For the vast majority of aspiring homeowners and real estate investors, the 30-year fixed-rate mortgage represents the cornerstone of the American Dream. It is more than just a loan; it is a long-term financial instrument that provides stability in an otherwise volatile economy. However, determining the “current” rate is a moving target, influenced by a complex interplay of global economic shifts, central bank policies, and individual financial health. Understanding the nuances behind these rates is essential for making informed decisions that will impact your net worth for decades to come.

The Anatomy of the 30-Year Fixed-Rate Mortgage

The 30-year fixed-rate mortgage is the gold standard of home financing because of its predictability. Unlike adjustable-rate mortgages (ARMs), where the interest rate can fluctuate after an initial period, the fixed-rate option locks in an interest rate for the entire 360-month duration of the loan.

The Mechanics of Amortization

When you secure a 30-year fixed mortgage, your monthly payment remains constant, but the composition of that payment changes over time. In the early years of the loan, a significant portion of your payment is directed toward interest. As the loan matures, a larger share is applied to the principal balance. This process, known as amortization, ensures that the loan is paid in full by the end of the term. For the borrower, this creates a “forced savings” mechanism, gradually building equity in a tangible asset.

Why Stability Matters in Personal Finance

Financial planning thrives on predictability. By locking in a rate, homeowners protect themselves against future inflation. If the cost of living rises and the value of the dollar decreases, your mortgage payment—fixed in today’s dollars—effectively becomes “cheaper” over time. This hedge against inflation is a primary reason why many financial advisors recommend the 30-year fixed-rate over shorter-term or variable options, particularly when rates are historically moderate.

Economic Drivers Shaping Today’s Interest Rate Environment

The interest rate you see quoted by lenders is not an arbitrary number. It is a reflection of the broader economic climate. While the 30-year fixed rate is not directly set by the government, it is heavily influenced by several macroeconomic factors.

The Role of the Federal Reserve and Inflation

The Federal Reserve (the Fed) manages the federal funds rate to control inflation and maximize employment. When inflation is high, the Fed typically raises rates to cool the economy. While this does not directly dictate mortgage rates, it increases the cost of borrowing for banks, which then passes those costs on to consumers. If you are tracking current mortgage rates, you must keep a close eye on the Consumer Price Index (CPI) and the Fed’s subsequent policy meetings.

The Correlation with the 10-Year Treasury Yield

Interestingly, 30-year mortgage rates track more closely with the 10-year Treasury yield than they do with the Fed’s short-term rates. Investors view both 10-year Treasuries and 30-year mortgages as long-term fixed-income investments. When investors are confident in the economy, they demand higher yields for Treasuries, which pushes mortgage rates upward. Conversely, in times of economic uncertainty, investors flock to the safety of bonds, driving yields—and mortgage rates—down.

Global Market Volatility and Risk Premiums

Mortgage rates also include a “risk premium.” Lenders must account for the possibility that a borrower might default or that the loan might be paid off early (prepayment risk). In times of global instability or domestic economic recession, this risk premium expands, meaning even if benchmark yields are low, the mortgage rate offered to consumers may remain high to compensate lenders for the perceived risk.

Navigating the Cost of Capital: Beyond the Headline Rate

When asking “what is the current mortgage rate,” many consumers make the mistake of looking only at the interest rate. In reality, the true cost of borrowing is more comprehensive and requires an understanding of several financial layers.

Interest Rate vs. Annual Percentage Rate (APR)

The interest rate is the percentage charged on the principal loan amount. The Annual Percentage Rate (APR), however, is a broader measure of the cost of the loan. It includes the interest rate plus other costs such as broker fees, points, and some closing costs. When comparing offers from different financial institutions, the APR is the more accurate tool for evaluating which loan is actually more affordable over the long term.

The Strategic Use of Discount Points

In today’s market, many borrowers choose to “buy down” their interest rate using discount points. One point typically costs 1% of the total loan amount and reduces the interest rate by a predetermined increment (often 0.25%). This is a classic capital allocation decision: you pay more upfront to reduce your monthly obligations and total interest paid over 30 years. This strategy is highly effective if you plan to stay in the home for a significant period—usually seven years or more—to reach the “break-even” point.

