For countless veterans, active-duty service members, and eligible surviving spouses, the VA home loan program represents a cornerstone of their financial well-being, offering unparalleled access to homeownership. A critical component of securing this benefit is understanding the associated interest rate, which directly impacts monthly payments and the total cost of the loan over its lifetime. Unlike a single, universal rate, VA loan interest rates are dynamic, influenced by a confluence of market forces, lender policies, and individual borrower characteristics. Navigating these variables requires diligence and a strategic approach to ensure beneficiaries secure the most favorable terms available.

Understanding VA Home Loan Interest Rates

The journey to comprehending VA home loan interest rates begins with recognizing their multifaceted nature. While the Department of Veterans Affairs guarantees a portion of these loans, thereby reducing risk for lenders, the VA itself does not set interest rates. Instead, rates are determined by private lenders, including banks, credit unions, and mortgage companies, operating within a competitive market landscape.

The Nature of VA Loan Rates

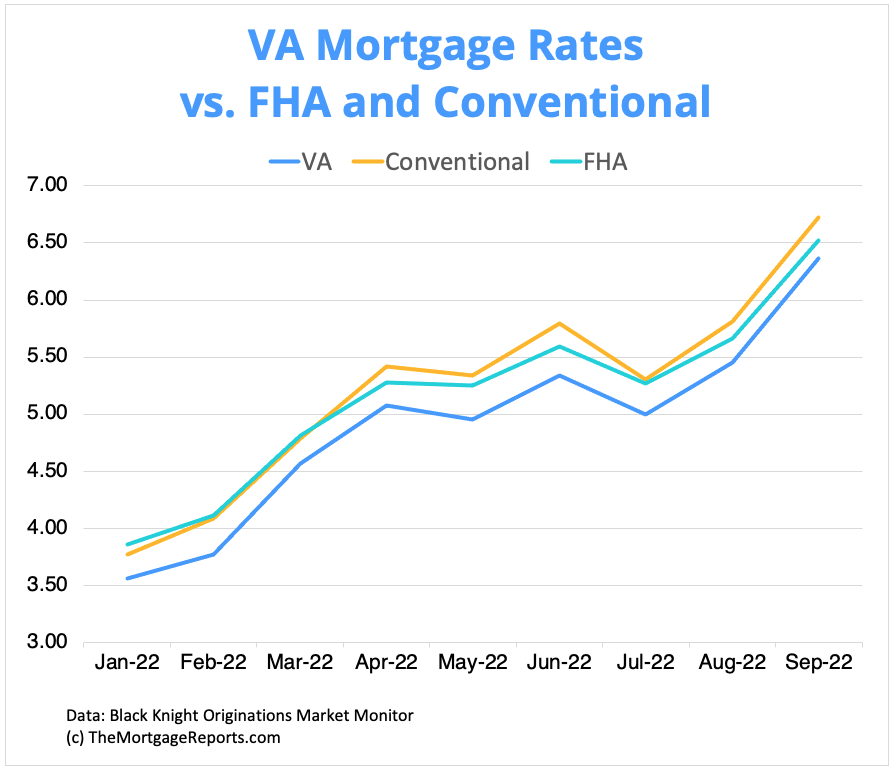

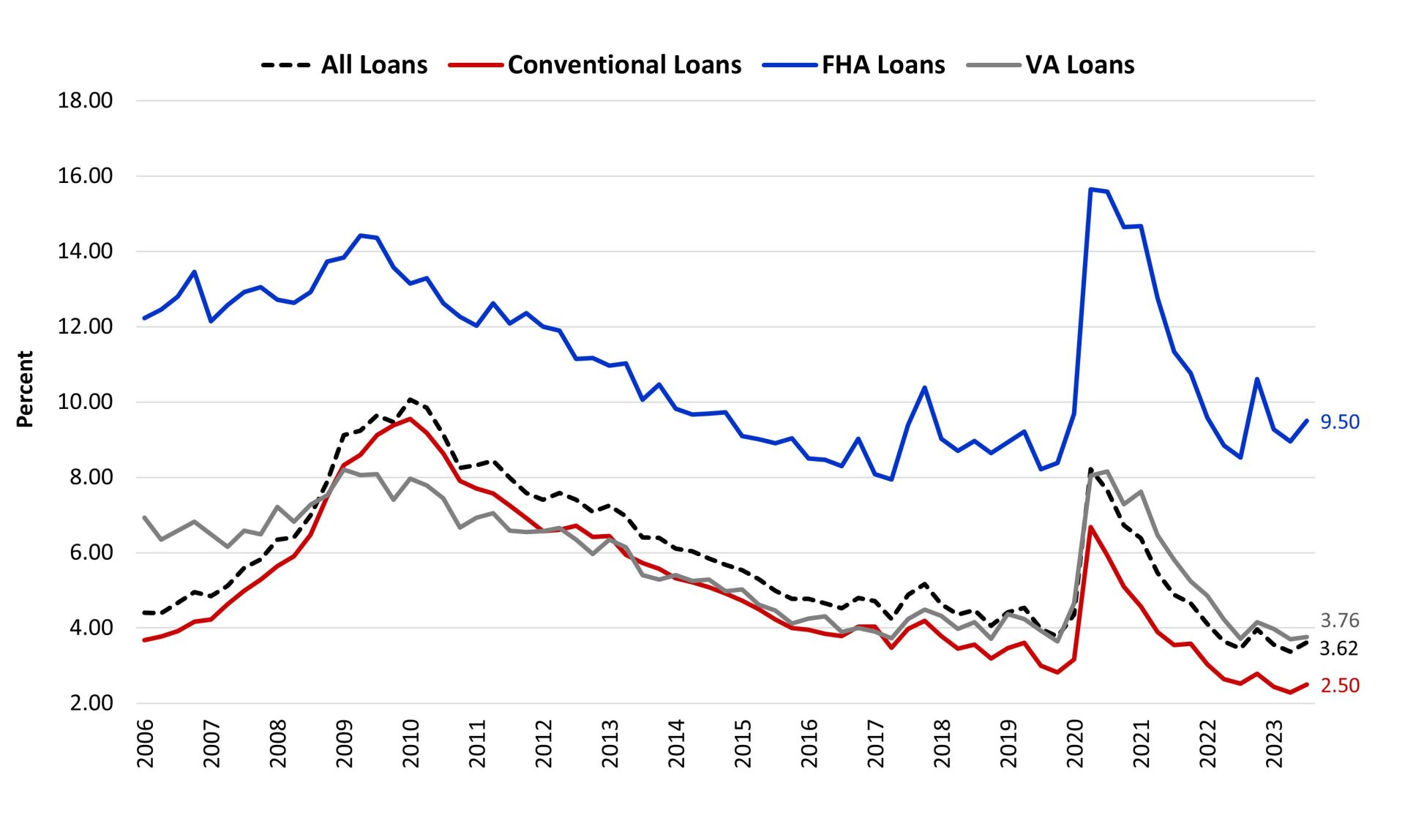

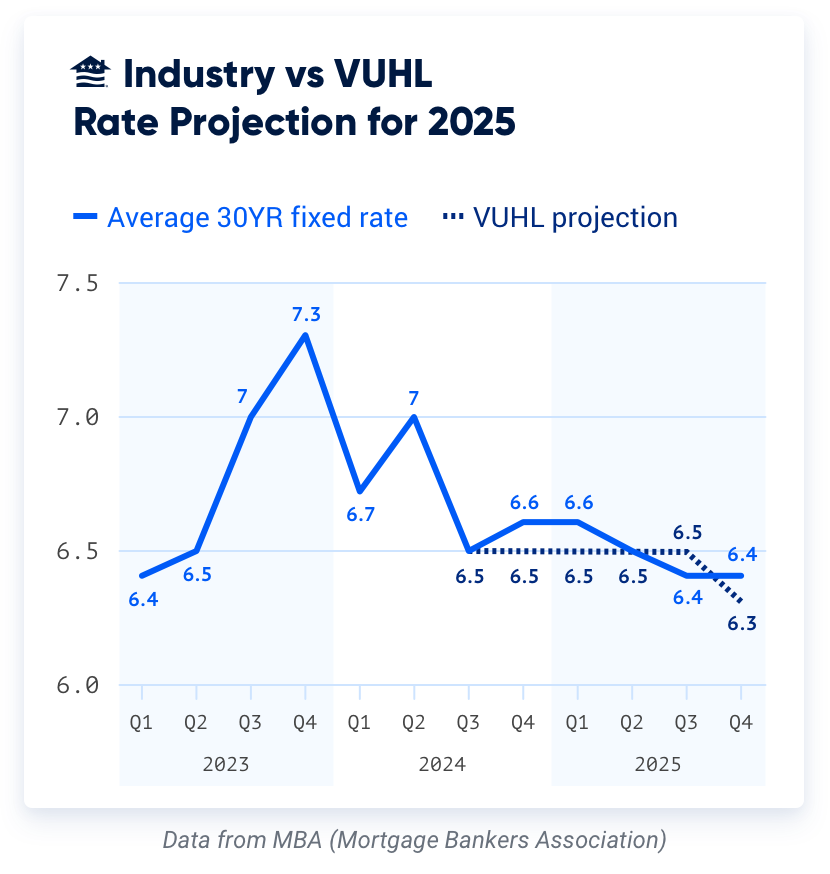

