Navigating the landscape of mortgage rates can feel like tracking a moving target, and nowhere is this more evident than when seeking to understand “what is the FHA interest rate today.” For millions of aspiring homeowners, particularly first-time buyers or those with less-than-perfect credit, Federal Housing Administration (FHA) loans represent a vital pathway to homeownership. These government-insured mortgages offer more flexible qualification criteria compared to conventional loans, primarily lower down payment requirements and more lenient credit score guidelines. However, the interest rate attached to an FHA loan is a dynamic figure, fluctuating daily based on a complex interplay of economic forces, market sentiment, and individual borrower profiles.

Understanding today’s FHA interest rate isn’t just about quoting a single number; it’s about grasping the mechanisms that drive these rates, the additional costs associated with FHA financing, and how to position yourself to secure the most favorable terms possible. This deep dive will explore the nuances of FHA loans, the factors influencing their interest rates, and practical strategies for potential homeowners.

Understanding FHA Loans and Their Appeal

The Federal Housing Administration, an agency within the U.S. Department of Housing and Urban Development (HUD), doesn’t lend money directly. Instead, it insures mortgages issued by FHA-approved lenders. This insurance protects lenders from losses if a borrower defaults, which in turn encourages them to offer more accessible financing options to a broader range of borrowers.

What is an FHA Loan?

An FHA loan is a mortgage insured by the FHA. Its primary purpose is to make homeownership more accessible, especially for individuals who might struggle to qualify for a conventional loan due to lower credit scores or limited funds for a large down payment. While FHA loans come with specific guidelines for lenders and borrowers, they remain one of the most popular mortgage options in the United States.

Who Benefits from FHA Loans?

FHA loans are particularly attractive to several demographics:

