Understanding the average home interest rate is far more than just knowing a number; it’s a critical insight into the health of the housing market, the broader economy, and, most importantly, your personal financial future. For most individuals, purchasing a home represents the single largest financial transaction of their lives, and the interest rate attached to their mortgage can dramatically alter the cost of that investment over decades. A seemingly small fluctuation in the average rate can translate into tens of thousands of dollars saved or spent over the life of a loan, directly impacting affordability, monthly budgets, and overall wealth accumulation.

This article delves into the intricate world of home interest rates, dissecting what they are, how they are influenced, and their profound implications for homebuyers, homeowners, and the economy at large. We will explore the various factors that cause these rates to rise and fall, how the “average” is actually determined, and practical strategies you can employ to secure the most favorable terms for your unique financial situation. Navigating the mortgage landscape requires more than just searching for the lowest rate; it demands a comprehensive understanding of the forces at play and a proactive approach to financial planning.

Understanding the Dynamics of Home Interest Rates

Home interest rates are not static figures but rather dynamic indicators influenced by a complex interplay of economic forces, central bank policies, and market sentiment. Grasping these underlying mechanisms is crucial for anyone looking to enter the housing market or manage an existing mortgage.

Key Factors Influencing Rates

Several powerful factors continually shape and reshape the average home interest rate, making it a moving target for prospective borrowers.

- Federal Funds Rate and Federal Reserve Policy: Perhaps the most significant influence comes from the U.S. central bank, the Federal Reserve. While the Fed does not directly set mortgage rates, its actions profoundly impact them. The Federal Funds Rate, the target rate for overnight lending between banks, serves as a benchmark for other interest rates across the economy. When the Fed raises this rate, it typically signals a tightening of monetary policy, making borrowing more expensive for banks, which then pass those increased costs on to consumers through higher interest rates on various loans, including mortgages. Conversely, a reduction in the Federal Funds Rate can lead to lower borrowing costs. The Fed’s pronouncements on inflation, employment, and economic growth are closely watched by markets for clues about future rate movements.

- Inflation: Inflation, the rate at which the general level of prices for goods and services is rising, has a direct correlation with interest rates. Lenders charge interest to compensate for the risk of lending money and to ensure their return on investment isn’t eroded by future inflation. If inflation is expected to rise, lenders will demand higher interest rates to preserve the purchasing power of the money they will be repaid. Conversely, low or stable inflation can contribute to lower rates.

- Economic Growth and Employment: A robust economy, characterized by strong GDP growth and low unemployment, often leads to higher interest rates. Lenders perceive a healthier economy as an environment where there is greater demand for loans and where borrowers are more likely to repay their debts, allowing them to charge more. However, strong economic growth can also spark inflation concerns, prompting the Fed to raise rates to cool down an overheating economy. Conversely, during economic downturns, central banks might lower rates to stimulate borrowing and investment.

- The Bond Market (Specifically the 10-Year Treasury Yield): Mortgage rates, particularly for 30-year fixed-rate mortgages, are closely tied to the yields on long-term U.S. Treasury bonds, especially the 10-year Treasury note. Mortgage-backed securities (MBS), which are bundles of mortgages sold to investors, compete with Treasury bonds for investment dollars. When the yield on the 10-year Treasury rises, it makes Treasuries more attractive to investors, and mortgage-backed securities must offer higher yields (and thus higher interest rates) to compete. This relationship makes the 10-year Treasury yield a critical barometer for future mortgage rate movements.

- Market Demand and Supply for Mortgages: Like any market, the supply and demand for mortgage credit also play a role. If there’s high demand for homes and mortgages, but a limited supply of lenders or capital, rates may rise. Conversely, an abundance of available capital and fewer borrowers could push rates down as lenders compete for business.

The Difference Between Fixed and Adjustable Rates

When securing a home loan, borrowers typically encounter two primary types of interest rates, each with distinct characteristics and implications.

- Fixed-Rate Mortgages (FRMs): A fixed-rate mortgage is characterized by an interest rate that remains constant throughout the entire life of the loan. This provides unparalleled stability and predictability in monthly payments, making budgeting straightforward for homeowners. Popular terms include 15-year and 30-year fixed mortgages. Borrowers opting for a fixed rate are protected from future rate hikes but also miss out if rates fall significantly, unless they choose to refinance. This option is generally preferred by those seeking long-term stability and who believe current rates are favorable or are likely to rise in the future.