It’s crucial to understand that there isn’t one “current VA home loan interest rate” published by the VA. Rather, rates fluctuate daily, sometimes even hourly, reflecting broader economic trends and the specific pricing models of individual lenders. This means that a borrower contacting five different VA-approved lenders on the same day might receive five slightly different rate quotes, even for the same loan product. The underlying principle is that lenders are competing for your business, and their rates reflect their cost of funds, overhead, and desired profit margins.

Key Components of Your Rate

When evaluating VA loan offers, it’s important to differentiate between the quoted interest rate and the Annual Percentage Rate (APR).

- Interest Rate: This is the percentage you pay on the principal balance of your loan. It directly determines the amount of your monthly principal and interest payment. A lower interest rate translates to lower monthly payments and less interest paid over the life of the loan.

- Annual Percentage Rate (APR): The APR provides a more comprehensive measure of the total cost of borrowing. It includes the interest rate plus certain other charges you pay to get the loan, such as the VA funding fee, origination fees, and discount points. Because it incorporates these additional costs, the APR is almost always higher than the simple interest rate. Comparing APRs across different lenders can give you a clearer picture of which loan is truly less expensive overall.

- Fixed vs. Adjustable Rates: Most VA loan borrowers opt for a fixed-rate mortgage, where the interest rate remains constant for the entire life of the loan, offering predictable monthly payments. Adjustable-Rate Mortgages (ARMs) for VA loans are also available, where the interest rate can change periodically after an initial fixed period. While ARMs can sometimes offer a lower initial rate, they introduce payment uncertainty, making them less common for VA borrowers seeking stability.

Factors Influencing VA Loan Interest Rates

The variability of VA loan interest rates stems from a complex interplay of macroeconomic forces, lender-specific strategies, and the individual borrower’s financial profile. Understanding these influences is key to anticipating rate movements and positioning oneself for the best possible offer.

General Market Conditions

Broader economic factors play a significant role in setting the baseline for all mortgage rates, including VA loans.

- Federal Reserve Policy: While the Federal Reserve does not directly set mortgage rates, its actions significantly impact them. When the Fed raises or lowers the federal funds rate, it influences the cost of borrowing for banks, which then trickles down to consumer loan products.

- Inflation Expectations: Lenders factor in inflation when setting rates. If inflation is expected to rise, lenders will demand higher interest rates to compensate for the reduced purchasing power of future payments.

- Economic Indicators: Reports on employment, GDP growth, and consumer confidence all paint a picture of the economy’s health. Strong economic data can sometimes lead to higher rates as it might signal future inflation, while weaker data might suggest the opposite.

