Understanding the interest rate for a 30-year mortgage is a cornerstone of homeownership and a critical financial decision for millions. It’s not a static number but a dynamic figure influenced by a myriad of economic forces, individual financial health, and lender policies. For prospective homeowners and those looking to refinance, grasping the intricacies behind these rates is essential for making informed choices that can impact their financial well-being for decades. This comprehensive guide will delve into what determines these rates, how to find the best ones, and their profound impact on your long-term financial landscape.

Understanding the 30-Year Fixed-Rate Mortgage

The 30-year fixed-rate mortgage stands as one of the most popular financing options for homebuyers in the United States. Its appeal lies in its long repayment period and predictable monthly payments, offering a sense of security rarely found in other financial products.

Why the 30-Year Mortgage is Popular

The enduring popularity of the 30-year fixed-rate mortgage can be attributed to several key advantages. Primarily, the extended repayment term results in lower monthly payments compared to shorter-term options like a 15-year mortgage for the same loan amount. This affordability makes homeownership accessible to a wider range of individuals and families, allowing them to manage their budgets more effectively and potentially save for other financial goals.

Furthermore, the “fixed-rate” component provides unparalleled predictability. Once the loan is secured, the interest rate remains constant for the entire 30-year duration. This means your principal and interest payment will never change, regardless of market fluctuations. This stability is invaluable for long-term financial planning, protecting homeowners from the volatility of interest rate hikes and providing peace of mind. For many, especially first-time homebuyers, this combination of lower payments and unwavering stability makes the 30-year fixed-rate mortgage the default choice.

How Fixed Rates Work

A fixed-rate mortgage locks in an interest rate for the entire life of the loan. This is in contrast to adjustable-rate mortgages (ARMs), where the interest rate can change periodically after an initial fixed period. With a 30-year fixed mortgage, the monthly payment for principal and interest remains the same from the first payment to the last, assuming you don’t refinance.

The interest rate you secure is determined at the time of closing and is applied to the outstanding principal balance. Early in the loan term, a larger portion of your monthly payment goes towards interest, and a smaller portion towards principal. As the loan matures, this ratio gradually shifts, with more of your payment allocated to reducing the principal balance. This amortization schedule is pre-calculated, allowing homeowners to see precisely how their loan will be repaid over three decades. The consistency of the fixed rate is a powerful shield against economic uncertainty, offering a predictable financial commitment for the long haul.

Key Factors Influencing 30-Year Mortgage Rates

The interest rate you receive on a 30-year mortgage is not pulled from thin air; it’s the result of a complex interplay of broad economic conditions, lender-specific strategies, and your personal financial profile. Understanding these influences is crucial for comprehending why rates fluctuate and what you can do to secure the best possible terms.

