As we navigate the economic landscape, planning for retirement remains a paramount concern for individuals across all career stages. The 401(k) stands as a cornerstone of many Americans’ retirement strategies, offering tax advantages and a disciplined approach to saving. Each year, the Internal Revenue Service (IRS) adjusts the maximum allowable contributions to these plans, primarily influenced by inflation and cost-of-living adjustments. Understanding these limits, especially for an upcoming year like 2025, is crucial for maximizing your savings potential and ensuring a secure financial future. While the official 2025 limits are typically announced in late October or early November of the preceding year (i.e., late 2024), we can project and prepare based on current trends, historical adjustments, and the most recent 2024 figures. This article will delve into what these limits entail, why they matter, and how you can strategically plan to optimize your contributions for 2025.

Understanding Your 401(k) and Its Importance

Before we project the numbers for 2025, it’s essential to grasp the fundamental nature of a 401(k) and why maximizing your contributions is a smart financial move. This understanding forms the bedrock of effective retirement planning.

What is a 401(k)?

A 401(k) is an employer-sponsored retirement savings plan that allows employees to invest a portion of their pre-tax or after-tax (Roth) salary. Contributions grow tax-deferred until retirement (for traditional 401(k)s) or tax-free upon withdrawal in retirement (for Roth 401(k)s), provided certain conditions are met. One of its most attractive features is often an employer matching contribution, which is essentially “free money” that significantly boosts your retirement savings. The plan’s tax benefits, combined with the power of compounding interest over decades, make it an incredibly potent tool for building wealth for your golden years.

Why Maximizing Contributions Matters

Maximizing your 401(k) contributions offers a multitude of benefits that extend beyond simply saving for retirement. Firstly, it leverages the tax advantages unique to these plans, either reducing your current taxable income (traditional 401(k)) or providing tax-free income in retirement (Roth 401(k)). Secondly, it ensures you take full advantage of any employer match, which can equate to thousands of dollars in additional savings annually. Thirdly, consistent, high contributions harness the power of compounding, allowing your investments to grow exponentially over time. Failing to contribute the maximum means leaving potential tax savings, employer contributions, and significant compound growth on the table, ultimately delaying or diminishing your retirement security.

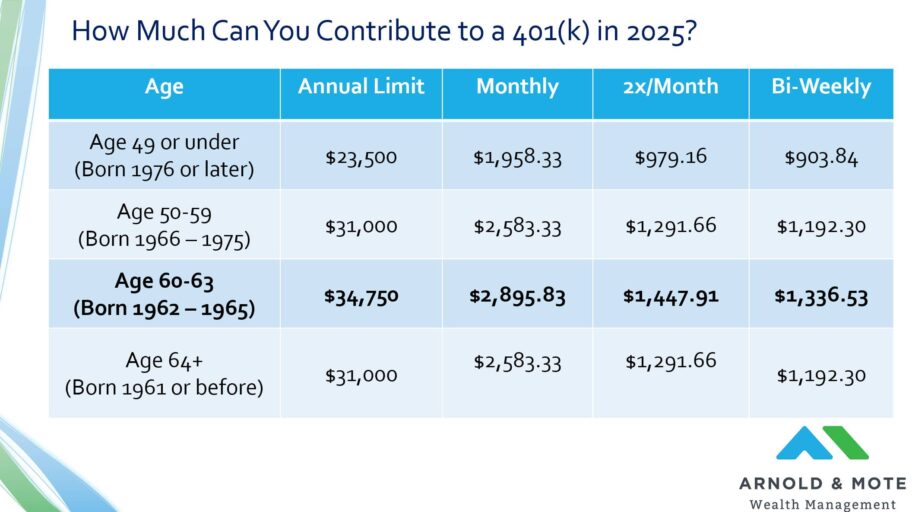

Projecting the 2025 401(k) Contribution Limits

While the exact figures for 2025 are yet to be officially released by the IRS, we can make informed projections based on the formula used for adjustments and recent inflation trends. The IRS typically bases these adjustments on the Consumer Price Index for All Urban Consumers (CPI-U).