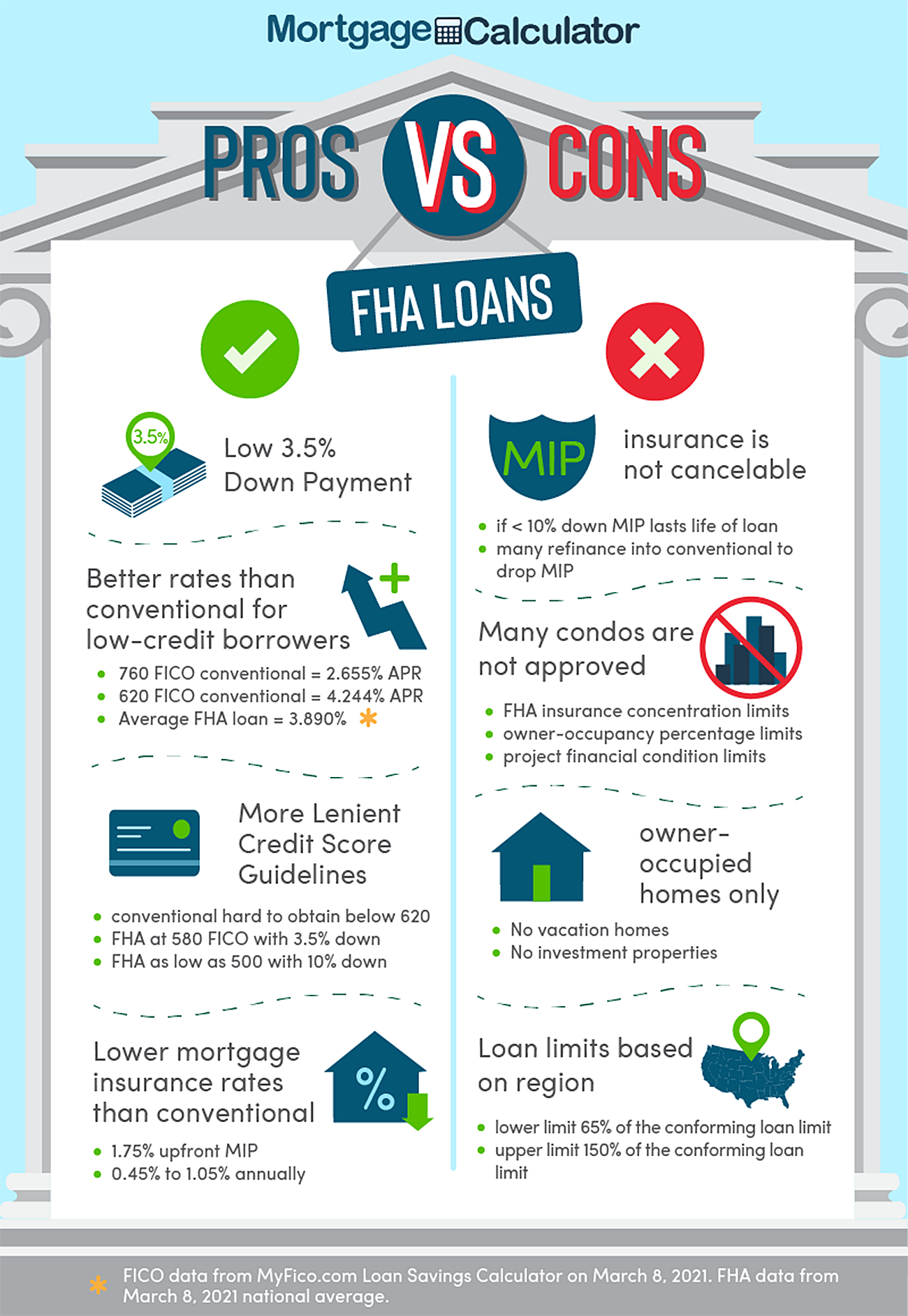

- First-time homebuyers: The low down payment requirement (as little as 3.5% of the purchase price) makes entry into the housing market more attainable.

- Borrowers with lower credit scores: While conventional loans often demand a FICO score of 620 or higher (and often much higher for the best rates), FHA loans can be approved with scores as low as 580 for the 3.5% down payment, and even lower (down to 500) with a 10% down payment.

- Individuals with higher debt-to-income (DTI) ratios: FHA guidelines can be more flexible regarding the percentage of a borrower’s income that goes toward debt payments, though limits still apply.

- Buyers looking for a streamlined refinance: The FHA Streamline Refinance program can help existing FHA borrowers lower their interest rates with minimal paperwork and no appraisal.

Key Requirements for FHA Loans

While FHA loans are more flexible, they still have crucial requirements:

- Credit Score: A minimum FICO score of 580 for a 3.5% down payment. Scores between 500-579 require a 10% down payment.

- Down Payment: At least 3.5% of the purchase price. This can often be sourced from gifts or grants.

- Debt-to-Income (DTI) Ratio: Generally, a front-end ratio (housing costs) of 31% and a back-end ratio (total debts) of 43% are preferred, though exceptions up to 40%/50% are possible with strong compensating factors.

- Property Requirements: The home must meet FHA appraisal standards to ensure it is safe, sound, and secure, and the loan amount must be within FHA loan limits for the specific geographic area.

- Mortgage Insurance Premium (MIP): This is a mandatory component of FHA loans. There’s an Upfront Mortgage Insurance Premium (UFMIP) and an Annual Mortgage Insurance Premium (AMIP). UFMIP is typically 1.75% of the loan amount, paid at closing (or financed into the loan). AMIP is an annual charge, typically ranging from 0.45% to 1.05% of the loan amount, depending on the loan-to-value (LTV) ratio and loan term, paid monthly. This is a critical distinction from the interest rate itself but significantly impacts the total monthly payment.

Deciphering FHA Interest Rates

Unlike some government programs that dictate specific interest rates, the FHA does not set the interest rate for its insured loans. Instead, individual FHA-approved lenders determine their own rates based on various factors. This means that “today’s FHA interest rate” is not a single, universal figure, but rather a range of rates offered by different lenders on any given day.

