Understanding the current interest rate for a 15-year mortgage is a critical first step for anyone considering buying a home or refinancing an existing one. While the immediate answer to “what is the current rate?” is a constantly fluctuating figure, a comprehensive understanding requires delving into the economic forces that shape these rates, the distinct advantages and trade-offs of a 15-year term, and the practical steps to secure the most favorable terms for your unique financial situation. This guide aims to provide a professional, insightful, and engaging exploration of 15-year mortgage rates, empowering you with the knowledge to make informed financial decisions.

The 15-year mortgage, often overshadowed by its 30-year counterpart, offers a compelling pathway to accelerated homeownership, significant interest savings, and enhanced financial freedom. However, it demands a higher monthly payment, necessitating a thorough assessment of one’s budget and long-term financial goals. Navigating the world of mortgage rates can feel like a complex endeavor, but by breaking down the key factors and processes, you can approach this significant financial commitment with confidence.

Understanding the Dynamics of Mortgage Rates

Mortgage rates are not static; they are a dynamic reflection of broader economic conditions, monetary policy, and investor sentiment. While the precise rate you receive will be personalized, the baseline rates offered by lenders are heavily influenced by a confluence of macroeconomic factors.

Key Economic Indicators at Play

Several powerful indicators provide the backdrop against which mortgage rates are set:

- Federal Reserve Policy: The Federal Reserve’s actions, particularly its stance on the federal funds rate and its quantitative easing/tightening policies, have a profound indirect impact on mortgage rates. While the federal funds rate directly affects short-term lending between banks, changes in this rate signal the Fed’s inflationary outlook and economic growth expectations. When the Fed raises rates, it generally makes borrowing more expensive across the board, pushing up mortgage rates. Conversely, a dovish stance can lead to lower rates. Furthermore, the Fed’s purchases or sales of Mortgage-Backed Securities (MBS) directly influence their supply and demand, thereby affecting their yields, which are closely tied to mortgage rates.

- Inflation: Inflation is arguably the most significant driver of long-term interest rates, including mortgages. Lenders need to ensure that the interest they earn on a loan will outpace the erosion of purchasing power caused by inflation. When inflation is high or expected to rise, lenders demand higher interest rates to compensate for the reduced future value of the money they will be repaid. Key inflation gauges like the Consumer Price Index (CPI) and the Personal Consumption Expenditures (PCE) index are closely watched.

- Job Market Data: A strong job market, characterized by low unemployment and wage growth, often signals a robust economy and potential inflationary pressures. This can lead to the Fed tightening monetary policy and bond investors demanding higher yields, pushing mortgage rates upwards. Conversely, a weakening job market can suggest economic slowdown, potentially leading to lower rates as the Fed might ease policy and investors seek safer assets like bonds.

- Economic Growth (GDP): A rapidly expanding economy, as measured by Gross Domestic Product (GDP), typically correlates with higher demand for credit and potential inflation, which can drive up interest rates. Slower economic growth or recessionary fears tend to suppress rates.

Global Events and Geopolitical Factors

Beyond domestic economic indicators, global events can send ripples through financial markets, impacting mortgage rates. Geopolitical instability, international trade disputes, pandemics, or significant economic shifts in major global economies can trigger a “flight to safety” among investors, often leading them to purchase U.S. Treasury bonds. Increased demand for bonds can drive down their yields, which, in turn, can exert downward pressure on mortgage rates. Conversely, a stable global environment might see investors move out of safe-haven assets, potentially leading to higher yields and rates.

The Role of Mortgage-Backed Securities (MBS)

Mortgage rates are not directly tied to the prime rate or the federal funds rate. Instead, they are primarily influenced by the bond market, specifically the market for Mortgage-Backed Securities (MBS). MBS are bonds that represent claims to the cash flows from pools of mortgage loans. When you take out a mortgage, your loan is often bundled with thousands of others and sold to investors as an MBS. The yield (return) that investors demand on these securities largely dictates the interest rate that lenders offer. Factors affecting the overall bond market, such as investor appetite for risk, the supply of new bonds, and comparisons to other investment opportunities, all play a crucial role in setting the ultimate price of mortgages.

The Allure of the 15-Year Mortgage: Benefits and Considerations

The 15-year mortgage offers distinct advantages, primarily centered around cost savings and accelerated debt repayment, but it also comes with a notable trade-off.

