at a 5% interest rate, you’ll pay 5% of the outstanding balance annually on top of repaying the principal. Over a typical 60-month or 72-month loan term, these charges accumulate, making the final cost of your car considerably higher than its initial sale price. The lower the interest rate, the less you pay in total interest, freeing up your budget for other financial goals or reducing your overall debt burden.

Types of Interest Rates: Fixed vs. Variable

Car loans primarily come with two types of interest rates: fixed and variable.

- Fixed Interest Rates: The vast majority of car loans feature a fixed interest rate. This means the interest rate remains the same for the entire duration of the loan. Your monthly payment for principal and interest will not change, providing stability and predictability in your budget. This consistency is highly valued by borrowers, as it protects them from potential rate increases in the market.

- Variable Interest Rates: While less common for car loans, some lenders may offer variable interest rates. These rates can fluctuate over the loan term based on a specified market index, such as the prime rate. If the index rises, your interest rate and consequently your monthly payments could increase. Conversely, if the index falls, your payments might decrease. Variable rates introduce an element of uncertainty, which can be risky for those on a tight budget, despite potentially offering lower initial rates than fixed loans.

APR vs. Interest Rate

It’s crucial to distinguish between the nominal interest rate and the Annual Percentage Rate (APR). While often used interchangeably, they represent different things in the context of borrowing.

- Interest Rate: This is the percentage applied to the principal balance of your loan to calculate the cost of borrowing money.

- APR (Annual Percentage Rate): The APR provides a more comprehensive measure of the total cost of borrowing. It includes the interest rate plus any additional fees associated with the loan, such as origination fees, processing fees, or discount points. For instance, a loan might have a 4.5% interest rate, but if there are significant fees, its APR could be 4.9% or higher. When comparing loan offers, the APR is generally a better metric to use, as it gives you a truer picture of the overall cost. Lenders are legally required to disclose the APR, allowing consumers to make informed comparisons.

Factors Influencing Your Car Loan Interest Rate

Many elements come into play when a lender determines the interest rate you’ll be offered. Understanding these factors can empower you to improve your financial standing before applying for a loan, potentially securing a significantly lower rate.

Your Credit Score (The Biggest Driver)

Your credit score is arguably the single most influential factor in determining your car loan interest rate. Lenders use credit scores (like FICO scores) to assess your creditworthiness—your likelihood of repaying the loan on time.

- Excellent Credit (780+): Borrowers with excellent credit scores are considered low-risk and typically qualify for the lowest interest rates available, sometimes even 0% APR promotions.

- Good Credit (670-739): Those with good credit will still receive competitive rates, though slightly higher than those with excellent credit.

- Fair Credit (580-669): Borrowers in this range may face higher interest rates as lenders perceive a greater risk.

- Poor Credit (Below 580): Individuals with poor credit scores will encounter the highest interest rates, reflecting a high-risk assessment by lenders. In some cases, they may struggle to secure a loan without a co-signer or a substantial down payment.

A higher credit score signals to lenders that you are a reliable borrower with a history of managing debt responsibly. Conversely, a lower score suggests a higher risk of default, prompting lenders to charge a premium in the form of increased interest to offset that risk.

Loan Term and Down Payment

The length of your loan and the amount of your down payment also play significant roles.

- Loan Term: Shorter loan terms (e.g., 36 or 48 months) generally come with lower interest rates compared to longer terms (e.g., 72 or 84 months). This is because a shorter term reduces the lender’s risk exposure over time. While longer terms result in lower monthly payments, you’ll pay significantly more in total interest due to the extended period and often a higher interest rate.

- Down Payment: A larger down payment reduces the amount you need to borrow, which lowers the lender’s risk. When you have more equity in the vehicle from the start, you’re less likely to become “upside down” (owing more than the car is worth), making you a more attractive borrower and potentially qualifying you for a lower interest rate. A standard recommendation is to put down at least 10-20% for a new car and 20% for a used car.

Vehicle Type (New vs. Used) and Age

The type and age of the vehicle you’re financing can also impact the interest rate.

- New Cars: New car loans typically offer lower interest rates than used car loans. This is because new cars hold their value better initially, making them lower risk for lenders. Additionally, manufacturers often offer special promotional financing rates (sometimes 0% APR) on new vehicles to boost sales.

- Used Cars: Used cars tend to have higher interest rates because they are perceived as higher risk. They depreciate faster, have a shorter lifespan, and may require more maintenance, which could strain a borrower’s ability to repay. Older used cars usually command even higher rates.

Economic Conditions (Federal Reserve Rates)

Broader economic conditions, particularly the federal funds rate set by the Federal Reserve, can influence car loan interest rates. When the Fed raises its benchmark rate, the cost of borrowing for banks increases, and these higher costs are often passed on to consumers in the form of higher interest rates for various loans, including car loans. Conversely, when the Fed lowers rates, consumer loan rates tend to follow suit.

Lender Type and Competition

The type of lender you choose can also affect the rate.

- Banks and Credit Unions: Credit unions often offer slightly lower interest rates than traditional banks due to their non-profit status and focus on member benefits.

- Dealership Financing: While convenient, dealership financing (often arranged through captive finance companies like Ford Credit or Toyota Financial Services) may not always offer the best rates, though they sometimes have promotional rates directly from manufacturers.

- Online Lenders: A growing number of online lenders specialize in car loans and can offer competitive rates, often with streamlined application processes.

The competitive landscape among lenders also plays a role. In a highly competitive market, lenders may lower rates to attract more borrowers.