How FHA Interest Rates are Determined

The interest rate you receive on an FHA loan is a composite of several influences:

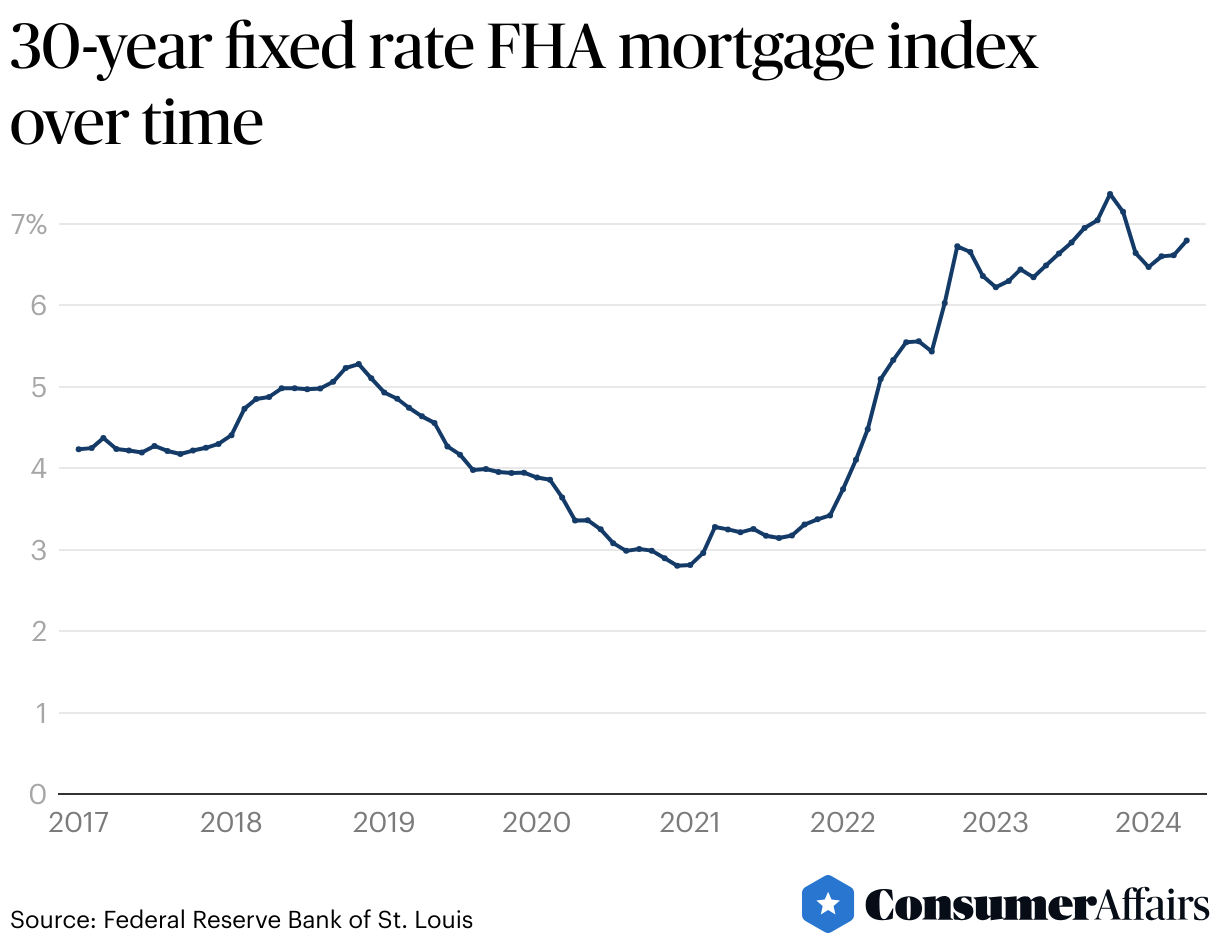

- Broader Market Conditions: This is the most significant factor. FHA rates largely mirror trends in the broader mortgage market, which are heavily influenced by the yield on U.S. Treasury bonds, inflation expectations, the Federal Reserve’s monetary policy, and overall economic stability. When these indicators suggest a stronger economy or higher inflation, interest rates tend to rise.

- Lender’s Risk Assessment: While FHA insurance mitigates much of the risk, lenders still assess factors like the borrower’s credit score (even within FHA’s flexible guidelines), debt-to-income ratio, and down payment amount. A borrower with a higher credit score or a larger down payment (even if only 5% instead of 3.5%) might qualify for a slightly lower rate.

- Lender’s Overhead and Profit Margins: Each lender has its own operational costs and profit targets, which are factored into the rates they offer.

- Loan Term: Shorter loan terms (e.g., 15-year fixed) typically carry lower interest rates than longer terms (e.g., 30-year fixed) because the lender’s risk is spread over a shorter period.

