Navigating the complexities of life insurance requires more than just a basic understanding of monthly premiums and death benefits. For many policyholders, life insurance is not just a safety net for their loved ones; it is a sophisticated financial asset that can accumulate tangible wealth over time. One of the most critical concepts in the management of this asset is the “surrender value.”

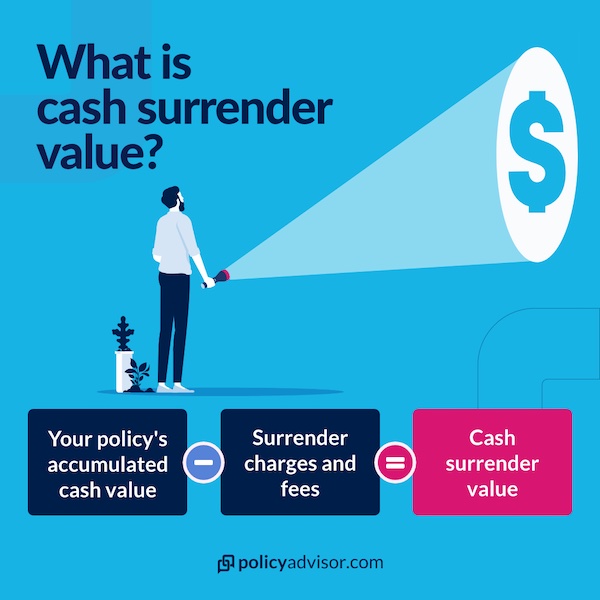

The surrender value represents the actual sum of money an insurance company will pay to a policyholder if they decide to terminate their policy before it matures or before the insured event occurs. While the concept sounds straightforward, the financial mechanics behind it are intricate, involving various fees, growth rates, and tax considerations. Understanding the nuances of surrender value is essential for anyone looking to optimize their personal finance strategy and ensure their long-term wealth is managed effectively.

Decoding Surrender Value: More Than Just a Cancellation Fee

To understand surrender value, one must first distinguish between different types of life insurance. Surrender value is almost exclusively associated with permanent life insurance policies—such as Whole Life or Universal Life—rather than term life insurance. Term life insurance provides coverage for a specific period and does not accumulate cash value; if you cancel a term policy, you simply walk away without any payout. Permanent life insurance, however, contains a savings or investment component known as “cash value.”

How Cash Value Accumulates

When you pay a premium for a permanent life insurance policy, a portion of that payment goes toward the cost of insurance (the death benefit protection) and administrative fees. The remaining portion is funneled into a cash value account. This account grows over time, often at a guaranteed minimum rate set by the insurer or through market-linked gains in the case of variable policies. As the policy matures, this cash value becomes a significant reservoir of liquidity.

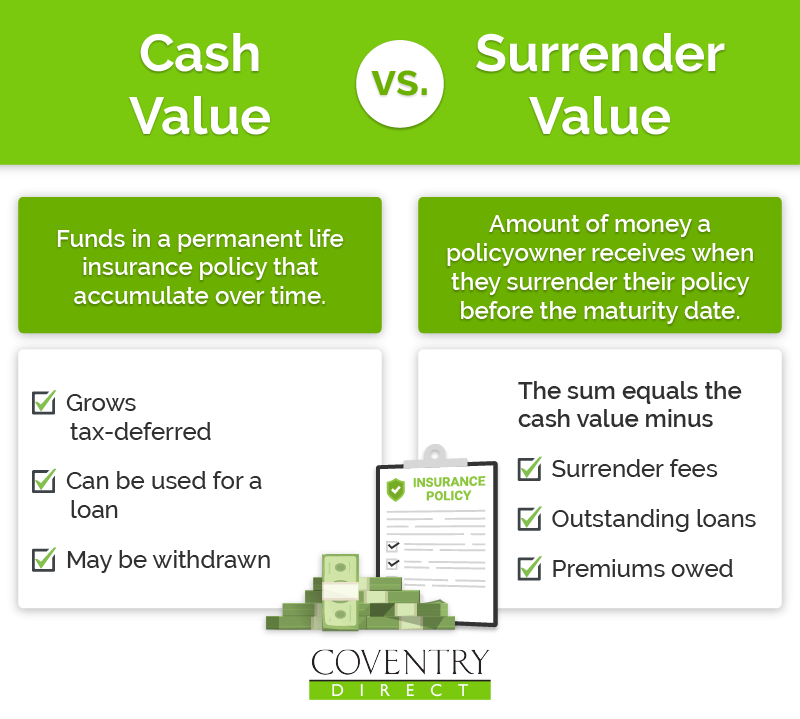

The surrender value is essentially this cash value minus any “surrender charges” applied by the insurance company. In the early years of a policy, the surrender value might be significantly lower than the total cash value because the insurance company needs to recoup the high costs associated with setting up the policy and paying agent commissions.

