The concept of an “ecological footprint” is often relegated to the realm of environmental science, yet for the modern American, it is fundamentally a matter of personal and macro-level finance. An ecological footprint measures the amount of biologically productive land and sea area an individual, a city, or a country requires to produce the resources they consume and to absorb the waste they generate. For the average American, this footprint is approximately 8.0 global hectares (gha) per person—nearly four times the global average.

From a financial perspective, this massive footprint represents more than just a biological deficit; it reflects a specific pattern of capital allocation, consumer behavior, and long-term economic risk. Understanding the average American’s ecological footprint is essential for anyone looking to optimize their personal finances, invest sustainably, or understand the future of the global marketplace.

The Financial Mechanics of the Ecological Footprint

The high ecological footprint of the average American is a direct reflection of a consumer-driven economy where convenience often takes precedence over cost-efficiency. When we break down the footprint into financial terms, we see that it is built on three pillars: high-energy housing, intensive transportation, and resource-heavy dietary habits. Each of these carries a significant price tag that impacts net worth over time.

Resource Consumption as an Expense Item

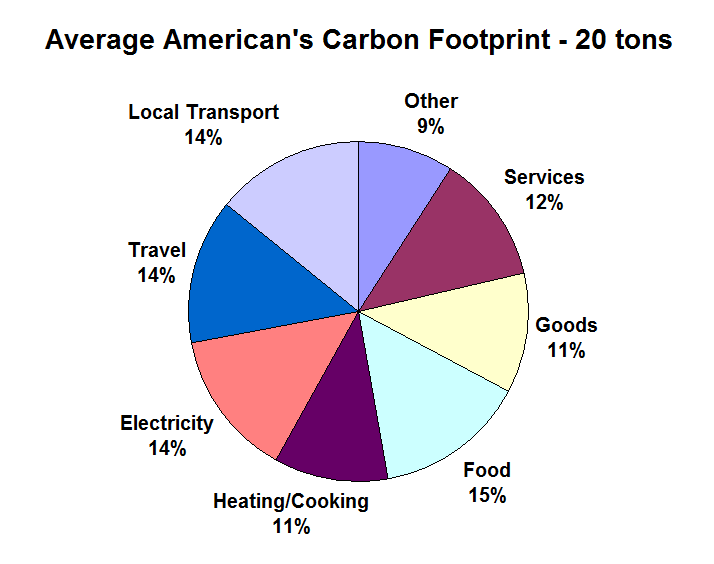

The average American’s footprint is driven largely by carbon emissions, which account for over 60% of the total impact. In financial terms, carbon is an inefficiency. When a household has a high carbon footprint, it typically indicates high monthly utility bills, frequent expenditures on fuel, and a reliance on products with complex, expensive supply chains. By analyzing the footprint as an expense report, it becomes clear that “living large” ecologically often equates to “leaking cash” financially. High consumption isn’t just an environmental burden; it is a recurring liability on a personal balance sheet that prevents the accumulation of investable capital.

The Luxury Tax of High-Carbon Living

Many of the habits that inflate the American ecological footprint function as a “luxury tax” that consumers pay voluntarily. For example, the preference for large, single-family suburban homes requires significant capital for heating, cooling, and maintenance. Similarly, the American reliance on personal vehicles rather than public transit or micromobility represents a massive depreciation trap. Between insurance, fuel, maintenance, and the rapid loss of asset value, the “footprint” of a car is one of the greatest hurdles to achieving financial independence. In this light, reducing one’s ecological footprint is not merely an act of altruism; it is a strategic move to eliminate high-cost, low-yield expenditures.

Sustainable Wealth: The Intersection of Personal Finance and Ecology

As the global economy shifts toward sustainability, the relationship between an individual’s footprint and their financial health is becoming more pronounced. Savvy investors and homeowners are beginning to realize that a low ecological footprint is often synonymous with high financial resilience.

ESG and the Shift in Capital Markets

On a broader scale, the financial world has embraced ESG (Environmental, Social, and Governance) criteria as a standard for assessing risk and potential return. Just as corporations are being scrutinized for their carbon output, individual “financial footprints” are being reshaped by the availability of green financial products. From green bonds to sustainable index funds, the flow of capital is increasingly favoring entities—and by extension, individuals—who minimize resource waste. For the average American, aligning their personal “portfolio” (including their home and lifestyle choices) with these trends is a way to hedge against future carbon taxes and rising resource costs.