Significant Interest Savings Over Time

The most compelling argument for a 15-year mortgage is the substantial amount of interest you save over the life of the loan compared to a 30-year mortgage. Because the principal is paid down much faster, and the interest rate itself is typically lower (due to less risk for the lender over a shorter term), the total interest paid can be tens or even hundreds of thousands of dollars less. For example, on a $300,000 loan at 6% over 30 years, you’d pay around $347,517 in interest. The same loan over 15 years at 5.5% would result in approximately $150,563 in interest – a saving of nearly $200,000. These savings translate directly into more wealth in your pocket.

Building Equity Faster

A 15-year mortgage allows you to build equity in your home at a much faster pace. A larger portion of each monthly payment goes towards the principal balance, meaning you own more of your home sooner. Rapid equity accumulation is beneficial for several reasons: it provides a buffer against market downturns, offers greater flexibility for refinancing in the future, and can serve as a significant asset for other financial goals, such as funding education or retirement, should you choose to tap into it.

Achieving Debt-Free Homeownership Sooner

The psychological and financial freedom that comes with paying off your mortgage in 15 years, rather than 30, is immense. Imagine being mortgage-free in your 40s or 50s, allowing you to redirect those significant monthly payments towards other investments, retirement savings, or simply enjoying a lower-stress financial life. This expedited path to homeownership can be a cornerstone of a robust long-term financial plan, particularly for those nearing retirement.

The Trade-off: Higher Monthly Payments

The primary drawback of a 15-year mortgage is the higher monthly payment. Since you are paying off the same loan amount in half the time, your scheduled payments will be significantly larger. It is crucial to run the numbers and ensure that these higher payments are comfortably within your monthly budget, allowing room for emergencies, other financial goals, and discretionary spending without feeling overly stretched. Over-extending yourself can lead to financial stress and potentially put you at risk if unexpected expenses arise.

Less Flexibility in Cash Flow

With higher fixed payments, a 15-year mortgage can offer less flexibility in your monthly cash flow compared to a 30-year loan. While the long-term savings are attractive, ensure you maintain a robust emergency fund and are not sacrificing other important financial goals (like maxing out retirement accounts or saving for a child’s education) to afford the accelerated payments. Financial stability is paramount, and sometimes the flexibility of a lower 30-year payment, with the option to make extra principal payments when possible, might be a more suitable strategy.

How to Find the Most Accurate Current Rates

Pinpointing the “current rate” involves more than a quick Google search; it requires understanding where to look and how to interpret the information. Rates are highly personalized, so what you see advertised might not be the exact rate you qualify for.

Online Lenders and Rate Comparison Sites

Online lenders and dedicated mortgage rate comparison websites are excellent starting points. They offer the convenience of comparing multiple lenders side-by-side, often displaying generalized current rates based on common credit scores and loan-to-value ratios. However, be aware that these advertised rates are often “best-case scenarios” and may not include all fees (like origination fees or discount points) that affect the overall cost (represented by the Annual Percentage Rate or APR). Always look for “live” or personalized quotes that require a soft credit pull to get a more accurate picture.

Traditional Banks and Credit Unions

Don’t overlook traditional brick-and-mortar banks and local credit unions. While they may not always offer the absolute lowest rates, they can provide competitive options, personalized service, and potentially better terms for existing customers. Credit unions, in particular, are member-owned and often prioritize lower fees and more flexible lending criteria. Building a relationship with a local institution can also be beneficial for future financial needs.

Mortgage Brokers

A mortgage broker acts as an intermediary between you and multiple lenders. They have access to a wide network of wholesale lenders and can shop around on your behalf to find the best rates and terms. Brokers can be particularly helpful for borrowers with unique financial situations or those who prefer a guided experience. They earn a commission, either from the lender or the borrower, so it’s important to understand their fee structure upfront.

Factors Influencing Your Individual Rate

The rate you ultimately qualify for is a highly individualized figure, determined by several key personal financial metrics:

- Credit Score: A strong credit score (generally 740 or higher) signals to lenders that you are a reliable borrower, leading to the best available rates. Lower scores indicate higher risk and will result in higher interest rates.

- Debt-to-Income (DTI) Ratio: This ratio compares your total monthly debt payments (including the proposed mortgage payment) to your gross monthly income. Lenders typically prefer a DTI below 43% (though some programs allow higher) as a sign that you can comfortably manage your debts.

- Down Payment: A larger down payment (e.g., 20% or more) reduces the lender’s risk, often leading to a lower interest rate and eliminating the need for private mortgage insurance (PMI).

- Loan-to-Value (LTV) Ratio: This is the loan amount divided by the home’s appraised value. A lower LTV (meaning a higher down payment) generally results in better rates.