Fixed vs. Adjustable Rate FHA Loans

Most FHA borrowers opt for a fixed-rate mortgage, typically a 30-year fixed loan. With a fixed rate, your interest rate and principal and interest payment remain constant for the entire life of the loan, providing predictable monthly housing costs. This stability is highly valued by homeowners.

Less common, but available, are Adjustable-Rate Mortgages (ARMs) insured by the FHA. These loans start with a lower fixed rate for an initial period (e.g., 3, 5, 7 years), after which the interest rate adjusts periodically based on a predetermined index plus a margin. While ARMs can offer lower initial payments, they introduce interest rate risk, as future payments could increase significantly.

The Role of Mortgage Insurance Premium (MIP)

It’s crucial to distinguish between the FHA interest rate and the Mortgage Insurance Premium (MIP). As mentioned, MIP is a mandatory insurance cost for FHA loans, consisting of an Upfront MIP (UFMIP) and an Annual MIP (AMIP). While not part of the interest rate, MIP significantly adds to your monthly mortgage payment. For many FHA loans, the annual MIP continues for the entire loan term, regardless of how much equity you build. This can make the effective cost of an FHA loan higher than a conventional loan with a similar interest rate, especially if you have a lower down payment.

Factors Influencing Today’s FHA Interest Rates

To truly understand “what is the FHA interest rate today,” one must appreciate the forces that exert constant pressure on these rates. Mortgage rates are a dynamic reflection of the broader economy.

Economic Indicators

A host of economic data points influence the bond market, which in turn dictates mortgage rates:

- Inflation Reports: Higher inflation erodes the purchasing power of money, leading investors to demand higher yields on bonds to compensate for this loss. This upward pressure on bond yields translates to higher mortgage rates.

- Employment Data: Strong job growth and low unemployment typically signal a robust economy, which can lead to inflationary pressures and higher interest rates. Conversely, weak employment data can signal an economic slowdown, potentially leading to lower rates.

- Gross Domestic Product (GDP) Growth: A strong GDP indicates economic expansion, which can also contribute to inflationary expectations and higher rates.

- Consumer Confidence: High consumer confidence can stimulate spending, potentially leading to economic growth and higher rates.

The Bond Market

The U.S. Treasury bond market is a critical barometer for mortgage rates. Long-term mortgage rates are closely correlated with the yield on the 10-year Treasury note. When bond yields rise, mortgage rates generally follow suit. This is because mortgage-backed securities (MBS), which are a primary component of the secondary mortgage market, compete with Treasury bonds for investor capital. To attract investors, MBS must offer yields competitive with or better than government bonds.

Federal Reserve Actions

While the Federal Reserve does not directly set mortgage rates, its actions have a profound indirect impact. The Fed influences short-term interest rates through its federal funds rate target. Changes to this rate can affect the cost of borrowing for banks, which then trickle down to various consumer loans, including mortgages. The Fed’s commentary on the economy and its bond-buying or selling programs (Quantitative Easing/Tightening) also significantly sway market sentiment and long-term interest rates.

Lender-Specific Factors

Beyond the broader economy, individual lenders contribute to rate variations:

- Operational Costs: Each lender has different overhead costs, staffing levels, and technological investments, which are built into their rate offerings.

- Profit Margins: Lenders set their rates to achieve specific profit targets.

- Competitive Landscape: In a highly competitive market, lenders may slightly lower their rates to attract more borrowers.

- Points: Borrowers can sometimes “buy down” their interest rate by paying discount points at closing. Each point typically costs 1% of the loan amount and can reduce the interest rate by a certain fraction.

Borrower-Specific Variables

Even with all the external factors, your individual financial profile plays a crucial role:

- Credit Score: While FHA is flexible, a higher FICO score (e.g., 680 vs. 580) within the FHA guidelines will almost always qualify you for a better interest rate from a lender.

- Down Payment Amount: While 3.5% is the minimum, a larger down payment (e.g., 5% or 10%) can signal lower risk to a lender, potentially earning you a slightly more favorable rate.

- Loan Term: As noted, 15-year fixed FHA loans typically have lower rates than 30-year fixed FHA loans.

- Debt-to-Income Ratio: A lower DTI ratio indicates greater financial stability and less risk for the lender.

