In the complex landscape of personal finance and international business, documentation is the bedrock upon which trust and legality are built. For millions of individuals navigating the transition into the United States economy, one specific identifier stands out as a primary key to unlocking financial opportunity: the A-Number. While often discussed in the context of immigration, the Alien Registration Number (A-Number) is a fundamental component of financial identity, influencing everything from credit scores to corporate payroll compliance.

For entrepreneurs, investors, and professionals, understanding what the A-Number is—and how it functions within the financial ecosystem—is essential. This guide explores the intersection of this unique identifier with banking, taxation, and long-term wealth building, providing a comprehensive look at how a simple seven- to nine-digit number facilitates participation in one of the world’s most robust financial markets.

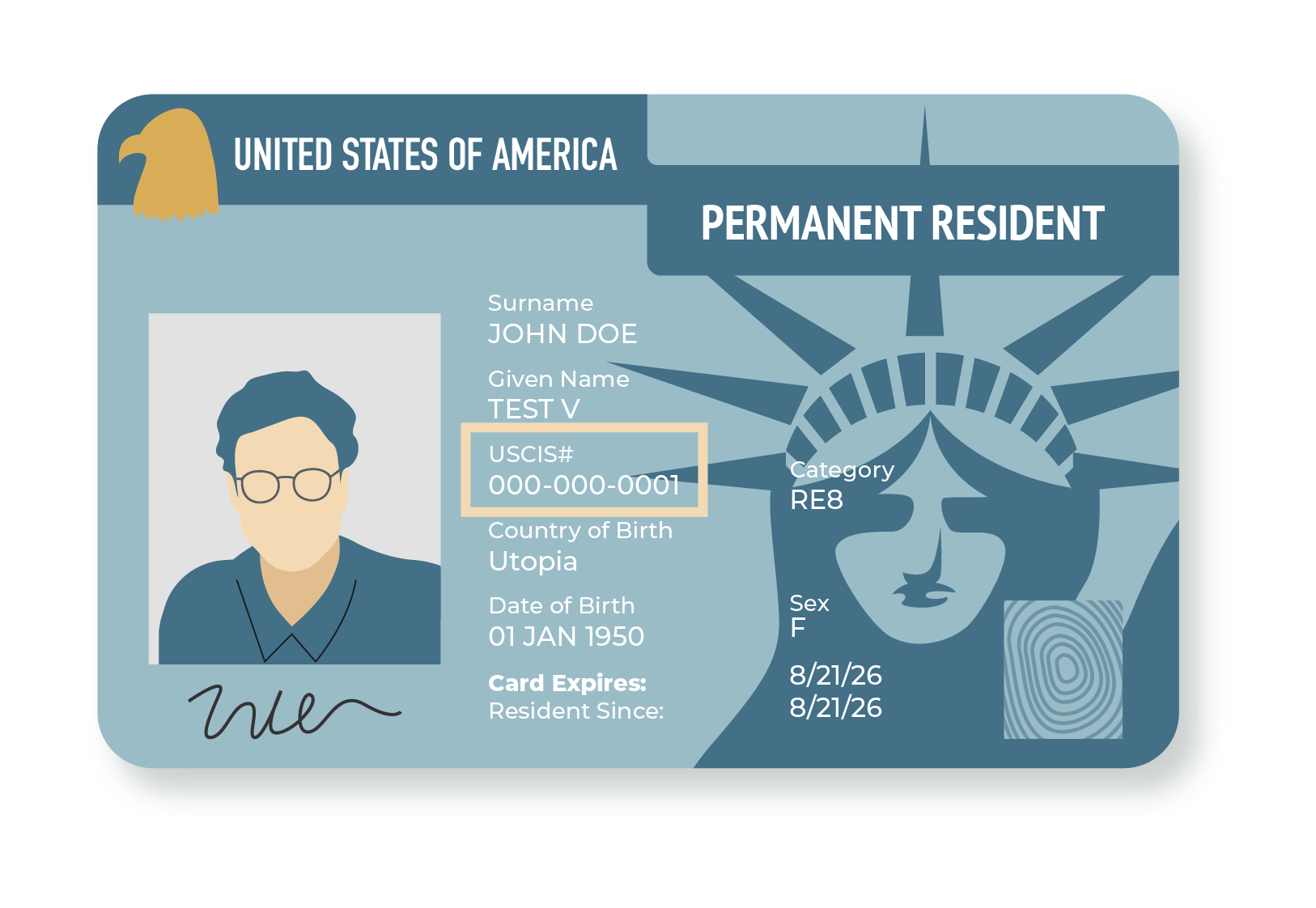

What is an A-Number and Why Does it Matter for Your Finances?

At its core, the A-Number is a unique identification number assigned by the Department of Homeland Security (DHS) to non-citizens. However, to view it strictly as a “legal” or “immigration” figure is to ignore its immense weight in the world of money. In the United States, your ability to generate income, store wealth, and access credit is tied to your identity. The A-Number serves as the primary financial “fingerprint” for those who do not yet possess a Social Security Number (SSN) or are in the process of transitioning their legal status.

Defining the Alien Registration Number

The A-Number, also known as a USCIS Number, is a permanent identifier. Unlike a visa, which might expire or change based on your travel status, the A-Number stays with an individual for life. In the realm of personal finance, this permanence is vital. It allows financial institutions to track a person’s history and ensure that the “John Doe” who opened a bank account five years ago is the same “John Doe” now applying for a mortgage. For those involved in business finance, the A-Number is the bridge that allows non-citizens to be legally onboarded into a company’s financial systems.

The Difference Between an A-Number, SSN, and ITIN

Navigating the American financial system requires an understanding of the “alphabet soup” of identification. While the SSN is the gold standard for financial tracking, many people starting their journey in the U.S. use an A-Number first.

