In the realm of personal finance and legal strategy, the term “immediate family” is far more than a sentimental descriptor of one’s household. It is a precise legal and financial classification that determines eligibility for benefits, the distribution of assets, tax obligations, and employment rights. Whether you are drafting a will, applying for a life insurance policy, or navigating the complexities of workplace benefits, understanding how various institutions define your “immediate family” is critical to securing your financial future.

While the colloquial definition might include anyone you share a close bond with, financial and legal entities operate under much stricter parameters. These definitions can shift depending on whether you are dealing with the Internal Revenue Service (IRS), a private insurance provider, or a corporate HR department. This guide explores the multifaceted definitions of immediate family through the lens of personal finance and wealth management.

The Core Definitions Across Financial Landscapes

The definition of immediate family is rarely universal. Instead, it is a modular term that adjusts based on the regulatory environment. At its most basic level, the “nuclear” definition is the standard, but as financial complexity increases, so does the scope of the term.

The Legal Standard: Spouses, Children, and Parents

In the vast majority of financial and legal contexts, the primary tier of immediate family consists of your spouse, your children (including adopted children), and your parents. This “first-degree” relationship is the most legally protected. For example, in the event of an individual passing away without a will (intestacy), these are the individuals who are first in line for asset distribution under most state laws. From a financial planning perspective, these individuals are often the automatic beneficiaries of government programs like Social Security.

Broadening the Scope: Siblings and Grandparents in Financial Terms

As we move into “second-degree” relatives, the definition becomes more fluid. Many financial institutions, particularly in the context of “family office” wealth management or private banking, include siblings, grandparents, and grandchildren in the definition of immediate family. However, this is not a guarantee. For instance, while a sibling might be considered immediate family for a bereavement leave policy at a corporation, they may not be considered a “dependent” for tax purposes unless specific financial support thresholds are met. Distinguishing between these layers is essential for accurate estate planning and tax strategy.

Why the Definition Matters for Your Personal Finances

Understanding who qualifies as immediate family is a fundamental component of risk management. If you assume someone is covered under your financial umbrella when they are not, it can lead to devastating out-of-pocket expenses or the loss of generational wealth.

Insurance Policies and Beneficiary Designations

Life, health, and disability insurance are perhaps the most sensitive to the definition of immediate family. In health insurance, “immediate family” usually dictates who can be added to a family plan as a dependent. Typically, this is limited to a spouse and children under the age of 26.

In life insurance, while you can technically name anyone as a beneficiary, the “insurable interest” doctrine often requires a familial or financial connection. If you are setting up a trust or a complex insurance strategy to offset estate taxes, the definition of immediate family determines how the policy is structured to avoid “incidents of ownership” that could trigger unwanted tax liabilities.

Tax Implications and Household Credits

The IRS has its own set of rules regarding who constitutes a family member for the purpose of credits and deductions. The “Qualifying Child” and “Qualifying Relative” tests are the gold standards here. To claim someone as a dependent—which can significantly lower your taxable income through various credits—you must prove not only a relationship but also a residency and support requirement.

Furthermore, the “Family Attribution Rules” in the tax code are designed to prevent families from splitting income or assets to move into lower tax brackets. For business owners, these rules mean that stock owned by a spouse, child, or parent may be attributed to you, affecting your status as a majority shareholder or your eligibility for certain small business tax breaks.

Workplace Benefits and the Immediate Family Clause

For most professionals, the definition of immediate family is most frequently encountered in the employee handbook. These definitions govern everything from your healthcare premiums to your ability to take time off during a crisis.