- Treasury Yields: Mortgage rates often track the yield on the 10-year Treasury note. When Treasury yields rise, mortgage rates typically follow suit, and vice versa. This is because mortgage-backed securities (MBS), which are packaged mortgages sold to investors, compete with Treasuries for investor capital.

Lender-Specific Factors

Beyond market conditions, individual lenders apply their own internal criteria and business models to set rates.

- Overhead Costs: Lenders have operating expenses, and these are factored into the rates they offer. More efficient lenders might be able to offer slightly lower rates.

- Profit Margins: Lenders are businesses, and they need to make a profit. Their desired profit margin will influence the rates they quote.

- Loan Volume: Lenders with higher loan volumes might be able to offer more competitive rates due to economies of scale.

- Competition: The competitive landscape among VA-approved lenders also plays a role. In a highly competitive market, lenders may lower rates to attract borrowers.

Borrower-Specific Factors

Even when market conditions are stable, an individual’s financial situation can significantly impact the specific rate they are offered.

- Credit Score: While the VA loan program is known for being more forgiving than conventional loans regarding credit, a higher credit score (typically FICO scores above 720) signals lower risk to lenders, often translating into access to the lowest available interest rates. Conversely, lower scores might lead to slightly higher rates.

- Debt-to-Income (DTI) Ratio: This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI indicates that you have more disposable income to cover your mortgage payments, making you a less risky borrower and potentially qualifying you for better rates.

- Loan Term: The length of your loan significantly impacts the interest rate. Shorter terms, such as a 15-year VA mortgage, typically come with lower interest rates than longer terms, like a 30-year VA mortgage. While the monthly payments are higher for a 15-year loan, you pay significantly less interest over the life of the loan.

- Loan Type (Purchase vs. Refinance): Rates for purchase loans can differ from those for refinancing options like a VA Interest Rate Reduction Refinance Loan (IRRRL) or a VA cash-out refinance. IRRRLs, designed solely to lower your rate or switch from an ARM to a fixed rate, often have streamlined processes and potentially favorable rates.

- Discount Points: Borrowers have the option to pay “discount points” at closing to effectively “buy down” their interest rate. Each point typically costs 1% of the loan amount and can reduce the interest rate by a fraction of a percent. Whether paying points is worthwhile depends on how long you plan to stay in the home and the long-term savings generated.

How to Find the Most Current VA Home Loan Interest Rates

Given the dynamic nature of VA loan interest rates, proactively seeking out and comparing offers is paramount to securing the best deal.

Online Rate Comparison Tools

Numerous websites offer online tools that provide estimated VA loan interest rates. These tools can be a good starting point to get a general idea of current market rates. However, it’s crucial to remember that these are often generalized averages or promotional rates and may not reflect the exact rate you’d qualify for. They serve as a guide, not a definitive quote.

Contacting Multiple VA-Approved Lenders

The most effective way to determine your actual current VA home loan interest rate is to directly contact several VA-approved lenders. This step cannot be overstated. By shopping around, you force lenders to compete for your business, often leading to better offers. Aim to get personalized quotes from at least three to five different lenders within a short timeframe (e.g., 24-48 hours) to ensure you’re comparing similar market conditions.

When contacting lenders, be prepared to provide:

- Your Certificate of Eligibility (COE) or an agreement to help you obtain it.

- Basic financial information (income, assets, debts).

- Your credit score range (if known).

- Details about the property you intend to purchase (if applicable).

Daily Market Updates

Stay informed about general market trends by consulting reputable financial news sources, mortgage industry publications, and economic reports. While these won’t give you your specific rate, they can help you understand whether rates are generally rising, falling, or holding steady, which can inform your decision-making process for when to lock in a rate.

Getting a Loan Estimate

Once you’ve applied for a mortgage, lenders are required by law to provide you with a “Loan Estimate” within three business days. This standardized document clearly outlines the interest rate, APR, monthly payment, closing costs, and other essential terms. Critically, it allows you to easily compare offers from different lenders side-by-side. Pay close attention to the “rate lock” details, which specify how long the quoted interest rate is guaranteed.