The Impact of Private Mortgage Insurance (PMI)

For many, the current mortgage rate is secondary to the total monthly outflow, which may include Private Mortgage Insurance. If a borrower provides a down payment of less than 20%, lenders require PMI to protect their investment. While PMI doesn’t change your interest rate, it increases your effective borrowing cost. As you build equity and reach that 20% threshold, canceling PMI is one of the fastest ways to improve your monthly cash flow without needing to refinance.

Strategies to Optimize Your Financial Profile for Lower Rates

The “current rate” quoted in news headlines is typically reserved for “prime” borrowers—those with impeccable financial credentials. If your goal is to secure a rate at or below the market average, you must treat your financial profile as a resume for lenders.

Credit Score Optimization

Your credit score is the single most important factor in determining the rate a lender offers you. A score above 760 generally qualifies you for the best available rates. Even a 20-point difference in your credit score can result in a 0.25% to 0.50% difference in your interest rate. Over a 30-year period, that seemingly small fraction can translate into tens of thousands of dollars in interest savings. Prioritizing debt reduction and ensuring timely payments in the months leading up to a mortgage application is a high-ROI activity.

Debt-to-Income (DTI) and Loan-to-Value (LTV) Ratios

Lenders evaluate your ability to manage monthly payments through the DTI ratio. Most conventional lenders prefer a DTI below 36%, though some programs allow for higher. Similarly, the Loan-to-Value (LTV) ratio—the size of the loan relative to the home’s value—affects your risk profile. A larger down payment reduces the LTV, signals lower risk to the lender, and can often unlock “tier-one” pricing for your mortgage rate.

Shopping for Lenders and Rate Locks

Mortgage rates can vary significantly between big banks, credit unions, and online mortgage brokers. It is financially prudent to obtain at least three different Loan Estimates. Once you find a competitive rate that fits your budget, considering a “rate lock” is essential. Because market rates can change daily (or even hourly), a rate lock protects you from increases while your loan is being processed, which can take anywhere from 30 to 60 days.

Long-Term Financial Implications of Current Rate Trends

Deciding whether to lock in a 30-year fixed rate requires an analysis of the current market cycle versus your personal investment horizon.

“Marry the House, Date the Rate”

This common real estate adage suggests that if you find the right property, you should purchase it even if current rates are higher than you’d like. The logic is that you can always refinance your mortgage if rates drop in the future, but you cannot change the purchase price of the home. However, this strategy requires a financial cushion; you must be able to afford the current rate comfortably today, rather than banking on a speculative future refinance that may not materialize if economic conditions shift.

The Opportunity Cost of Homeownership

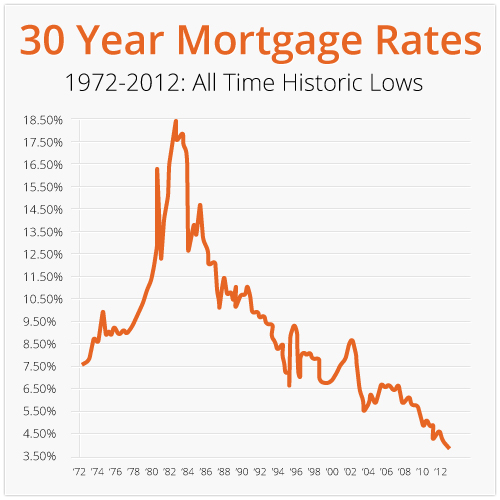

From a personal finance perspective, a mortgage is a tool for leveraging capital. While a 6% or 7% interest rate might feel high compared to the historic lows of 2020-2021, it is important to view this in the context of other investment opportunities. If the historical return of the stock market is roughly 10%, borrowing at 6.5% to own an appreciating asset (real estate) while keeping your other capital invested in the market can still be a sound wealth-building strategy.

Conclusion: Making the Move

The current mortgage rate for a 30-year fixed loan is a reflection of a complex economic machine. While you cannot control the Federal Reserve or global inflation, you can control your financial readiness. By optimizing your credit, understanding the difference between interest rates and APR, and viewing homeownership as a long-term hedge against inflation, you can navigate today’s lending environment with confidence. Ultimately, the best rate is the one that allows you to secure a valuable asset while maintaining a healthy, diversified financial portfolio.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.