- A-Number: Identifies a person’s status and right to be in the country/work.

- SSN: Primarily for tax reporting and social security benefits, but used by banks for credit tracking.

- ITIN (Individual Taxpayer Identification Number): Used specifically for tax processing by the IRS for those who cannot get an SSN.

For many, the A-Number is the precursor to the SSN. Understanding this hierarchy is the first step in strategic financial planning. Without a properly recorded A-Number, a non-citizen may find themselves “invisible” to the traditional banking system, making it impossible to leverage their income for future growth.

Navigating the Financial System: Banking and Credit with an A-Number

One of the most significant challenges for those new to the U.S. economy is establishing a financial footprint. Without a history of credit or a verifiable identity, an individual is often locked out of low-interest loans, credit cards, and even basic checking accounts. The A-Number acts as a vital tool in overcoming these barriers.

Opening Bank Accounts as a Non-Citizen

Modern banking is governed by “Know Your Customer” (KYC) and Anti-Money Laundering (AML) regulations. Banks are legally required to verify the identity of anyone opening an account to prevent financial crimes. For non-citizens, the A-Number—provided via a Green Card or an Employment Authorization Document (EAD)—is often the primary document used to satisfy these requirements.

When a financial institution recognizes an A-Number, it creates a profile that allows the individual to deposit earnings, pay bills, and participate in the digital economy. This is the first step in personal finance management: moving away from a cash-based existence and into a system that offers protection, interest-bearing accounts, and the ability to manage money through modern apps and tools.

Building Credit History Using Your Unique Identifier

In the United States, “Money” isn’t just about what you have; it’s about what you can borrow. Credit scores dictate the cost of life—from the interest rate on a car loan to the ability to rent an apartment. While credit bureaus primarily use SSNs to track history, many modern fintech companies and forward-thinking banks allow individuals to start building a profile using their A-Number and other identifying documents.

By using the A-Number to secure a “secured credit card” or a small credit-builder loan, individuals can begin demonstrating financial responsibility. Over time, this history becomes a valuable asset. When an individual eventually transitions to an SSN, their history tied to their A-Number can often be linked, ensuring that years of hard work and timely payments are not lost in the transition.

The A-Number in Business and Employment Finance

For business owners and corporate finance departments, the A-Number is not just a personal identifier; it is a compliance necessity. Hiring international talent or managing a diverse workforce requires a deep understanding of how this number interacts with payroll and tax law.

Payroll Compliance and the Form I-9

Every time a business hires a new employee in the U.S., they must complete a Form I-9, Employment Eligibility Verification. For non-citizen employees, the A-Number is the key piece of data required to confirm that the individual is legally allowed to work and receive a salary. From a business finance perspective, failing to properly record and verify an A-Number can lead to massive fines and legal liabilities.

Efficient payroll systems are built on accurate data. For CFOs and HR managers, ensuring that the A-Number is correctly integrated into the company’s financial software is paramount. This ensures that tax withholdings are accurate and that the company remains in good standing with federal labor and financial regulators.

Tax Obligations and the Role of Financial Identification

The intersection of the A-Number and the IRS is where “Money” and “Compliance” truly meet. Even if an individual does not yet have an SSN, they may have tax obligations based on their income earned within the U.S. The A-Number is frequently used on tax-related documents to ensure that earnings are properly reported.

For entrepreneurs operating as “resident aliens” for tax purposes, the A-Number serves as a link between their legal status and their business’s financial reporting. Understanding how to use this number for filing taxes correctly is the difference between a thriving business and one bogged down by audits and penalties. It is the foundation of “tax hygiene,” a concept every serious investor and business person must master.

Strategic Financial Planning for Non-Citizens

Beyond the basics of banking and payroll, the A-Number plays a role in sophisticated financial strategies. Whether it’s investing in the stock market or planning for retirement, your identification status dictates the tools available to you.

Investment Opportunities and Regulatory Requirements

To invest in U.S. markets—whether through a brokerage account like Robinhood, Schwab, or a 401(k) provided by an employer—you must have a verified identity. For many international professionals working in the tech or finance sectors on H-1B or L-1 visas, their A-Number is the primary identifier used during the “onboarding” process for these investment platforms.

Investing is the primary way to build long-term wealth. By understanding how to use their A-Number to open brokerage accounts, individuals can begin participating in compounding returns. This allows them to build a “portable” wealth portfolio that remains theirs, regardless of where their career eventually takes them. In the world of money, the A-Number is the ticket that grants entry into the most liquid and lucrative markets on earth.

Protecting Your Financial Identity

As with any unique identifier, the security of an A-Number is paramount. In an age of digital fraud and identity theft, protecting this number is a critical aspect of personal finance. If an A-Number is compromised, it can lead to fraudulent employment claims, “synthetic” identity theft, and the ruining of a burgeoning credit profile.

Financial literacy involves more than just making money; it involves defending it. Professional advice suggests treating an A-Number with the same level of secrecy as a Social Security Number. By using digital security tools, monitoring credit reports, and being cautious with whom this number is shared, individuals can safeguard their financial future.

Conclusion: The A-Number as a Financial Asset

While the A-Number is birthed from administrative requirements, its true value is found in the financial freedom it facilitates. It is the starting point for a non-citizen’s financial journey in the United States, acting as the bridge between “outsider” and “active participant” in the economy.

From the simple act of opening a savings account to the complex process of corporate payroll compliance and stock market investing, the A-Number is an indispensable tool. By understanding its nuances, individuals can better navigate the path to creditworthiness, and businesses can ensure they are operating within the legal frameworks that govern modern finance. In the final analysis, the A-Number is more than just a digit on a card—it is a cornerstone of financial identity and a catalyst for economic growth.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.