Saving, at its core, is the act of setting aside a portion of one’s current income or wealth for future use rather than spending it immediately. While seemingly straightforward, the concept of saving is a cornerstone of personal finance, a critical component of economic stability, and a deeply psychological exercise. It represents a conscious decision to defer gratification, prioritize future security, and build a foundation for achieving financial aspirations. Far from being a mere passive accumulation of funds, effective saving is an active strategy that underpins financial independence, resilience, and the pursuit of long-term wealth.

The Fundamental Concept of Saving

To truly understand what saving entails, we must look beyond its simplest definition and appreciate its multifaceted implications for individuals, families, and even national economies. It’s not just about accumulating money; it’s about strategically allocating resources across time.

More Than Just Stashing Cash

In its most basic form, saving might conjure images of money tucked away in a piggy bank or under a mattress. However, in the modern financial landscape, saving is a much more sophisticated endeavor. It involves making informed choices about where to store funds (savings accounts, money market accounts, certificates of deposit), how to protect them from inflation, and how to make them grow through interest or investment returns. It’s a dynamic process that evolves with one’s financial journey and goals.

The Core Principles: Present Sacrifice for Future Gain

The essence of saving lies in the trade-off between immediate consumption and future benefit. Every dollar saved today is a dollar not spent on a current want or need. This act of deferring gratification is a powerful financial discipline. It acknowledges that current resources are finite and that by allocating some to the future, one can address unforeseen challenges, capitalize on opportunities, and build a more secure existence. This principle is foundational to wealth creation, as it shifts focus from transient pleasures to enduring security and prosperity.

Why Saving is Indispensable for Financial Well-being

Saving is not merely a good habit; it is an indispensable pillar of financial well-being. Without a robust savings strategy, individuals are vulnerable to life’s inevitable curveballs – job loss, medical emergencies, or unexpected home repairs. Beyond defensive measures, saving is the engine that drives progress towards aspirational goals, whether it’s buying a home, funding a child’s education, starting a business, or enjoying a comfortable retirement. It provides peace of mind, reduces stress, and opens doors to choices that would otherwise be unattainable.

Understanding the Mechanisms and Psychology Behind Saving

While the objective of saving is clear, the actual execution often involves navigating human psychology and implementing practical financial mechanisms.

Behavioral Economics of Saving: Overcoming Instant Gratification

One of the biggest hurdles to saving is the human tendency towards instant gratification. Our brains are often wired to prioritize immediate rewards over future benefits. This is where behavioral economics sheds light on why saving can be challenging and how to overcome these innate biases. Concepts like “present bias” and “hyperbolic discounting” explain why people struggle to save even when they understand its importance. Recognizing these psychological barriers is the first step towards building effective saving habits. Strategies often involve making the future benefits more tangible or making the act of saving less effortful.

Practical Approaches: Budgeting and Tracking Your Money

Effective saving begins with a clear understanding of one’s financial inflows and outflows. Budgeting is the primary tool for this. By meticulously tracking income and expenses, individuals can identify where their money is going, pinpoint areas for reduction, and consciously allocate funds to savings goals. Whether using spreadsheets, budgeting apps, or traditional pen and paper, a budget acts as a financial roadmap, transforming vague intentions into actionable plans. It provides clarity and control, empowering individuals to make deliberate choices about their spending versus saving.

Automating Your Savings: The Path of Least Resistance

One of the most powerful strategies for consistent saving is automation. By setting up automatic transfers from a checking account to a savings or investment account on payday, individuals bypass the need for conscious decision-making each time. This “set it and forget it” approach leverages behavioral insights by removing willpower from the equation and making saving the default action. Automating savings ensures consistency, reduces the temptation to spend the money, and allows savings to accumulate steadily over time without constant effort.

Diverse Forms and Purposes of Saving

Saving is not a monolithic activity; it manifests in various forms, each serving a distinct purpose within a comprehensive financial plan. Understanding these different types is crucial for strategic financial management.