How Limits Are Determined: The Role of Inflation

The IRS adjusts 401(k) contribution limits annually based on inflation and specific indexing rules outlined in the tax code. These adjustments are designed to ensure that the purchasing power of retirement savings is maintained over time, even as the cost of living increases. Significant inflation, as observed in recent years, often leads to more substantial increases in contribution limits. Conversely, periods of low inflation might see smaller adjustments or even no change in limits. Understanding this mechanism helps set expectations for the 2025 figures.

The Standard Employee Contribution Limit (and 2024 comparison)

For 2024, the standard employee contribution limit for a 401(k) (and similar plans like 403(b)s and most 457 plans) was set at $23,000. Given the ongoing inflationary pressures and historical patterns, it is highly probable that this limit will see an increase for 2025.

- Projection for 2025: Based on recent inflation rates, it’s reasonable to expect the standard employee contribution limit to increase by at least $500, potentially reaching $23,500 or $24,000 for 2025. A more aggressive projection, should inflation remain elevated, could even push it slightly higher.

The Catch-Up Contribution for Those 50 and Over (and 2024 comparison)

Individuals aged 50 or older are permitted to make additional “catch-up” contributions to their 401(k)s. This provision is designed to allow older workers to boost their retirement savings as they approach retirement age, especially if they started saving later in life or experienced career interruptions. For 2024, the catch-up contribution limit remained at $7,500.

- Projection for 2025: The catch-up contribution limit has been less consistent in its annual adjustments compared to the standard limit. While it has remained stable for a few years, a significant increase in the standard limit for 2025 might also trigger an increase in the catch-up contribution. A conservative estimate would be for it to remain at $7,500, but an increase to $8,000 is plausible if overall inflation warrants it.

The Total 401(k) Contribution Limit (Employer + Employee)

Beyond individual employee contributions, there’s an overarching limit on the total contributions that can be made to a defined contribution plan like a 401(k) in a given year, which includes both employee contributions (pre-tax, Roth, and catch-up) and employer contributions (matching and profit-sharing). For 2024, this total limit was $69,000 (or $76,500 for those aged 50 and over).

- Projection for 2025: This total limit is also adjusted for inflation. Given the likely increase in the standard employee limit, the total contribution limit is also expected to rise. We could see this figure reach $70,000 to $71,000 (or $77,500 to $79,000 for those 50 and over) for 2025.

Strategies for Maximizing Your 401(k) Contributions

Knowing the limits is only half the battle; the other half is implementing strategies to actually hit those targets. Maximizing your 401(k) contributions requires discipline, planning, and an understanding of how to best leverage your employer’s plan.

The Power of Dollar-Cost Averaging

Dollar-cost averaging involves investing a fixed amount of money at regular intervals, regardless of market fluctuations. When applied to 401(k) contributions, this means consistently contributing a set percentage or amount from each paycheck. This strategy helps mitigate risk by averaging out your purchase price over time and ensures you buy more shares when prices are low and fewer when prices are high. It’s an effortless way to ensure you’re continuously contributing towards the limit throughout the year.

Taking Advantage of Employer Matches

Perhaps the most straightforward strategy for boosting your 401(k) is to always contribute at least enough to receive your full employer match. This is, quite literally, free money that employers offer as a benefit. Failing to contribute enough to capture the full match is akin to turning down a guaranteed return on investment. If your employer matches 50% of your contributions up to 6% of your salary, ensure you’re contributing at least 6% to unlock that additional 3% from your employer.

Utilizing Catch-Up Contributions

If you are 50 or older, make sure you are taking full advantage of the catch-up contribution provision. This additional contribution amount allows you to significantly accelerate your retirement savings in your prime earning years. It can be a game-changer for those who started saving later or faced financial setbacks. Even if you’re not 50 yet, understanding this future option can influence your long-term savings plan.

The Mega Backdoor Roth Strategy (if applicable to plan)

For high-income earners who have already maxed out their traditional and Roth IRA options, and their standard 401(k) contributions, the “Mega Backdoor Roth” strategy can be a powerful tool. This involves contributing after-tax money to your 401(k) (if your plan allows for after-tax non-Roth contributions), and then converting that money into a Roth 401(k) or Roth IRA. This allows you to bypass income limitations for direct Roth contributions and push more money into a tax-free growth vehicle, up to the overall total 401(k) limit (employee + employer contributions). It’s a complex strategy that requires your plan to allow after-tax contributions and in-plan Roth conversions, so consult with your plan administrator and a financial advisor.