Economic Indicators

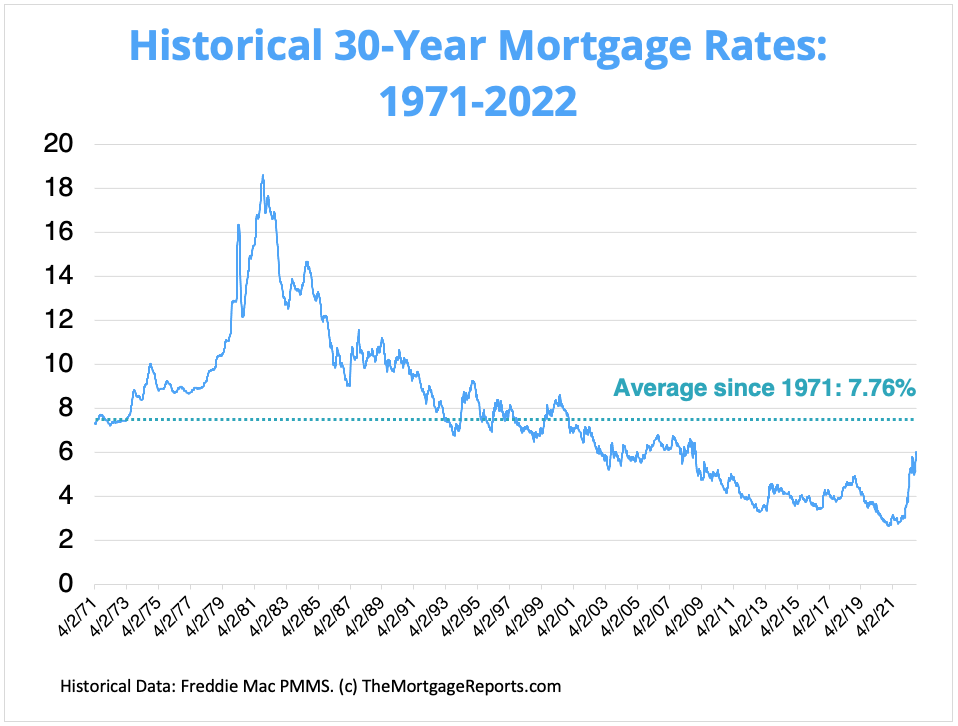

At a macro level, several powerful economic indicators dictate the general direction of mortgage rates. Inflation is a primary driver; when inflation is high or expected to rise, lenders demand higher interest rates to compensate for the reduced purchasing power of future repayment dollars. The Federal Reserve’s monetary policy, particularly its decisions regarding the federal funds rate, indirectly impacts mortgage rates. While the Fed doesn’t directly set mortgage rates, its actions influence the broader interest rate environment, including the yield on Treasury bonds, to which mortgage rates are closely tied. Specifically, the 10-year Treasury yield often serves as a benchmark for 30-year fixed mortgage rates, moving in tandem with them. When the bond market anticipates economic growth or inflation, yields rise, pushing mortgage rates up. Conversely, during periods of economic uncertainty or recession, bond yields often fall, leading to lower mortgage rates.

Lender-Specific Factors

Beyond the broader economy, individual lenders also play a significant role in setting their rates. Each financial institution—whether it’s a large bank, a credit union, or a mortgage broker—has its own business model, overhead costs, and desired profit margins. They also assess risk differently and have varying capacities to originate and service loans. This means that two different lenders might offer slightly different rates on the same day for the same borrower, reflecting their internal cost structures, competitive strategies, and access to capital markets. Lenders also account for their “secondary market execution,” which refers to how they package and sell mortgages to investors. The more efficiently they can do this, the more competitive their rates can be.

Borrower-Specific Factors

Perhaps the most direct influence on the rate you receive is your personal financial situation. Lenders evaluate several key aspects to assess your creditworthiness and the risk associated with lending to you. Your credit score (FICO score) is paramount; a higher score (typically 740+) indicates a lower risk of default, qualifying you for the most favorable rates. Conversely, a lower score will result in a higher interest rate to compensate the lender for the increased risk.

Your debt-to-income (DTI) ratio is another critical factor, calculated by dividing your total monthly debt payments by your gross monthly income. A lower DTI (ideally below 36%) signals that you can comfortably manage your existing debts and take on a new mortgage payment. The size of your down payment also matters significantly. A larger down payment reduces the loan-to-value (LTV) ratio, meaning you’re borrowing less relative to the home’s value. A lower LTV (e.g., 80% or less) is seen as less risky, often leading to better rates and potentially avoiding private mortgage insurance (PMI).

Market Competition and Geography

The competitive landscape among lenders can also influence rates. In areas with many active mortgage lenders, competition can drive rates down as institutions vie for market share. Conversely, in less competitive markets, rates might be slightly higher. Geographic location can also have a subtle impact due to varying state-specific regulations, taxes, and economic conditions that lenders must factor into their pricing models. While less significant than national economic trends, local market dynamics can contribute to minor rate differentials.

How to Find the Best 30-Year Mortgage Rate

Securing the most favorable 30-year mortgage rate requires a proactive and strategic approach. It’s not just about what the market offers, but how you position yourself as a borrower and how diligently you shop around.