Optimizing Your VA Home Loan Rate

Securing a favorable VA home loan interest rate involves more than just finding a lender; it requires strategic financial preparation and informed decision-making.

Improve Your Credit Score

Before applying, take steps to improve your credit score. Pay down existing debts, especially revolving credit balances. Make all payments on time and avoid opening new lines of credit. Regularly check your credit report for errors and dispute any inaccuracies. A higher credit score can significantly reduce the interest rate you’re offered.

Reduce Your DTI

Lowering your debt-to-income ratio demonstrates to lenders that you have ample capacity to manage a new mortgage payment. Focus on paying off high-interest debts like credit card balances or personal loans. Even a small reduction in monthly debt obligations can positively impact your DTI and potentially your interest rate.

Understand Discount Points

Evaluate whether paying discount points to lower your interest rate makes financial sense. Calculate the “break-even point” – how long it will take for the savings from the lower interest rate to offset the upfront cost of the points. If you plan to stay in the home for a long time, buying down the rate could yield significant long-term savings. If you anticipate moving sooner, it might not be a wise investment.

Consider the Loan Term

Decide between a 15-year or 30-year loan term based on your financial goals and comfort level. While a 15-year loan typically comes with a lower interest rate and allows you to pay off your home faster, it also results in higher monthly payments. A 30-year loan offers lower monthly payments, providing more financial flexibility, but you’ll pay more interest over the loan’s duration.

Get Pre-Approved

Obtaining a VA loan pre-approval is a crucial step. It involves a lender reviewing your financial information to determine how much you can afford and at what estimated rate. A pre-approval letter not only strengthens your offer to sellers but also gives you a concrete understanding of your potential interest rate and monthly payments, allowing you to budget more accurately. Some lenders may even allow you to lock in an estimated rate during the pre-approval process, offering protection against rising rates for a limited time.

Beyond the Rate: Other VA Loan Benefits and Considerations

While the interest rate is a primary concern, the VA home loan program offers several other significant benefits and features that contribute to its overall value, making it one of the most advantageous mortgage options available.

No Down Payment Requirement

One of the most compelling advantages of a VA loan is the ability to purchase a home with no down payment, provided the purchase price does not exceed the VA county loan limits (which are quite high in most areas) and you have full entitlement. This saves eligible borrowers from the significant upfront financial burden associated with conventional mortgages.

No Private Mortgage Insurance (PMI)

Unlike conventional loans with less than a 20% down payment, VA loans do not require private mortgage insurance (PMI). PMI is an additional monthly cost designed to protect the lender in case you default. The absence of PMI for VA loans can save borrowers hundreds of dollars each month, significantly reducing the overall cost of homeownership compared to other loan types.

VA Funding Fee

The VA funding fee is a one-time fee paid directly to the VA. It helps to offset the costs of the program for taxpayers and ensures its continued availability. The amount of the fee varies based on factors such as your service type, whether you’re a first-time or subsequent VA loan user, and your down payment amount (if any). Importantly, certain veterans, such as those receiving VA compensation for service-connected disabilities, are exempt from paying the funding fee. This fee can typically be financed into the loan, meaning you don’t have to pay it out-of-pocket at closing.

Closing Costs

While the VA limits what fees a veteran can be charged, closing costs are still a factor. These are various fees and charges associated with finalizing a mortgage loan, including appraisal fees, title insurance, recording fees, and attorney fees. The VA does allow sellers to pay some or all of a buyer’s closing costs, which can be a valuable negotiation point.

Assumability

A unique feature of VA loans is their assumability. This means that a qualified buyer, military or civilian, can take over your existing VA mortgage, including your current interest rate, which can be particularly attractive if interest rates rise in the future. This feature can make your home more marketable when it’s time to sell.

In conclusion, understanding the current VA home loan interest rate involves navigating a complex landscape of market indicators, lender specifics, and personal financial health. By actively shopping around, improving your creditworthiness, and leveraging the unique benefits of the VA loan program, eligible service members and veterans can secure a home loan that truly serves their financial best interests.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.