Budgeting and Automation

The most effective way to hit the annual contribution limit is through meticulous budgeting and automation. Review your household budget to identify areas where you can trim expenses and reallocate those funds to your 401(k). Then, set up automatic payroll deductions to ensure that a fixed percentage or dollar amount is contributed from each paycheck. If you aim to hit the maximum, divide the projected limit by the number of paychecks you receive in a year to determine the exact amount you need to contribute per pay period. This “set it and forget it” approach makes it easier to stay on track.

Benefits of Hitting the 401(k) Limit

Committing to maximizing your 401(k) contributions provides a wealth of advantages that can significantly impact your financial well-being, both in the short term and throughout your retirement.

Tax Advantages (Pre-tax vs. Roth 401k)

The tax benefits are a primary draw of 401(k) plans. With a traditional (pre-tax) 401(k), your contributions reduce your taxable income in the current year, potentially lowering your immediate tax burden. Your investments grow tax-deferred, meaning you don’t pay taxes on earnings until you withdraw them in retirement. A Roth 401(k), on the other hand, involves after-tax contributions, but qualified withdrawals in retirement are entirely tax-free. Maxing out either type provides substantial tax savings, either now or in the future.

Compounding Growth for Retirement Security

Perhaps the most powerful benefit of consistent, maximal 401(k) contributions is the effect of compounding. Over decades, even modest returns on significant principal amounts can lead to exponential growth. The more you contribute early and consistently, the more time your money has to grow, potentially accumulating a substantial nest egg that can support a comfortable retirement lifestyle. Hitting the limit means you’re giving your money the maximum possible runway for this growth.

Reducing Your Taxable Income

For traditional 401(k)s, every dollar you contribute reduces your current year’s taxable income. If the 2025 limit is, for example, $24,000, and you contribute that full amount, your taxable income is reduced by $24,000. Depending on your tax bracket, this can translate into significant immediate tax savings, effectively making your retirement savings less costly. This immediate tax benefit can be a strong incentive to reach the maximum contribution.

Achieving Financial Independence Sooner

By consistently maxing out your 401(k) and leveraging other retirement accounts, you accelerate your journey towards financial independence. A robust retirement fund provides the flexibility to retire earlier, transition to part-time work, or pursue passions without financial constraint. The security and options that a well-funded 401(k) offers can transform your later years into a period of freedom and enjoyment rather than financial worry.

Preparing for 2025 and Beyond

Successful long-term financial planning is an ongoing process that requires vigilance, adaptability, and a willingness to seek expert advice. As you look towards 2025 and beyond, a few key actions will help ensure you remain on track to meet your retirement goals.

Staying Informed About IRS Updates

The most critical step in preparing for 2025 is to stay informed. Keep an eye on IRS announcements, typically in late October or early November, for the official 401(k) contribution limits for the upcoming year. Reliable financial news sources, your 401(k) plan administrator, or a financial advisor can provide these updates. Once the official numbers are released, adjust your payroll contributions accordingly to ensure you hit the new maximum.

Reviewing Your Financial Plan Annually

An annual review of your overall financial plan is highly recommended. This includes assessing your current income, expenses, investment performance, and retirement goals. Are your contributions still aligned with your objectives? Have your life circumstances changed (e.g., marriage, children, career change) that might warrant adjustments to your savings strategy? This holistic review ensures that your 401(k) contributions are part of a larger, coherent financial strategy.

Consulting a Financial Advisor

Navigating the complexities of retirement planning, especially for high-income earners or those with unique financial situations, can be challenging. A qualified financial advisor can provide personalized guidance, help you understand the nuances of various retirement vehicles (including 401(k)s, IRAs, HSAs, etc.), optimize your investment strategy, and ensure you’re making the most of all available tax advantages. They can also help clarify specific rules, like those for the Mega Backdoor Roth, and ensure your plan aligns with your broader financial goals.

In conclusion, while the official 401(k) contribution limits for 2025 are still pending, proactive planning based on current projections and a solid understanding of your retirement strategy is essential. By consistently maximizing your contributions, leveraging employer matches, and staying informed, you can harness the full power of your 401(k) to build a secure and prosperous financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.