Improve Your Financial Profile

Before even applying for a mortgage, taking steps to bolster your financial health can significantly improve the rates you’re offered. Focus on boosting your credit score by paying all bills on time, reducing outstanding debt, and correcting any errors on your credit report. A higher score directly translates to lower perceived risk for lenders and thus, better rates. Simultaneously, work on reducing your debt-to-income ratio by paying down existing loans and avoiding new debt. The less debt you carry relative to your income, the more financially stable you appear. Finally, saving for a larger down payment is incredibly beneficial. A substantial down payment (e.g., 20% or more) not only reduces your loan amount but also lowers your loan-to-value (LTV) ratio, often resulting in a lower interest rate and the elimination of private mortgage insurance (PMI).

Shop Around Extensively

This is arguably the single most important step in finding the best rate. Do not settle for the first quote you receive. Get quotes from multiple lenders including large national banks, smaller community banks, credit unions, and independent mortgage brokers. Each lender has different pricing models, risk assessments, and overheads, meaning their rates and fees can vary considerably even on the same day for the same borrower. Use the same loan scenario (e.g., loan amount, down payment, estimated credit score) across all inquiries to ensure an apples-to-apples comparison. Most mortgage applications within a 45-day window are grouped as a single inquiry for credit scoring purposes, so shopping around will not negatively impact your score if done within this timeframe.

Understand Loan Estimates and Fees

Once you start receiving quotes, lenders are legally required to provide you with a Loan Estimate (LE) within three business days of your application. This standardized document clearly outlines the interest rate, estimated monthly payment, and total closing costs. Pay close attention to the Annual Percentage Rate (APR), which represents the total cost of the loan over its term, including the interest rate and most fees. While the interest rate is what you’ll pay on the principal, the APR gives you a more comprehensive picture of the loan’s true cost. Compare the “Cash to Close” figures and itemized closing costs, looking for fees like origination fees, appraisal fees, title insurance, and prepaid interest. Some lenders might offer a slightly lower interest rate but compensate with higher closing costs, so it’s crucial to analyze both.

Consider Rate Locks

A rate lock is an agreement between you and the lender that guarantees a specific interest rate for a set period, typically 30 to 60 days, while your loan is being processed. This protects you from rising rates during the underwriting period. It’s generally advisable to lock your rate when you’re confident in your lender and have a clear timeline for closing. However, be mindful of the lock period; if your closing gets delayed beyond the lock expiration, you might incur extension fees or risk being subject to current market rates, which could be higher. Some lenders offer a “float down” option, which allows you to take advantage of lower rates if they drop significantly before closing, though this usually comes with a fee.

The Impact of Interest Rates on Your Mortgage

The interest rate on your 30-year mortgage is more than just a number; it’s a powerful financial lever that dictates the affordability of your home, your monthly budget, and the total cost of your investment over three decades.

Monthly Payment Calculations

Even a small change in the interest rate can have a significant impact on your monthly mortgage payment. For example, on a $300,000, 30-year fixed-rate mortgage:

- At 6.00% interest, the principal and interest payment would be approximately $1,798 per month.

- At 6.50% interest, the payment would rise to approximately $1,897 per month – nearly a $100 increase per month.

- At 7.00% interest, the payment jumps to approximately $1,996 per month – almost $200 more than the 6.00% rate.

These seemingly modest percentage point differences accumulate quickly, affecting your household budget and potentially your ability to qualify for the loan in the first place. Lenders use a debt-to-income ratio (DTI) to assess affordability, and a higher monthly payment due to a higher interest rate can push your DTI above their acceptable limits.

Total Cost Over the Loan Term

The long-term effect of interest rates is even more profound. Over 30 years, the compounded interest can add up to hundreds of thousands of dollars. Using the same $300,000 loan example:

- At 6.00%, the total interest paid over 30 years would be approximately $347,380, making the total repayment about $647,380.