Strategies to Secure a Lower Car Loan Interest Rate

Proactive steps can significantly improve your chances of securing a more favorable interest rate, saving you money over the life of your car loan.

Improve Your Credit Score Before Applying

Given its paramount importance, taking steps to boost your credit score should be your first priority.

- Pay Bills On Time: Payment history is the most significant factor in your credit score. Ensure all credit card, loan, and utility bills are paid by their due dates.

- Reduce Credit Card Debt: High credit utilization (the amount of credit you’re using versus your total available credit) can negatively impact your score. Pay down revolving balances to below 30% of your credit limit, or even lower.

- Check Your Credit Report for Errors: Obtain free copies of your credit report from Equifax, Experian, and TransUnion via AnnualCreditReport.com. Dispute any inaccuracies, as they could be dragging down your score.

- Avoid Opening New Credit Accounts: Multiple hard inquiries for new credit in a short period can temporarily lower your score.

Shop Around and Compare Offers

Never accept the first loan offer you receive. Different lenders will have different underwriting criteria and offer varying rates based on their risk assessment and business models.

- Get Pre-Approved: Seek pre-approvals from multiple banks, credit unions, and online lenders before you even step foot on a dealership lot. This allows you to compare actual offers side-by-side, giving you leverage during negotiations.

- Use the APR: As mentioned, always compare APRs, not just interest rates, to get a true comparison of the total cost.

- Leverage Offers: If you receive a better offer from one lender, see if another lender (or the dealership) is willing to match or beat it.

Make a Larger Down Payment

As discussed, a larger down payment reduces the loan amount and the lender’s risk, potentially leading to a lower interest rate. Aim for at least 10-20% for a new car and 20% for a used car if feasible. A substantial down payment also reduces your monthly payments and lessens the risk of being upside down on your loan.

Consider a Shorter Loan Term

While longer loan terms offer lower monthly payments, they typically come with higher interest rates and result in more interest paid overall. If your budget allows, opt for the shortest loan term you can comfortably afford. This will not only save you money on interest but also allow you to pay off your vehicle faster.

Refinancing Your Existing Car Loan

If you’ve already financed a car and your credit score has improved, interest rates have dropped, or you’ve found a better offer, consider refinancing. Refinancing replaces your existing loan with a new one, often with a lower interest rate, which can reduce your monthly payment and total interest paid. It’s particularly beneficial if you initially took out a loan with a high interest rate due to poor credit.

The True Cost of Car Loan Interest

Beyond the immediate monthly payment, the cumulative impact of interest can significantly inflate the total cost of your vehicle.

Calculating Your Total Interest Paid

To truly understand the cost, you must look beyond the principal. Take your loan amount, interest rate, and loan term, and calculate the total amount you’ll pay over the life of the loan. Online car loan calculators are excellent tools for this. For example, a $30,000 loan at 5% over 60 months results in approximately $3,950 in total interest paid. The same loan at 8% would accrue over $6,500 in interest. This demonstrates how even a few percentage points can mean thousands of dollars.

The Long-Term Financial Implications

High interest rates can tie up a significant portion of your disposable income for years, limiting your ability to save, invest, or pay down other debts. This opportunity cost is a crucial consideration. A car loan with a manageable interest rate frees up cash flow, allowing for better financial flexibility and progress toward other long-term goals like homeownership or retirement savings. Conversely, being locked into a high-interest loan can create financial strain, making it harder to build wealth.

Beyond the Monthly Payment: Total Cost of Ownership

While the interest rate directly affects the loan payment, it’s essential to view it within the broader context of the total cost of ownership. This includes not just the purchase price and interest, but also insurance, fuel, maintenance, repairs, and depreciation. A low interest rate makes the financing component cheaper, but if the vehicle itself is expensive to maintain or insure, the overall cost of ownership might still be high. Always consider the full financial picture before making a purchase.

Navigating the Car Loan Application Process

Understanding the process will help you avoid common pitfalls and secure the best possible deal.

Gathering Necessary Documentation

Before applying, assemble all necessary documents. This typically includes:

- Proof of Identity: Driver’s license or state ID.

- Proof of Income: Pay stubs, W-2s, or tax returns (if self-employed).

- Proof of Residence: Utility bill, lease agreement.

- Social Security Number: For credit checks.

- Vehicle Information: If you know what car you’re buying (VIN, mileage, etc.).

Having these ready will streamline the application process and show lenders you are prepared.

Understanding Pre-Approval vs. Application

- Pre-Approval: This is a preliminary approval from a lender that states how much you can borrow and at what interest rate, based on a soft credit inquiry. It’s a non-binding offer that gives you significant bargaining power at the dealership.

- Full Application: Once you’ve chosen a vehicle and are ready to finalize the loan, you’ll complete a full application, which involves a hard credit inquiry and a final review of all your documents.

Always aim for pre-approval first to know your financial boundaries and leverage your position.

Avoiding Common Pitfalls

- Focusing Only on Monthly Payments: Don’t let a low monthly payment distract you from a high interest rate or a long loan term that ultimately costs more. Always look at the total cost.

- Accepting Dealership Financing Without Comparing: Dealerships are businesses; they may mark up interest rates to increase their profit. Always compare their offers with your pre-approvals.

- Not Reading the Fine Print: Carefully review all loan documents for hidden fees, prepayment penalties, or unexpected terms.

- Impulse Buying: Take your time. Research both the vehicle and the financing options thoroughly before committing.

By understanding the intricacies of car loan interest rates and employing smart financial strategies, you can significantly reduce the overall cost of your vehicle and ensure your car purchase aligns with your broader financial goals.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.