Emergency Funds: Your Financial Safety Net

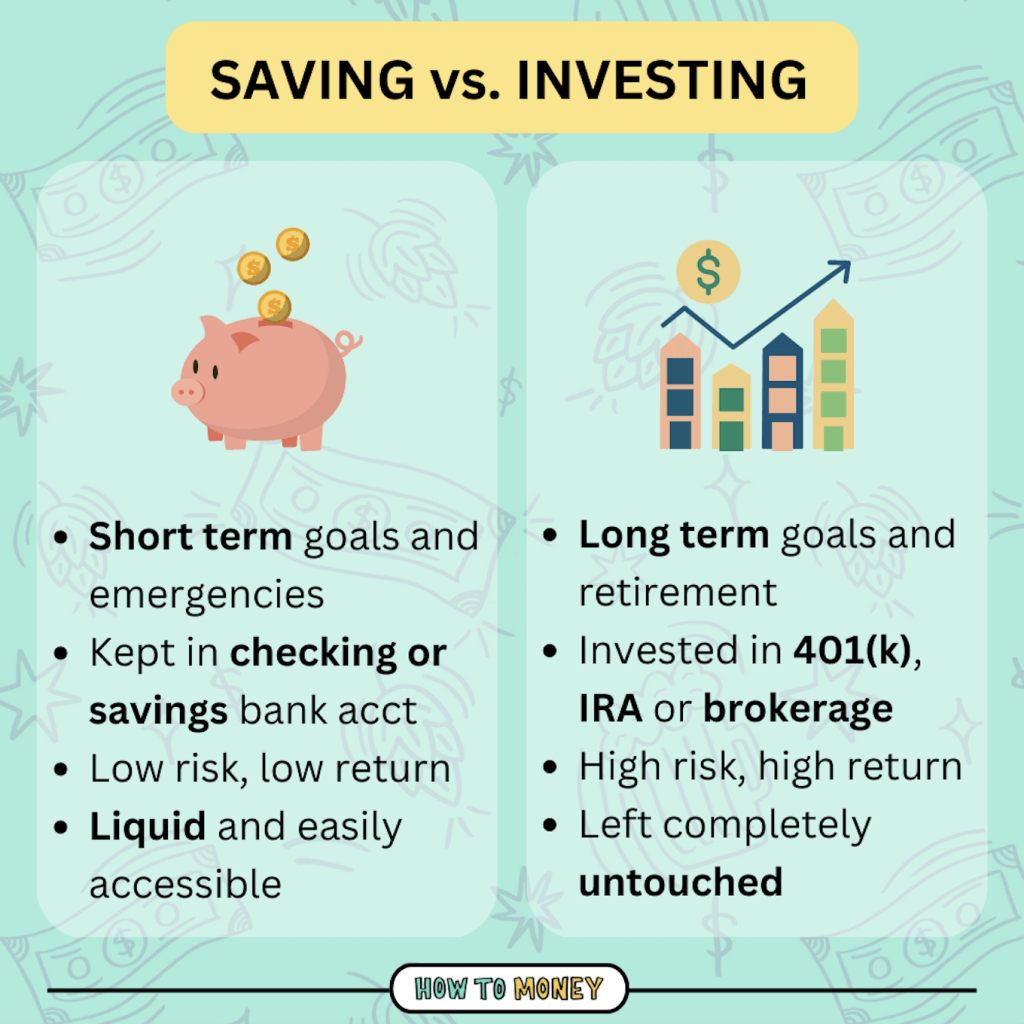

Perhaps the most critical form of saving is the emergency fund. This is a dedicated pool of money, typically held in an easily accessible, liquid account (like a high-yield savings account), designed to cover unexpected expenses or income disruptions. Experts generally recommend having 3 to 6 months’ worth of essential living expenses saved. An emergency fund acts as a financial shock absorber, preventing individuals from going into debt or derailing other financial goals when unforeseen circumstances arise.

Short-Term Goals: From Vacations to Down Payments

Beyond emergencies, saving is essential for achieving specific short-term goals, usually those within a 1-5 year horizon. This could include saving for a down payment on a car, a much-needed vacation, a new appliance, or professional development courses. These goals provide motivation and allow individuals to enjoy planned large purchases without incurring high-interest debt. Separate savings accounts for each short-term goal can help keep funds organized and visually track progress.

