When building a robust personal finance strategy, most individuals prioritize emergency funds, retirement accounts, and standard life insurance. However, a comprehensive financial plan often requires more nuanced layers of protection to account for specific, high-impact risks. One such layer is Supplemental Accidental Death and Dismemberment (AD&D) insurance.

While it is frequently offered as an add-on to employer-sponsored benefit packages, many policyholders remain unclear about its actual value, its limitations, and how it fits into a broader wealth-preservation strategy. This guide explores the mechanics of supplemental AD&D insurance from a financial perspective, helping you determine if it is a necessary expenditure for your specific economic situation.

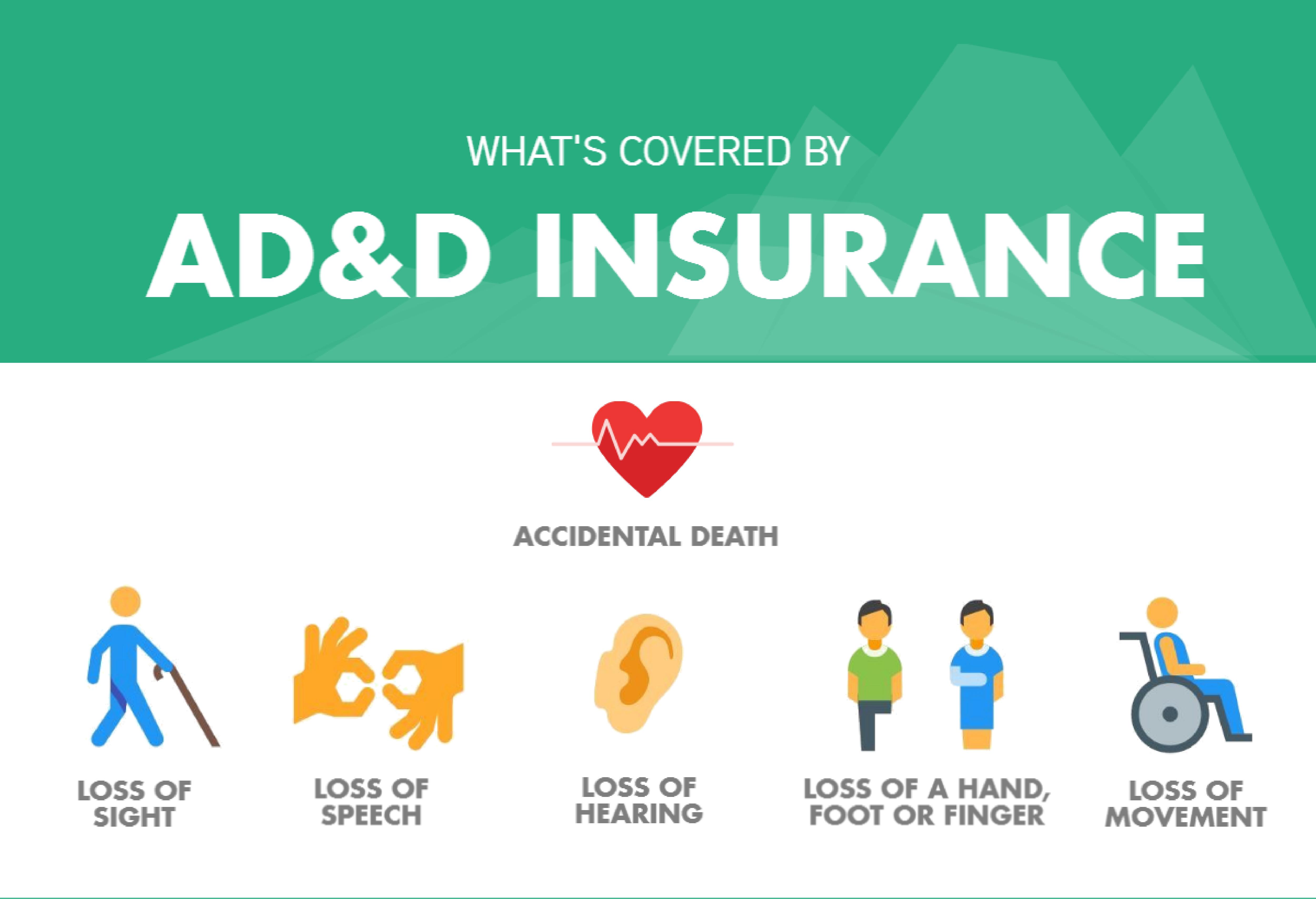

Decoding the Mechanics of Accidental Death and Dismemberment

At its core, Accidental Death and Dismemberment (AD&D) insurance is a specialized form of coverage that pays out a lump sum if the policyholder dies or suffers a specific, life-altering injury due to a covered accident. Unlike traditional life insurance, which typically covers death by most causes (including illness and natural causes), AD&D is strictly limited to “accidental” events.

The Core Coverage: Death vs. Living Benefits

The financial payout from an AD&D policy is divided into two primary categories. The “Accidental Death” portion functions similarly to life insurance; if the insured party passes away due to a car crash, a fall, or another qualifying accident, the designated beneficiaries receive a death benefit. This is often referred to as “double indemnity” when it is attached as a rider to a standard life insurance policy, effectively doubling the payout in the event of an accident.

The “Dismemberment” portion provides what are known as “living benefits.” This is a crucial distinction in personal finance because a catastrophic injury often carries a heavier long-term financial burden than a death. If an individual survives an accident but loses a limb, their sight, or their hearing, the financial impact includes not only immediate medical bills but also a potential loss of future earning capacity. AD&D provides a liquidity injection during these crises to help offset those costs.

