In the high-stakes world of professional sports, the line between victory and defeat is often drawn not on the hardwood, but within the complex spreadsheets of a front office. For the National Basketball Association (NBA), the 2023 Collective Bargaining Agreement (CBA) introduced a fiscal mechanism that has fundamentally altered the landscape of team building and financial management: the Second Apron. While casual fans focus on trades and points per game, the “Money” side of the league is currently obsessed with this punitive luxury tax tier. Understanding the Second Apron is essential for anyone interested in the business of sports, as it represents one of the most aggressive attempts at fiscal regulation in modern corporate entertainment.

The Mechanics of the Salary Cap and the Tax Apron System

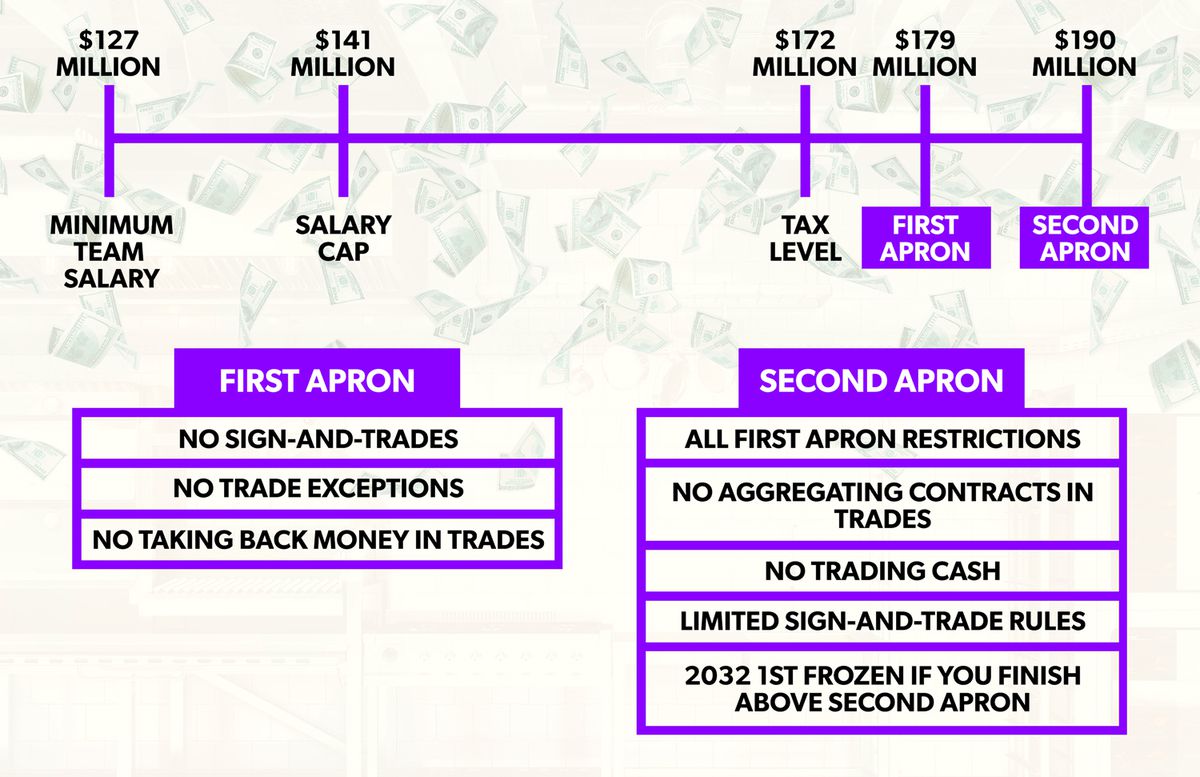

To understand the Second Apron, one must first grasp the foundational architecture of the NBA’s salary cap. Unlike “hard cap” systems found in other leagues, the NBA operates under a “soft cap,” allowing teams to exceed the cap through various exceptions. However, this flexibility comes at a steep financial price.

Defining the Luxury Tax Threshold

The luxury tax is the primary tool used by the league to maintain competitive balance. When a team’s total payroll exceeds a certain threshold—calculated annually based on Basketball Related Income (BRI)—they must pay a penalty for every dollar spent over that limit. In the current economic climate, this tax is graduated; the further a team goes into the red, the higher the “tax rate” per dollar. For the 2024-25 season, the luxury tax level is approximately $170.8 million.

The First Apron vs. The Second Apron

The “Aprons” are additional levels of spending above the luxury tax line that trigger increasingly severe operational restrictions. The First Apron is set roughly $7 million above the luxury tax line. Once a team crosses this, they lose certain trade flexibilities and the ability to sign players using the full Mid-Level Exception.

The Second Apron is the “final frontier” of spending, set approximately $17.5 million above the luxury tax line (roughly $188.9 million for the 2024-25 cycle). It is designed to be a “soft” hard cap. While a team is technically allowed to spend past it, the fiscal and operational penalties are so draconian that they serve as a massive deterrent for even the wealthiest ownership groups.