- Property Type and Location: Certain property types (e.g., multi-family homes, investment properties) or specific geographic locations might carry slightly different risk profiles and thus affect rates.

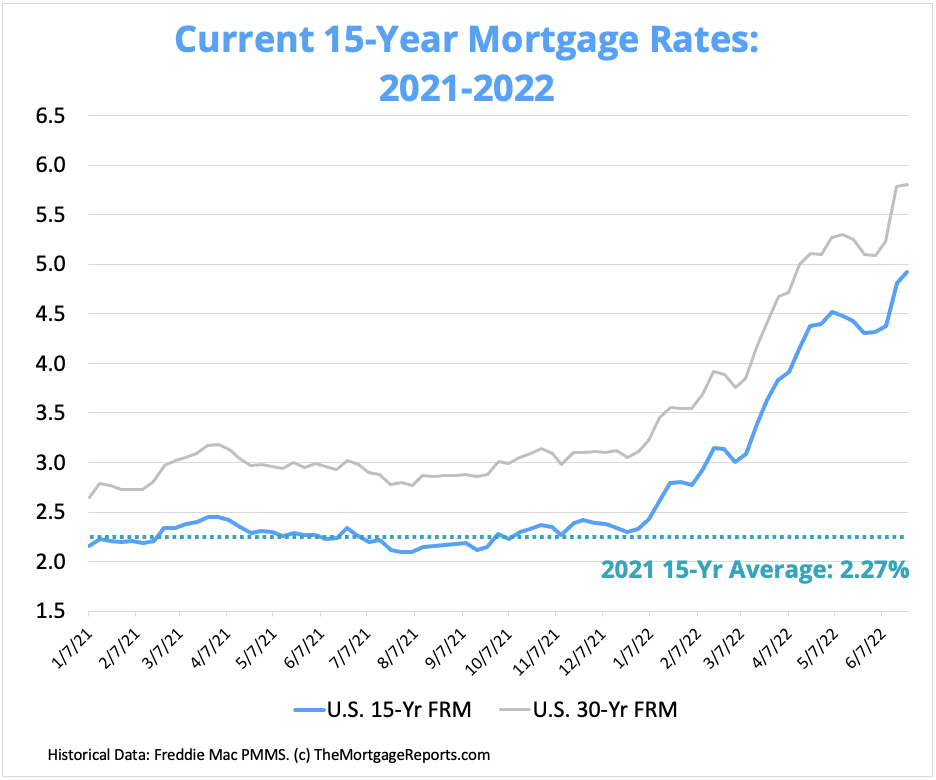

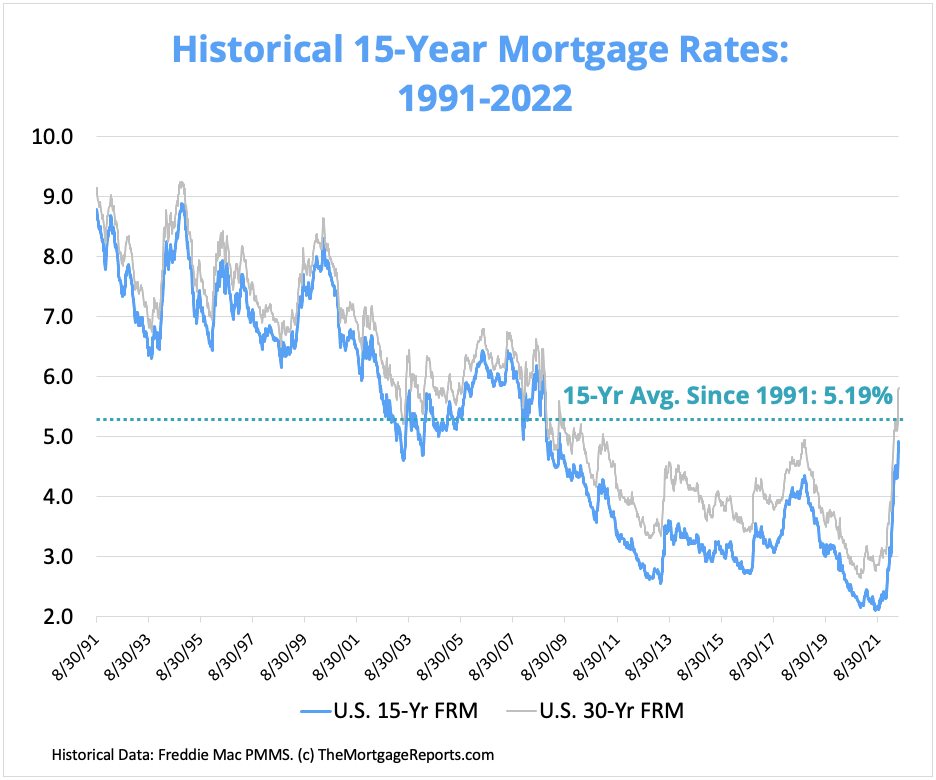

- Loan Term and Type: As discussed, 15-year mortgages typically have lower rates than 30-year fixed mortgages. Adjustable-Rate Mortgages (ARMs) often start with lower rates than fixed-rate options.

- Points: You can often “buy down” your interest rate by paying discount points at closing. Each point typically costs 1% of the loan amount and can reduce your interest rate, which may be beneficial if you plan to stay in the home for a long time.

Navigating the Application Process and Securing Your Rate

Once you’ve researched rates and understood the factors at play, the next step is the application process itself. This stage requires careful preparation and attention to detail.

Preparing Your Financial Documents

Lenders require a comprehensive set of documents to verify your financial standing. This typically includes:

- Income Verification: Pay stubs (last 30-60 days), W-2 forms (last two years), and tax returns (last two years for self-employed individuals).

- Asset Statements: Bank statements (last two months) and investment account statements to verify funds for your down payment and closing costs, as well as reserves.

- Credit Reports: Lenders will pull your credit reports from the three major bureaus. It’s wise to review your own reports beforehand for any inaccuracies.

- Employment History: Details of your current and previous employers.

- Other Debts: Statements for credit cards, auto loans, student loans, etc.

Being organized and providing complete, accurate documentation promptly can significantly streamline the approval process.

Understanding Loan Estimates and Closing Costs

When you apply for a mortgage, lenders are required to provide you with a Loan Estimate (LE) within three business days. This standardized form details your estimated interest rate, monthly payment, and all closing costs. Carefully review the LE, paying attention to:

- Interest Rate vs. APR: The interest rate is what you pay on the principal loan amount. The Annual Percentage Rate (APR) is a broader measure of the total cost of the loan, including the interest rate and most closing costs (like origination fees, discount points, and private mortgage insurance). The APR often gives a more accurate comparison between different loan offers.