Understanding the Dismemberment Schedule

AD&D policies operate on a “schedule of benefits.” This means the payout is not always 100% of the policy’s face value. Instead, the payout is tiered based on the severity of the loss. For instance, the loss of a single limb or the sight in one eye might result in a 50% payout of the total coverage amount, while the loss of two limbs or total paralysis might trigger the full 100% payout.

From a financial planning standpoint, it is essential to read the “fine print” of these schedules. Understanding exactly what percentage of the benefit is paid out for specific injuries allows an individual to assess whether the coverage adequately protects their specific career-related risks. A surgeon, for example, might view the loss of a hand differently than a software developer, making the dismemberment schedule a vital piece of their risk-management puzzle.

Why “Supplemental” Matters in Personal Finance

The term “supplemental” indicates that this coverage is purchased in addition to a base layer of protection—usually a group life insurance policy provided by an employer. While many employers provide a basic level of AD&D for free, “supplemental” AD&D allows the employee to pay an additional premium to increase their coverage limits significantly.

Bridging the Gap in Employer-Sponsored Plans

Standard employer-provided life insurance often equals one or two times an employee’s annual salary. For many families, this amount is insufficient to cover a mortgage, education costs for children, and long-term inflation. Supplemental AD&D serves as a cost-effective way to “bridge the gap.” Because AD&D only covers accidents, the premiums are significantly lower than those for standard term life insurance. This allows a person to secure a high coverage limit (e.g., $500,000 or $1,000,000) for a relatively small monthly payroll deduction, providing a massive financial buffer in the event of a tragedy.

Portability and Financial Independence

One of the major risks of relying solely on employer-provided insurance is the lack of portability. If you leave your job, your coverage usually ends. However, many supplemental AD&D policies offer “portability” or “conversion” options. This allows the individual to maintain the coverage even after a career change, ensuring that their financial safety net remains intact regardless of their employment status. In the context of “Money” and personal finance, maintaining continuous coverage is a cornerstone of avoiding “uninsured gaps” that could devastate a family’s net worth.

Evaluating the ROI of AD&D Policies

Every financial decision involves a trade-off. When deciding whether to allocate capital toward supplemental AD&D premiums, one must consider the Return on Investment (ROI) in terms of risk mitigation.

Premium Accessibility and Leveraged Protection

The primary financial appeal of AD&D is its “leverage.” For a few dollars a month, you can secure a payout that is hundreds of times the premium cost. For younger individuals or those in high-risk occupations (such as construction, transportation, or field engineering), the statistical likelihood of an accident vs. a natural death is higher than for the elderly. In these cases, supplemental AD&D offers high-value protection for a low opportunity cost. The money saved on these lower premiums can then be diverted into higher-yield investment vehicles, like a Roth IRA or an index fund, allowing for a more efficient allocation of capital.

The Impact of Exclusions on Financial Planning

From a strictly financial perspective, AD&D has a significant drawback: it is “narrow-spectrum” insurance. It does not pay out for deaths caused by heart attacks, cancer, or other illnesses—which account for the vast majority of deaths globally. Furthermore, most policies exclude “high-risk” activities such as skydiving, car racing, or even certain types of travel.

If a policyholder views AD&D as a replacement for life insurance, they are making a dangerous financial error. AD&D should be viewed as a supplement, not a substitute. A sound financial strategy uses term life insurance to cover all-cause mortality and uses AD&D to provide an extra layer of protection against the specific, sudden, and often expensive nature of accidental trauma.

AD&D vs. Traditional Life Insurance: A Strategic Comparison

To optimize one’s financial portfolio, it is necessary to understand how AD&D differs from traditional life insurance and where each fits within a wealth-management framework.

Fixed vs. Variable Risks

Traditional life insurance (Term or Whole Life) covers “fixed risks”—the certainty that everyone will eventually pass away. Because the payout is much more certain, the premiums are higher. AD&D covers “variable risks”—events that might happen but are not guaranteed. This is why AD&D is so much cheaper.

When managing a household budget, the strategic approach is to ensure the “fixed risk” is covered first. Once a base life insurance policy is in place to cover the family’s basic needs (mortgage, debt, income replacement), supplemental AD&D can be added to address the “variable risk” of an accident that could result in permanent disability or sudden death, which often requires immediate, large-scale liquidity.

Building a Multi-Layered Financial Safety Net

Think of your financial protection like a pyramid. The base is your emergency fund (liquidity). The middle layer is your standard life and disability insurance (all-cause protection). The top layer is supplemental AD&D.

This top layer is particularly useful for individuals who do not yet have significant assets. For someone in their 20s or 30s who is still in the “wealth accumulation” phase, an accidental injury that prevents them from working could derail their entire financial future. Supplemental AD&D provides a “stop-loss” mechanism that protects their most valuable asset: their ability to earn an income over the next several decades.

Conclusion: Integrating AD&D into Your Long-Term Financial Roadmap

Supplemental AD&D insurance is a powerful, low-cost tool in the personal finance arsenal, but it must be used correctly. It is not a “set-it-and-forget-it” solution, nor is it a comprehensive life insurance policy. Instead, it is a targeted financial instrument designed to provide massive liquidity in the face of specific, catastrophic accidents.

When deciding whether to opt for supplemental AD&D, evaluate your current lifestyle, your occupation’s risk level, and the current gaps in your insurance portfolio. If you find that your current life insurance wouldn’t sufficiently cover the extra medical and lifestyle-adjustment costs of a major injury, or if you want an inexpensive way to boost your family’s inheritance in a worst-case scenario, supplemental AD&D is a mathematically sound choice. By strategically layering this coverage over a solid foundation of traditional insurance and diversified investments, you can ensure that your financial journey remains on track, even when the unexpected occurs.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.