Green Real Estate: Efficiency as an Asset Class

For most Americans, their home is their largest financial asset. The ecological footprint of a home is determined by its energy efficiency, size, and location. Homes with a smaller footprint—those equipped with solar panels, high-grade insulation, and smart energy management systems—are increasingly commanding higher market premiums. These “green” features serve a dual purpose: they reduce the ecological footprint and lower the internal rate of return (IRR) required to maintain the property. Investing in a low-footprint home is no longer just a “green” choice; it is a capital improvement that enhances the asset’s resale value while providing an immediate boost to monthly cash flow through utility savings.

Strategic Frugality: Reducing Impact to Accelerate Financial Independence

The movement toward Financial Independence, Retire Early (FIRE) has long recognized that a lower ecological footprint is a secret weapon for wealth building. By adopting a “minimalist” or “essentialist” approach to consumption, individuals can drastically reduce their ecological impact while simultaneously increasing their savings rate.

Transportation and Housing: The Double-Bottom Line

In the world of personal finance, housing and transportation usually account for over 50% of an average household’s budget. Coincidentally, these are also the two largest contributors to the American ecological footprint. By optimizing these two areas—such as living in a walkable urban center or opting for a modest, energy-efficient dwelling—an individual can achieve a “double-bottom line.” They reduce their land and carbon requirements (the footprint) while freeing up thousands of dollars per month that can be diverted into compound-interest-bearing accounts. This synergy proves that environmental stewardship and aggressive wealth-building are not mutually exclusive; they are, in fact, complementary strategies.

Circular Economy Habits and Their Impact on Cash Flow

The “linear” economy—take, make, dispose—is the primary driver of the high American footprint. Shifting toward a “circular” mindset involves repairing, repurposing, and buying high-quality goods that last. Financially, this reduces the “cost per use” of every item owned. The average American spends a significant portion of their income on “fast” goods—fast fashion, fast food, and disposable electronics. By rejecting this model in favor of a low-footprint, circular approach, consumers avoid the “replacement cycle” that drains wealth. Buying a $100 pair of boots that lasts ten years is infinitely better for both the planet and the bank account than buying five $40 pairs that end up in a landfill within the same timeframe.

The Macroeconomic Impact of the American Footprint

Beyond personal finance, the average American’s ecological footprint has profound implications for the national economy and future fiscal policy. As resources become scarcer and more expensive to extract, the cost of maintaining a high-footprint lifestyle will inevitably rise.

The Rising Cost of Externality Internalization

For decades, the true cost of a high ecological footprint has been “externalized”—meaning the individual consumer didn’t pay for the environmental damage caused by their consumption. However, this is changing. Through carbon credits, plastic taxes, and increased waste management fees, these costs are being “internalized.” For the average American, this means that high-footprint behaviors will become increasingly expensive. From a business finance perspective, this is a clear signal to pivot. Those who proactively lower their footprint now are effectively “shorting” the rising cost of carbon, positioning themselves to be more competitive in a future where resource consumption is heavily taxed.

Economic Stability and Resource Security

On a national level, a high ecological footprint per capita places a strain on infrastructure and resource security. An economy that requires five “Earths” to sustain its lifestyle is inherently volatile. As a result, we are seeing a shift in government subsidies and incentives toward renewable energy and conservation. From a money management perspective, staying ahead of these policy shifts is crucial. Taking advantage of tax credits for electric vehicles or energy-efficient home upgrades allows Americans to use “other people’s money” (government incentives) to reduce their footprint and increase their long-term solvency.

Conclusion: The Path to Ecological and Financial Solvency

The average American’s ecological footprint of 8.0 gha is a stark reminder of the imbalance between our current consumption levels and the planet’s regenerative capacity. However, when viewed through the lens of money and finance, this footprint is also a roadmap for optimization.

Reducing your ecological footprint is one of the most effective ways to lower your cost of living, increase your investment capital, and protect your assets from the volatility of a resource-constrained future. By treating “global hectares” with the same scrutiny as “dollars and cents,” Americans can build a lifestyle that is not only environmentally sustainable but financially invincible. The goal is clear: move away from a deficit-based lifestyle—both ecologically and monetarily—and toward a model of regenerative wealth that serves both the individual and the planet.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.