Financial Implications and Team Building Restrictions

The Second Apron is not merely a tax; it is a set of handcuffs designed to prevent “Super Teams” from using pure capital to monopolize talent. From a business finance perspective, it shifts the strategy from “spending for growth” to “optimizing for efficiency.”

The Elimination of the Mid-Level Exception

Historically, the Taxpayer Mid-Level Exception (MLE) was a vital financial tool that allowed championship contenders to sign veteran impact players despite being over the cap. Under the new Second Apron rules, teams above this threshold lose the MLE entirely. This means a team cannot sign a free agent for anything other than a minimum salary. In a corporate sense, this is the equivalent of a firm being barred from hiring mid-level management, forced instead to rely solely on entry-level interns or existing executive talent.

Salary Matching and Trade Limitations

In a standard NBA trade, teams can often take back more salary than they send out, within a certain percentage. For Second Apron teams, this flexibility vanishes. They cannot take back even one dollar more in a trade than they send out. Furthermore, they are prohibited from “aggregating” salaries—meaning they cannot trade two players making $10 million each to acquire one player making $20 million. This creates a liquidity crisis in the trade market, making it nearly impossible for high-spending teams to pivot their roster construction once they have committed to a core group.

Cash Considerations and Buyout Markets

The Second Apron also restricts a team’s ability to use cash in trades. In the past, wealthy owners could “buy” second-round draft picks or facilitate trades by sending millions of dollars to another team. Second Apron teams are now prohibited from sending cash in any transaction. Additionally, they are barred from signing players in the “buyout market” (players waived by other teams) if those players’ previous salaries exceeded the non-taxpayer mid-level exception. This effectively cuts off the supply of discounted veteran talent that usually flocks to contenders mid-season.

Long-term Financial Planning and the “Frozen” Draft Pick

One of the most innovative and terrifying aspects of the Second Apron from a strategic finance perspective is the “Frozen Pick” rule. This mechanism links current overspending to future asset depreciation, creating a long-term risk profile that forces owners to think years in advance.

The Repeater Tax Burden

The NBA’s “Repeater Tax” has long been a nightmare for owners, charging teams higher rates if they have been in the tax for three of the previous four years. When combined with the Second Apron, the financial outlay becomes exponential. A team deep into the Second Apron might find themselves paying $4 or $5 in taxes for every $1 of salary. For a team $40 million over the tax, this can result in a total tax bill exceeding $150 million—on top of the actual payroll.

The Draft Pick Penalty Mechanism

If a team finishes a season in the Second Apron, their first-round draft pick seven years into the future is “frozen.” This means the pick cannot be traded. If the team remains in the Second Apron for two of the following four seasons, that frozen pick is automatically moved to the very end of the first round (30th overall), regardless of the team’s actual record.

For a business, this is the equivalent of a regulatory body seizing future R&D assets because of current debt levels. It devalues the franchise’s long-term “portfolio” and makes it incredibly difficult to rebuild once the current roster ages out of their prime.

The Business Strategy Behind the Second Apron

The implementation of the Second Apron was a calculated move by the NBA’s Board of Governors to ensure the long-term sustainability of the league’s economic model. While it may seem like a punishment for success, it is actually a protective measure for the league’s collective revenue.

Enforcing Parity through Fiscal Restraint

In the previous era, teams in massive markets like San Francisco, Los Angeles, and New York could outspend small-market rivals by hundreds of millions of dollars. From a market health perspective, the NBA recognized that if only a few teams have a realistic shot at a title due to spending power, the “product” suffers in other markets. The Second Apron forces a level of parity by making it financially and operationally unsustainable to keep a high-priced roster together for more than a few years. It forces “talent churn,” ensuring that stars eventually hit the market or are traded to teams with more cap flexibility.

Protecting Small-Market Revenue and ROI

By limiting the spending of the “Goliaths,” the NBA protects the Return on Investment (ROI) for “David.” Small-market owners who cannot afford $200 million tax bills are now on a more level playing field. The Second Apron essentially mandates that championships must be won through savvy scouting, player development, and cap management rather than just a large checkbook. In the world of business finance, this is a transition from an “acquisition-based growth model” to an “organic growth model.”

The “Sting” of the Hard Cap

Ultimately, the Second Apron serves as a psychological barrier. Front offices now talk about “the apron” with more trepidation than they do the luxury tax itself. We are seeing teams trade away productive players or let key free agents walk simply to stay $1 under the Second Apron. This fiscal discipline is a new reality for the NBA, turning the role of the General Manager into something more akin to a Chief Financial Officer. Every roster move must now be audited for its “apron implications,” ensuring that the team maintains enough liquidity to make moves in the future.

In conclusion, the NBA’s Second Apron is a masterclass in regulatory financial engineering. It creates a high-stakes environment where one bad contract doesn’t just cost money—it costs the ability to trade, the ability to sign free agents, and the value of future assets. For the teams that can navigate these waters with precision, the rewards are immense. For those who mismanage their cap, the Second Apron is a fiscal trap that can take a decade to escape. In the modern NBA, the game is won in the margins of the CBA, and the Second Apron is the most significant margin of all.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.