- Adjustable-Rate Mortgages (ARMs): In contrast, an adjustable-rate mortgage features an interest rate that is fixed for an initial period (e.g., 3, 5, 7, or 10 years) and then adjusts periodically for the remainder of the loan term. The initial fixed period often comes with a lower interest rate compared to a traditional fixed-rate mortgage, making it an attractive option for borrowers with specific financial circumstances. After the initial period, the rate typically adjusts annually based on a predetermined index (like the Secured Overnight Financing Rate – SOFR) plus a margin set by the lender. ARMs carry the risk of increased monthly payments if interest rates rise, but they can also lead to lower payments if rates fall. They are often considered by borrowers who plan to sell or refinance before the fixed period ends, or those who anticipate their income will increase significantly in the future, allowing them to absorb potential rate increases.

How Average Rates Are Calculated and Reported

When financial news outlets or real estate websites refer to the “average home interest rate,” they are typically referencing specific surveys or indices that provide a snapshot of prevailing market conditions. Understanding how these averages are derived helps in interpreting the data accurately.

Sources of Rate Data

Several reputable organizations regularly collect and disseminate mortgage rate data, offering valuable benchmarks for consumers and industry professionals.

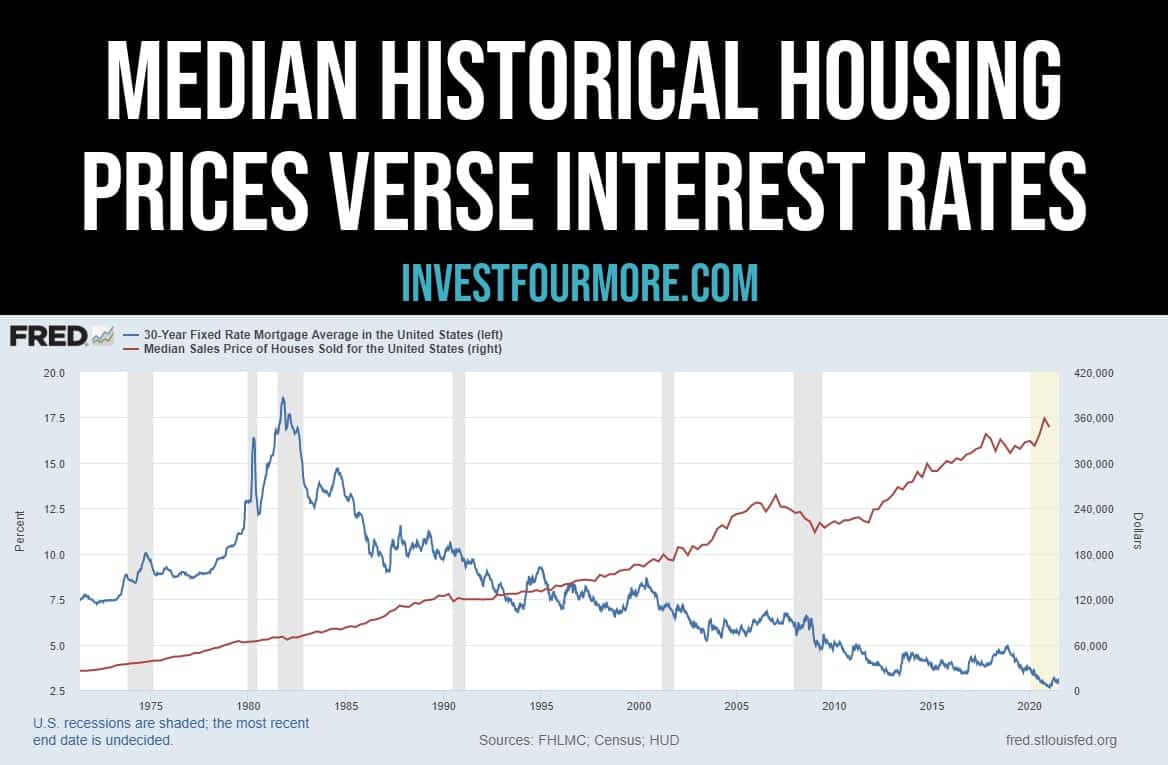

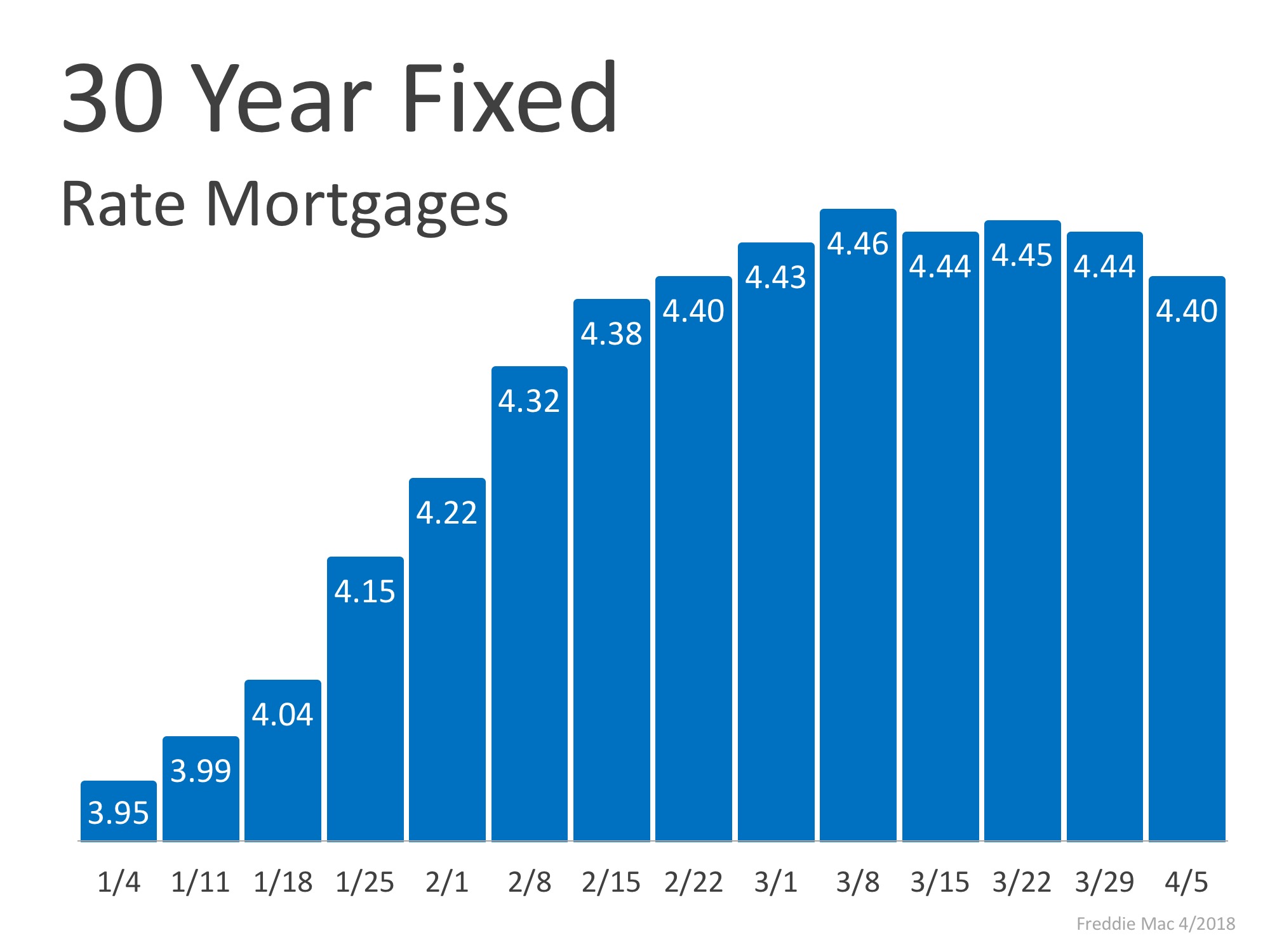

- Freddie Mac Primary Mortgage Market Survey (PMMS): This is perhaps the most widely cited source for average mortgage rates in the United States. Since 1971, Freddie Mac has surveyed thousands of lenders across the country each week, collecting data on their conventional 30-year fixed-rate, 15-year fixed-rate, and 5/1 adjustable-rate mortgage offerings. The PMMS reports national average rates, points, and fees for these loan types, providing a consistent historical series that serves as a benchmark for the industry. It’s important to note that the PMMS is a survey of offered rates, not necessarily the rates at which all loans close, and it focuses on borrowers with excellent credit.

- Mortgage Bankers Association (MBA): The MBA also conducts weekly surveys of mortgage applications, including data on rates, loan types, and volumes. While not as frequently quoted for “average rates” as Freddie Mac, the MBA’s data offers insights into market activity and trends from a different perspective.

- Individual Lender Data and Financial News Aggregators: Many major banks, credit unions, and online lenders publish their own current rates, and financial news sites often aggregate data from various sources to provide a real-time, albeit less formally averaged, view of the market. These can be useful for comparing specific offerings but might not reflect a true national average.