How to Find the Best FHA Interest Rate Today

Given the variability, finding the “best” FHA interest rate today requires diligent effort and strategic planning.

Shop Around Extensively

This is arguably the most critical step. Do not settle for the first quote you receive. Contact multiple FHA-approved lenders, including large banks, smaller credit unions, and independent mortgage brokers. Each lender has different pricing structures, risk assessments, and overheads. Obtaining quotes from at least three to five different sources within a short period (typically 14-45 days, as multiple mortgage inquiries within this timeframe usually count as a single hard inquiry for credit scoring purposes) allows you to compare offers accurately.

Improve Your Financial Profile

Before applying, take steps to strengthen your financial standing:

- Boost Your Credit Score: Pay bills on time, reduce revolving credit balances, and avoid taking on new debt. A higher score translates to lower perceived risk and potentially better rates.

- Reduce Debt: A lower debt-to-income ratio signals greater financial stability, which can be favorable for lenders.

- Save for a Larger Down Payment: While FHA allows a low down payment, putting down more cash, if feasible, can sometimes lead to slightly better rates or reduce your loan amount, thereby lowering your overall borrowing cost.

Understand the APR vs. Interest Rate

When comparing loan offers, pay close attention to both the interest rate and the Annual Percentage Rate (APR). The interest rate is simply the cost of borrowing the principal. The APR, however, includes the interest rate plus other loan costs, such as origination fees, discount points, and some closing costs. The APR provides a more comprehensive measure of the true annual cost of the loan and is an excellent tool for comparing different loan products.

Lock In Your Rate Strategically

Once you find a desirable rate, you’ll need to decide when to “lock” it. A rate lock guarantees that rate for a specific period (e.g., 30, 45, or 60 days) while your loan processes. If rates are trending downward, you might consider floating your rate (not locking it immediately) for a short period, though this carries the risk that rates could also rise. If rates are volatile or trending upward, locking in a favorable rate can provide peace of mind. Discuss the best strategy with your loan officer.

Beyond the Rate: Total Cost and Long-Term Strategy

While securing a low FHA interest rate is important, it’s only one piece of the homeownership puzzle. Understanding the total cost and having a long-term financial strategy are equally crucial.

The Impact of Mortgage Insurance (MIP) on Total Cost

As discussed, the mandatory FHA MIP (Upfront and Annual) significantly increases the overall cost of an FHA loan. For most FHA loans with a down payment of less than 10%, the annual MIP will remain for the entire life of the loan. This means even if you build substantial equity, you’ll continue paying for mortgage insurance. This is a key difference from conventional loans, where private mortgage insurance (PMI) can typically be canceled once you reach 20-22% equity. Understanding this long-term cost is vital for budgeting and future planning.

Considering Refinancing in the Future

The housing and financial markets are always evolving. If interest rates drop significantly after you’ve secured your FHA loan, or if your financial situation improves to qualify for a conventional loan, refinancing could be a smart move. An FHA Streamline Refinance can help reduce your interest rate with less hassle, while a cash-out refinance allows you to tap into your home equity. Many FHA borrowers eventually refinance into a conventional loan to eliminate the ongoing MIP once they’ve built sufficient equity.

Financial Planning for Homeownership

Beyond your monthly mortgage payment (principal, interest, MIP), remember to factor in other homeownership costs:

- Property Taxes: These are typically included in your escrow payment but are a significant annual expense.

- Homeowner’s Insurance: Also usually part of escrow.

- Utilities: Heating, cooling, water, electricity, internet.

- Maintenance and Repairs: Set aside a percentage of your home’s value annually for unexpected repairs and routine upkeep.

- Emergency Fund: Ensure you have a robust emergency fund to cover at least 3-6 months of living expenses, separate from your home savings.

In conclusion, “what is the FHA interest rate today” is a question with a multi-faceted answer. It reflects not just the daily fluctuations of the market but also your individual financial health and the specific offerings of various lenders. By understanding the components of FHA loans, diligently shopping for the best terms, and planning for the total cost of homeownership, you can successfully navigate the process and achieve your dream of owning a home. Proactive research and engagement with multiple lenders are your strongest tools in securing the most favorable FHA interest rate and overall loan terms available to you today.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.