The Difference Between Face Value and Surrender Value

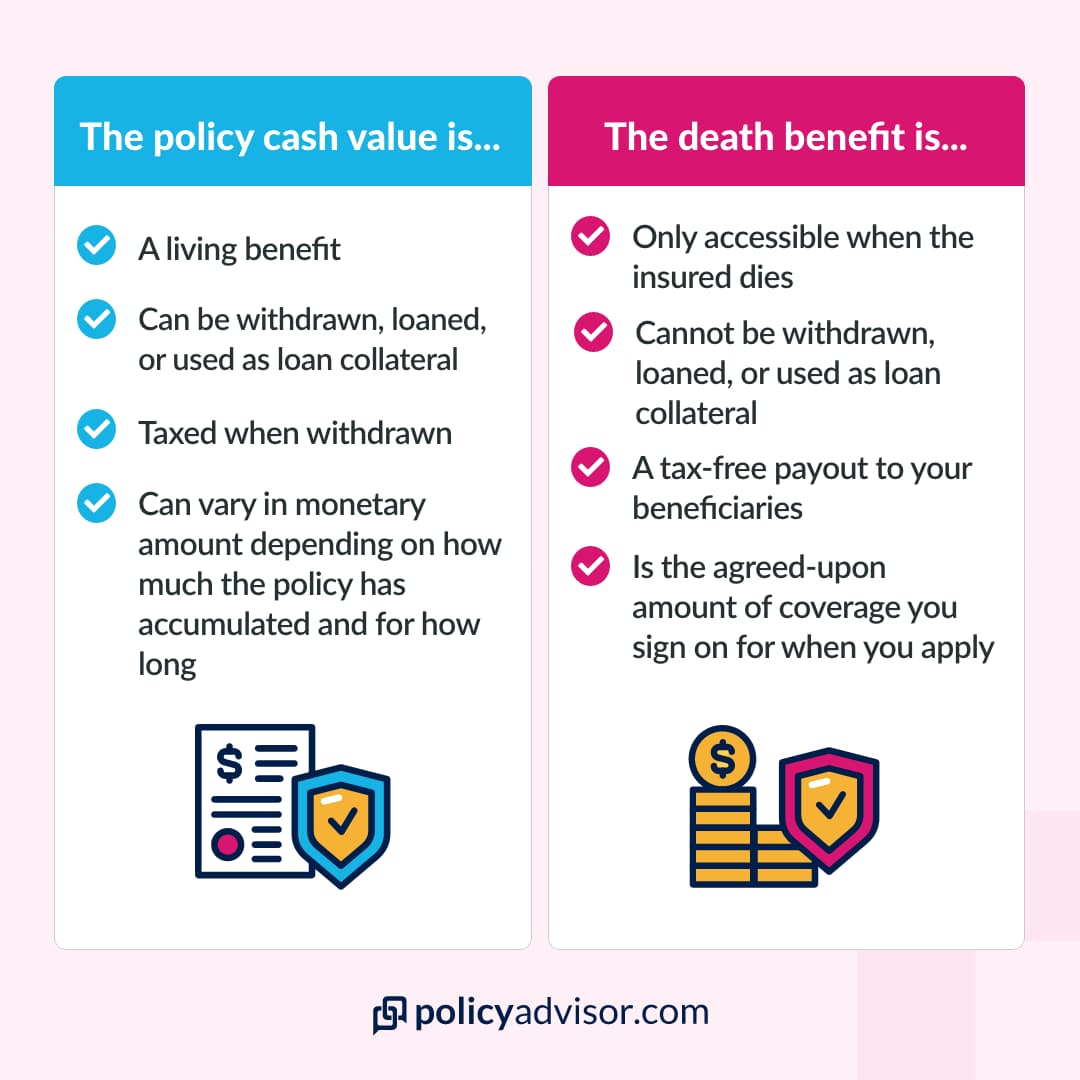

A common point of confusion for policyholders is the distinction between the “face value” and the “surrender value.” The face value, or death benefit, is the amount paid to your beneficiaries upon your passing. This is typically a much larger sum. The surrender value, conversely, is the “living benefit”—the amount you can access while you are alive if you choose to forfeit the death benefit. It is a critical distinction in financial planning: the face value protects your family’s future, while the surrender value provides current liquidity.

Factors That Determine Your Policy’s Cash Worth

The amount of money you receive upon surrendering a policy is not arbitrary. It is the result of a precise actuarial calculation that takes several variables into account. For a policyholder, monitoring these factors is key to determining the right time to exit or modify a policy.

Premiums and Time: The Compound Growth Factor

The most significant driver of surrender value is time. Because cash value accumulation relies on compounding interest and the steady contribution of premiums, policies that have been in force for decades typically have substantial surrender values. In the first few years of a policy, the surrender value is often zero or negligible. However, as the policy enters its second and third decades, the growth curve steepens. This is why financial advisors often view permanent life insurance as a long-term play rather than a short-term savings vehicle.