Nuances in “Average” Rates

It’s crucial to understand that the reported “average” interest rate is a generalized figure and may not precisely reflect the rate an individual borrower will receive. Many factors specific to the loan and the borrower can influence the final rate.

- Depends on Loan Type: The “average” often refers to a 30-year fixed-rate conventional mortgage. Rates for other loan types, such as 15-year fixed, FHA, VA, or USDA loans, will have their own distinct averages and can differ significantly due to varying risk profiles and government backing.

- Depends on Loan Term: Shorter-term mortgages, like a 15-year fixed, typically carry lower interest rates than longer-term options, such as a 30-year fixed. This is because lenders perceive less risk over a shorter repayment period.

- Borrower-Specific Factors: Your individual financial profile is paramount.

- Credit Score: A higher credit score (generally 740 and above) signals lower risk to lenders, often resulting in access to the lowest available rates. Lower scores will result in higher rates to compensate lenders for increased risk.

- Down Payment: A larger down payment reduces the loan-to-value (LTV) ratio, meaning the borrower has more equity upfront. This also reduces lender risk and can lead to a better interest rate.

- Debt-to-Income (DTI) Ratio: Lenders assess your DTI to determine your ability to manage monthly payments. A lower DTI (ideally below 43%) indicates less financial strain and can qualify you for better rates.

- Points and Fees: The quoted “average” rate often assumes a certain number of “points.” A mortgage point is a fee equal to 1% of the loan amount, paid upfront to the lender. Borrowers can sometimes “buy down” their interest rate by paying discount points, effectively getting a lower rate in exchange for a higher upfront cost. Conversely, a higher interest rate might come with fewer or no points. The average rate reported typically includes points, so borrowers should always compare both the rate and the associated fees.

The Impact of Interest Rates on Your Homeownership Journey

Interest rates are not just numbers; they are powerful economic levers that dictate affordability, shape market dynamics, and determine the long-term financial burden of homeownership. Their fluctuations can have far-reaching consequences for both prospective and current homeowners.

Affordability and Monthly Payments

The most immediate and tangible impact of interest rates is on the affordability of a home and the size of your monthly mortgage payment. Even small changes in the interest rate can lead to significant differences over the life of a 30-year loan.

- Direct Impact on Monthly Costs: A higher interest rate means a larger portion of your monthly payment goes towards interest, rather than principal. This directly increases your monthly outlay for the same loan amount. For example, on a $300,000, 30-year fixed mortgage, a rate increase from 5% to 6% can add over $180 to your monthly payment, totaling more than $65,000 over the life of the loan. This additional cost can strain budgets, making homeownership less accessible.

- Impact on Purchasing Power: Rising interest rates reduce a borrower’s purchasing power. With a higher rate, the maximum loan amount you can qualify for, while maintaining an affordable monthly payment, decreases. This means that a borrower who could afford a $400,000 home at 4% might only be able to afford a $350,000 home at 6%, effectively pricing them out of certain segments of the market or forcing them to compromise on their desired home features.

Refinancing Opportunities

For existing homeowners, changes in the average interest rate present crucial opportunities, most notably through refinancing.

- Reducing Monthly Payments: When interest rates drop significantly below your current mortgage rate, refinancing can be an attractive option. By securing a new loan at a lower rate, you can reduce your monthly mortgage payment, freeing up cash flow for other financial goals or savings.

- Accessing Home Equity (Cash-Out Refinance): A cash-out refinance allows homeowners to take out a new, larger mortgage than their current outstanding balance, receiving the difference in cash. This is often done when rates are low, allowing homeowners to leverage their home equity for purposes such as home renovations, debt consolidation, or other large expenses, while potentially securing a lower overall interest rate on the entire new loan.

- Changing Loan Terms: Refinancing also provides an opportunity to change the terms of your loan. You might convert an adjustable-rate mortgage (ARM) to a fixed-rate mortgage to lock in stability during a period of rising rates, or shorten your loan term (e.g., from 30 years to 15 years) to pay off your home faster, often at a lower interest rate, though with higher monthly payments.

Market Implications for Buyers and Sellers

Beyond individual finances, interest rates act as a significant market driver, influencing the overall health and activity of the housing market for both buyers and sellers.

- Higher Rates Cool the Market: When interest rates rise, the cost of borrowing increases, leading to a decrease in buyer demand. Fewer buyers can afford homes, leading to a slowdown in sales, an increase in housing inventory, and potentially a moderation or even decrease in home prices as sellers compete for a smaller pool of qualified buyers. This can shift the market from a seller’s market to a buyer’s market.