- Itemized Closing Costs: These are fees paid at the close of the loan, which can range from 2% to 5% of the loan amount. They include lender fees (origination, underwriting), third-party fees (appraisal, title insurance, recording fees), and prepaid items (property taxes, homeowner’s insurance). Understand what each fee is for and compare them across different lenders.

The Importance of a Rate Lock

Mortgage rates can change daily, even hourly. To protect yourself from a sudden rate hike between application and closing, you can “lock” your interest rate. A rate lock guarantees that your interest rate will not change for a specified period (typically 30, 45, or 60 days) as long as you close within that timeframe. Discuss the rate lock option with your lender and understand any associated fees or conditions, such as “float down” options if rates drop significantly after your lock. Timing your rate lock strategically is a crucial decision, often best made after your loan has moved through the initial underwriting stages.

Avoiding Common Pitfalls

The mortgage process can be complex, and certain missteps can jeopardize your application or cost you money:

- Not Shopping Around: Failing to compare offers from multiple lenders is one of the biggest mistakes. Even a quarter-point difference in interest can save you tens of thousands over the life of a 15-year loan.

- Ignoring Pre-Approval: Getting pre-approved for a mortgage before house hunting gives you a clear budget, demonstrates to sellers that you’re a serious buyer, and highlights any potential issues with your application early on.

- Making Large Financial Changes: Avoid taking on new debt (e.g., buying a car, opening new credit cards), making large cash deposits, changing jobs, or closing credit accounts between pre-approval and closing. These actions can alter your credit profile or DTI and potentially derail your loan approval.

- Focusing Only on Interest Rate: While crucial, the interest rate isn’t the only factor. Consider the APR, closing costs, lender reputation, and quality of service when choosing a mortgage.

In conclusion, understanding “what is the current rate for a 15-year mortgage” is a journey that begins with recognizing the intricate economic forces that drive rates, appreciating the distinct advantages and considerations of this accelerated loan term, and mastering the practicalities of securing the best possible rate. By being proactive, informed, and diligent throughout the process, you can leverage the power of a 15-year mortgage to achieve your homeownership dreams and build long-term financial stability. Always consult with a qualified financial advisor or mortgage professional to tailor advice to your specific circumstances.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.