- At 6.50%, the total interest paid rises to approximately $382,900, with a total repayment of around $682,900.

- At 7.00%, the total interest paid soars to approximately $418,600, bringing the total repayment to roughly $718,600.

This illustrates that a mere 1% difference in your interest rate can result in tens of thousands, if not over a hundred thousand dollars, in extra interest paid over the life of the loan. This significant difference underscores why diligently shopping for the best rate is crucial; it can save you a substantial sum of money over the long haul.

Refinancing Opportunities

Understanding interest rate movements also opens the door to potential refinancing opportunities. If market rates drop significantly after you’ve secured your initial mortgage, refinancing could allow you to replace your existing loan with a new one at a lower interest rate. This could reduce your monthly payments, decrease the total interest paid over the remaining loan term, or even allow you to shorten your loan term. However, refinancing comes with its own set of closing costs, so it’s essential to perform a break-even analysis to determine if the savings from a lower interest rate outweigh the costs of refinancing. Generally, a drop of at least 0.75% to 1.00% in prevailing rates compared to your current rate makes refinancing worth considering, but individual circumstances always apply.

Future Outlook and Expert Insights

Predicting the precise movement of 30-year mortgage rates is notoriously difficult, akin to forecasting the weather months in advance. However, understanding the factors that influence them and following expert analyses can help you navigate the market more effectively.

Predicting Rate Movements

Mortgage rates are influenced by a complex web of global and domestic economic factors, making precise predictions challenging. Experts typically look at several key indicators: the Federal Reserve’s stance on monetary policy (particularly inflation targets and potential rate hikes/cuts), the health of the job market, consumer spending and confidence, and the yield on the 10-year Treasury bond. Geopolitical events and global economic stability can also introduce volatility. While no one has a crystal ball, the general consensus among economists often provides a range of probable outcomes. For instance, if inflation remains stubbornly high, the Fed might keep interest rates elevated, indirectly pushing mortgage rates up. Conversely, signs of an economic slowdown could prompt the Fed to loosen policy, potentially leading to lower mortgage rates.

Navigating Market Volatility

For prospective homeowners, market volatility can be a source of anxiety. The key to navigating it is to stay informed but not to panic. If you’re actively searching for a home, get pre-approved for a mortgage to understand your borrowing capacity and the current rates you qualify for. When you find a home and are ready to make an offer, be prepared to act quickly if rates are favorable, and consider a rate lock to protect yourself from sudden increases during the escrow period. If rates are trending upwards, it might be wise to secure a lock as soon as possible. If they are falling, you might consider floating your rate for a short period, though this comes with inherent risk.

The Role of Financial Advisors

Given the significant financial implications of a mortgage, consulting with a qualified financial advisor can be invaluable. They can help you assess your overall financial picture, determine how a mortgage payment fits into your long-term goals, and provide personalized advice on debt management, savings, and investment strategies that complement your homeownership aspirations. While a mortgage loan officer will guide you through the loan process, a financial advisor offers a broader, holistic perspective on your financial health, ensuring that your mortgage decision aligns with your overarching wealth-building objectives. They can also help you understand the nuances of different loan products and their suitability for your specific situation.

Conclusion

The interest rate for a 30-year mortgage is far more than just a percentage point; it’s a dynamic indicator of economic health, a reflection of individual creditworthiness, and a profound determinant of your financial future. From the initial monthly payment to the total cost accrued over three decades, every fluctuation carries significant weight. By understanding the intricate factors that influence these rates – from global economic indicators to personal credit scores – and by diligently shopping around, improving your financial profile, and carefully analyzing loan estimates, you empower yourself to make the most informed and advantageous decisions.

As you embark on or continue your homeownership journey, remember that knowledge is your most valuable asset. Staying informed about market trends, being proactive in managing your finances, and seeking expert guidance when needed will enable you to navigate the complexities of mortgage interest rates with confidence and secure a financial foundation that serves you well for the long term.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.