- Lower Rates Heat Up the Market: Conversely, falling interest rates stimulate demand. Homes become more affordable, attracting a larger pool of buyers. This increased competition can lead to bidding wars, rapid sales, and upward pressure on home prices, creating a seller’s market. Lower rates also encourage current homeowners to consider selling and moving up, as their next mortgage might be more affordable.

Strategies for Securing the Best Home Interest Rate

While external economic forces dictate the general direction of average interest rates, individual borrowers are not entirely powerless. Several personal financial strategies can significantly improve your chances of securing a rate better than the prevailing average.

Improving Your Financial Profile

Lenders assess risk, and a stronger financial profile directly translates to a lower perceived risk, often resulting in more favorable interest rates.

- Credit Score: Your credit score is a primary determinant of your interest rate. Lenders use it to gauge your creditworthiness and your history of debt repayment. A FICO score of 740 or higher is generally considered excellent and will qualify you for the most competitive rates. Focus on paying bills on time, keeping credit utilization low, and correcting any errors on your credit report well in advance of applying for a mortgage.

- Down Payment: A larger down payment reduces the loan-to-value (LTV) ratio, which is the amount of the loan compared to the home’s value. A lower LTV means less risk for the lender. Putting down 20% or more typically helps you avoid private mortgage insurance (PMI) and often qualifies you for a better interest rate. Even if you can’t hit 20%, a larger down payment than the minimum required is always beneficial.

- Debt-to-Income (DTI) Ratio: Your DTI ratio is a measure of your monthly debt payments compared to your gross monthly income. Lenders prefer a lower DTI, ideally below 43%, as it indicates you have sufficient income to manage your mortgage payments alongside other financial obligations. Reduce non-essential debt, such as credit card balances or car loans, before applying for a mortgage.

Shopping Around and Negotiation

Never settle for the first offer you receive. The mortgage market is competitive, and comparing offers can save you a substantial amount of money.

- Get Quotes from Multiple Lenders: Contact at least three to five different types of lenders: large national banks, local credit unions, and mortgage brokers. Each may have different pricing models, loan products, and fee structures. Mortgage brokers, in particular, can shop your application among multiple wholesale lenders to find the best deal.

- Understand Loan Estimates and Compare Fees: Lenders are legally required to provide a standardized “Loan Estimate” within three business days of application. This document details the interest rate, estimated monthly payments, and closing costs. Carefully compare the annual percentage rate (APR), which reflects the true annual cost of the loan including some fees, as well as specific fees like origination fees, appraisal costs, and title insurance. Don’t just look at the rate; look at the total cost.

- Negotiation: While interest rates are largely market-driven, there might be some room for negotiation, especially on lender fees or if you have a strong financial profile. Use competing Loan Estimates to leverage a better deal with your preferred lender.

Locking In Your Rate

Once you’ve found a favorable interest rate, you’ll need to decide whether to “lock” it in.

- When and Why to Lock a Rate: A rate lock guarantees that your interest rate will not change between the time you apply for a loan and the day you close, even if market rates increase. This protects you from adverse rate movements. You typically lock a rate when you feel confident that you’ve found a good deal and that rates might start to rise. Be aware that most rate locks come with a specific timeframe (e.g., 30, 45, or 60 days).

- Lock Period Considerations: Choose a lock period that comfortably extends beyond your anticipated closing date. A longer lock period typically comes with a slightly higher interest rate or an additional fee, as it represents more risk for the lender. If your lock expires before closing, you might be subject to the current market rates or pay a fee to extend the lock.

Conclusion

The “average home interest rate” is a dynamic and multifaceted figure that profoundly influences the financial landscape of homeownership. Far from being a mere statistic, it serves as a powerful indicator of economic health, central bank policy, and market sentiment, with direct implications for a borrower’s monthly payments, overall affordability, and long-term wealth building.

Understanding the factors that drive these rates—from Federal Reserve actions and inflation to the nuances of the bond market and individual creditworthiness—is not just an academic exercise; it is an essential component of prudent personal finance. Whether you are a first-time homebuyer embarking on your property journey, an existing homeowner contemplating a refinance, or an investor tracking market trends, a comprehensive grasp of interest rate dynamics empowers you to make informed decisions.

By proactively managing your financial profile, diligently shopping for the best loan terms, and strategically locking in your rate, you can navigate the complexities of the mortgage market with greater confidence and secure a home loan that aligns with your financial goals. Staying informed, comparing offers, and understanding the long-term impact of your choices are paramount in harnessing the power of interest rates to your financial advantage. In the ever-evolving world of money, an educated borrower is truly an empowered borrower.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.