Understanding FMLA and Bereavement Leave

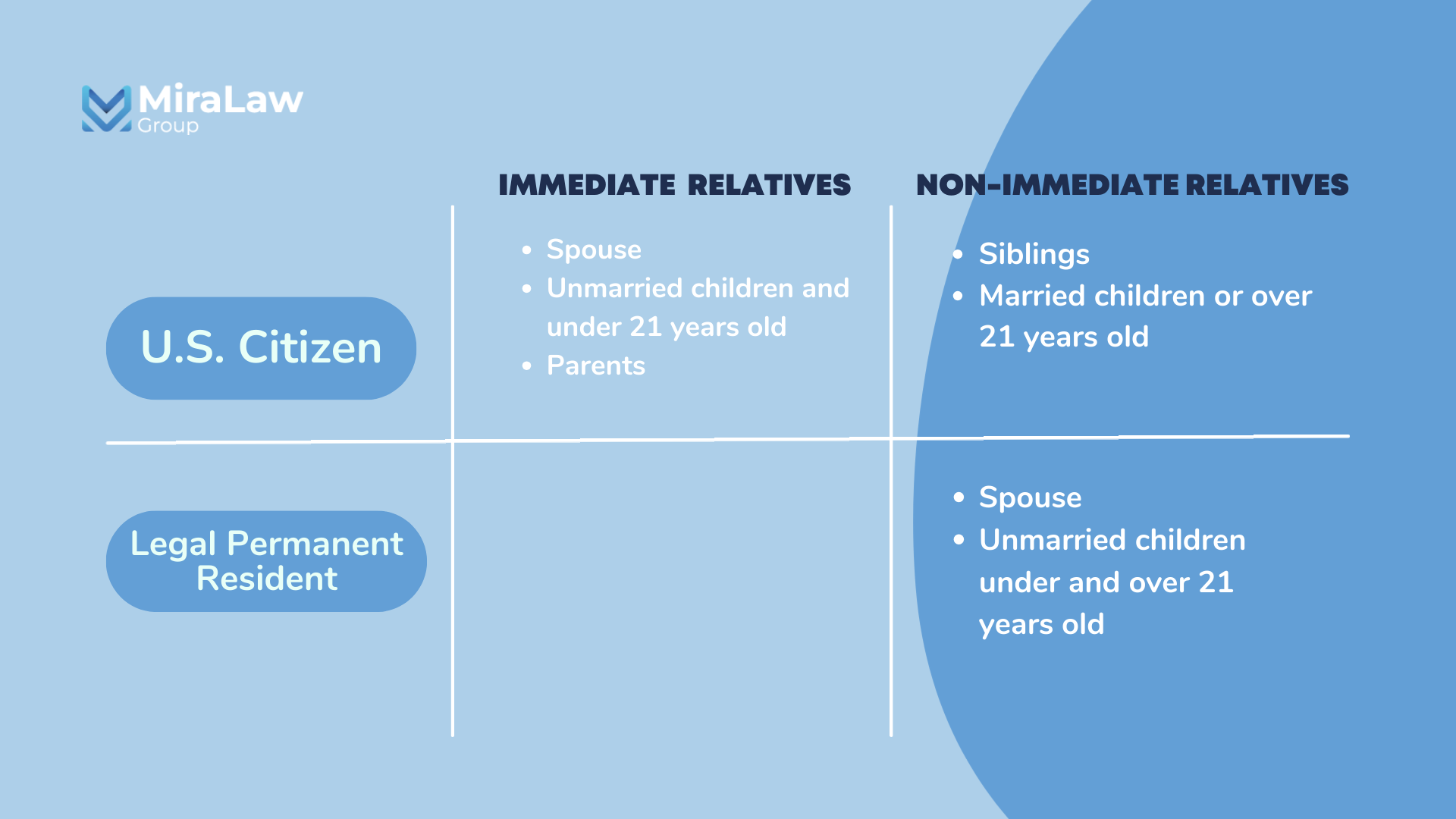

The Family and Medical Leave Act (FMLA) is a federal law that allows eligible employees to take unpaid, job-protected leave for specified family and medical reasons. However, the FMLA’s definition of “immediate family” is relatively narrow: it includes a spouse, parent, and child. It notably excludes siblings, grandparents, and in-laws unless they stood “in loco parentis” (acting as a parent) when the employee was a child.

Conversely, corporate bereavement policies are often broader but vary wildly between companies. Some firms include “domestic partners” and “step-relatives” in their definition, while others do not. From a financial wellness perspective, knowing these boundaries helps you prepare for potential income gaps during times of family emergency.

Health Insurance and Dependent Coverage

The financial impact of “dependent” definitions cannot be overstated. With the rising costs of healthcare, the ability to keep a child on a parent’s plan or to include a spouse is a significant “shadow” salary. However, many employers are now implementing “working spouse surcharges” or excluding spouses who have access to their own employer-sponsored insurance. Understanding the fine print of your company’s definition of a “covered dependent” is a vital part of annual budgeting and open enrollment strategy.

Estate Planning and Wealth Transfer

The ultimate test of the “immediate family” definition occurs during the transfer of wealth. How you define your family in your legal documents will dictate the ease with which your assets move to the next generation.

Intestate Succession: Who Inherits Without a Will?

If you fail to define your family through a last will and testament or a revocable living trust, the state will do it for you through intestate succession laws. Most states prioritize the “immediate family” in a specific order: spouse, then children, then parents, then siblings. If you have a non-traditional family structure—such as a long-term partner to whom you are not legally married—they may be legally excluded from your estate entirely, regardless of your intentions. This is why financial advisors emphasize legal documentation to override default statutory definitions.

Trusts and “Bloodline” Protections

In high-net-worth wealth management, the definition of immediate family is often narrowed to “lineal descendants” to keep assets within a specific bloodline. “Bloodline Trusts” are designed to ensure that if a child gets divorced, the family inheritance stays with the child and grandchildren (the immediate family) rather than being divided with an ex-spouse (the former family member). Defining these terms with precision in a trust instrument is a powerful tool for asset protection and ensuring that wealth serves its intended purpose for generations.

Navigating Modern Family Dynamics in Finance

The traditional definition of the nuclear family is evolving, and the world of personal finance is slowly catching up. For those in non-traditional or blended families, the “default” definitions can often be a hurdle.

Blended Families and Step-Relationships

For financial purposes, step-children and step-parents are not always automatically considered immediate family. In the eyes of the law, unless a step-child has been legally adopted, they may not have the same inheritance rights or eligibility for certain government benefits as a biological child. For families in this category, it is essential to use specific legal designations—such as naming step-children explicitly in insurance policies and wills—to ensure they are treated as part of the immediate financial circle.

Domestic Partnerships and Legal Recognition

While the legalization of same-sex marriage provided a uniform federal definition for “spouse,” many couples still choose domestic partnerships or cohabitation. Financially, this is a complex path. Many private companies offer benefits to domestic partners, but the IRS does not recognize them for joint tax filing. This creates a “definition gap” where a partner might be immediate family for health insurance but a “stranger” for estate tax exemptions. Navigating this requires a bespoke financial plan that uses contracts and trusts to replicate the protections naturally afforded to married couples.

Conclusion: Defining Your Financial Circle

The definition of “immediate family” is not a one-size-fits-all concept. It is a strategic designation that changes based on the financial task at hand. For the savvy investor or head of household, the goal is to align your legal documents, insurance policies, and employment benefits with your actual family reality.

By understanding how the IRS, your employer, and your state government define your inner circle, you can identify gaps in your coverage and vulnerabilities in your estate plan. Whether you are expanding your family, entering a new marriage, or planning your legacy, being precise about who counts as “immediate” is the first step toward long-term financial security and peace of mind. Proper planning ensures that your definitions—not a default legal statute—dictate how your wealth is protected and shared.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.