Surrender Charges and Administrative Fees

Most permanent life insurance policies include a “surrender charge period,” which can last anywhere from 5 to 15 years. If you cancel the policy during this window, the insurer deducts a percentage of the cash value as a penalty. These charges are usually highest in the first year and gradually decrease to zero as the surrender period expires. Understanding the schedule of these charges is vital; surrendering a policy in year nine when the charges drop off in year ten could result in a significant and unnecessary financial loss.

Outstanding Loans and Unpaid Premiums

One of the benefits of a cash-value policy is the ability to take out a policy loan against it. However, it is important to remember that any outstanding loan balance, including accrued interest, will be deducted from the cash value before the surrender payment is made. Similarly, if you have used the cash value to pay for premiums (a common feature in universal life policies), those “withdrawals” will reduce your final surrender value.

When and Why Should You Surrender a Life Insurance Policy?

Deciding to surrender a life insurance policy is a major financial move that should not be taken lightly. By surrendering, you are effectively ending your coverage and leaving your beneficiaries without a death benefit. However, there are strategic reasons why a policyholder might choose to walk away with the cash.

Navigating Financial Hardship

Life is unpredictable. If a policyholder faces an immediate need for capital—perhaps due to a medical emergency, a business failure, or the threat of foreclosure—the surrender value of a life insurance policy can act as an emergency fund of last resort. While it is rarely the first choice for liquidity, the ability to access thousands of dollars in cash can be a lifesaver in dire economic circumstances.

Reallocating Capital for Better Returns

In the world of investing, “opportunity cost” is a vital metric. If a policy is underperforming or if the internal fees are eating away at the growth, a savvy investor might decide that the surrender value could be better utilized elsewhere. For example, if the cash value is growing at a modest 3%, but the policyholder identifies an investment opportunity with an expected 8% return, surrendering the policy and reallocating that capital into a brokerage account or real estate could lead to higher long-term net worth.

Downsizing Insurance Needs in Retirement

Insurance needs change as we age. A person in their 30s with a mortgage and young children has a massive need for a large death benefit. However, a person in their 70s with a paid-off home, grown children, and a robust pension may no longer require that protection. In this scenario, the life insurance policy may have served its purpose. Surrendering the policy allows the individual to convert an unneeded death benefit into cash that can be used to fund their retirement lifestyle or travel.

The Alternatives to Surrendering Your Policy

Before signing the papers to surrender a policy, it is essential to explore alternatives that might provide the necessary cash without completely forfeiting the insurance coverage. In many cases, these alternatives offer a more favorable financial outcome.

Policy Loans: Accessing Cash Without Canceling

Instead of surrendering the policy, you can borrow against the cash value. Policy loans typically offer lower interest rates than traditional bank loans and do not require a credit check. The best part is that the policy remains in force. If you die before the loan is repaid, the balance is simply deducted from the death benefit paid to your beneficiaries. This allows for liquidity while maintaining protection.

Life Settlements: Selling the Policy on the Secondary Market

For seniors, a “life settlement” is often a much more lucrative option than surrendering the policy back to the insurance company. In a life settlement, you sell your policy to a third-party investor for a lump sum. This sum is invariably higher than the surrender value, though lower than the death benefit. The investor then takes over the premium payments and collects the death benefit when you pass away. This is a sophisticated financial maneuver that treats the policy like a tradable asset.

Reduced Paid-Up Insurance

If the primary goal is to stop paying premiums rather than to get a lump sum of cash, you can opt for “reduced paid-up insurance.” In this scenario, the insurance company uses the current cash value to “buy” a smaller death benefit that is fully paid for. You will never have to pay another premium, and your beneficiaries will still receive a payout, albeit a smaller one than originally planned.

Tax Implications and Long-Term Financial Planning

The surrender of a life insurance policy is not a tax-neutral event. The IRS views the cash value growth as taxable income under certain conditions. Understanding these rules is critical to ensure you don’t lose a significant portion of your payout to the government.

The Cost Basis vs. Taxable Gain

When you surrender a policy, the portion of the payout that is equal to the total premiums you have paid into the policy is considered a return of principal and is tax-free. This is known as your “cost basis.” Any amount you receive above that cost basis—the growth—is taxed as ordinary income. For policies that have been held for a long time, the taxable gain can be substantial, and failure to account for this can lead to an unexpected tax bill.

Consulting with Financial Advisors

Given the complexity of surrender charges, tax consequences, and the loss of death benefits, the decision to surrender should always be made in consultation with a financial advisor or tax professional. They can help run a “break-even analysis” to determine if the move makes sense within the context of your broader financial portfolio.

Ultimately, the surrender value is a powerful tool in your financial arsenal. It represents the flexibility and tangible worth of a permanent life insurance policy. By understanding how it is calculated, when to access it, and what the alternatives are, you can make informed decisions that protect your wealth and serve your long-term financial goals. Whether you choose to hold your policy for life or liquidate it for a new opportunity, being informed about surrender value ensures that you—not the insurance company—remain in control of your financial destiny.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.