Long-Term Aspirations: Retirement and Wealth Accumulation

For goals extending beyond five years, such as retirement planning, a child’s college education, or significant wealth accumulation, saving transitions into investing. While still fundamentally “saving” for the future, the approach shifts to utilizing investment vehicles that offer the potential for higher returns over the long term, such as stocks, bonds, mutual funds, and real estate. The primary objective here is to not only preserve capital but also to grow it significantly, often leveraging the power of compound interest to outpace inflation and build substantial wealth.

Specialized Savings Vehicles: IRAs, 401(k)s, and Beyond

Governments and financial institutions offer various specialized savings vehicles designed to encourage long-term saving, especially for retirement. These often come with tax advantages, making them particularly attractive.

- 401(k)s (and 403(b)s for non-profits): Employer-sponsored retirement plans that allow employees to contribute pre-tax income, often with an employer match, and grow tax-deferred.

- IRAs (Individual Retirement Accounts): Personal retirement accounts that individuals can open independently. Both Traditional IRAs (tax-deductible contributions, tax-deferred growth) and Roth IRAs (after-tax contributions, tax-free withdrawals in retirement) offer distinct benefits.

- HSAs (Health Savings Accounts): Tax-advantaged savings accounts that can be used for healthcare expenses and also serve as an excellent long-term investment vehicle for retirement if not used for health costs.

Understanding and utilizing these accounts can significantly enhance the efficiency and growth of long-term savings.

Strategies for Effective and Sustainable Saving

Building a robust savings habit requires more than just good intentions; it demands strategic planning and consistent execution.

Setting SMART Financial Goals

The foundation of effective saving is setting SMART goals: Specific, Measurable, Achievable, Relevant, and Time-bound. Instead of a vague goal like “I want to save more,” a SMART goal would be, “I will save $5,000 for a down payment on a car by December 31st of next year by setting aside $416.67 each month.” SMART goals provide clarity, motivation, and a framework for tracking progress, making the saving journey tangible and manageable.

The Power of the “Pay Yourself First” Principle

The “Pay Yourself First” principle is a cornerstone of successful saving. It means treating your savings contributions as a non-negotiable expense, just like rent or utilities, and prioritizing them immediately upon receiving income. Before paying bills, buying groceries, or indulging in discretionary spending, a portion of your income goes directly into savings or investment accounts. This psychological shift ensures that saving isn’t an afterthought but a primary financial commitment, leading to consistent accumulation of wealth.

Reducing Expenses: Finding Opportunities to Cut Back

While increasing income can boost saving capacity, for many, the most immediate and controllable lever is reducing expenses. This involves a critical review of spending habits to identify areas where costs can be cut without significantly impacting quality of life. This could range from small daily adjustments (e.g., brewing coffee at home instead of buying it) to larger lifestyle changes (e.g., optimizing utility usage, negotiating insurance premiums, or finding cheaper alternatives for subscriptions). Every dollar saved from expenses is a dollar that can be directed towards financial goals.

Increasing Income: Boosting Your Saving Capacity

Complementing expense reduction, actively seeking ways to increase income can dramatically accelerate saving efforts. This might involve negotiating a raise, taking on a side hustle, monetizing a hobby, freelancing, or investing in skills that lead to higher-paying job opportunities. A higher income provides more discretionary funds, making it easier to meet living expenses while simultaneously allocating a larger percentage towards savings and investments without feeling deprived.

The Compounding Effect: Saving’s Secret Weapon

The true magic of long-term saving, especially when coupled with investing, lies in the power of compounding.

Understanding Compound Interest: Money Making Money

Compound interest is often referred to as the “eighth wonder of the world” for good reason. It’s the process where the interest earned on an initial sum (principal) also earns interest. In essence, your money starts making money, and that “money making money” then starts making even more money. Over time, this snowball effect can lead to exponential growth, far surpassing what simple interest alone could achieve. The longer your money compounds, the more dramatic the results become.

The Advantage of Starting Early

The most crucial factor in harnessing compound interest is time. The earlier you start saving and investing, the more years your money has to compound and grow. Even small, consistent contributions made early in life can accumulate into substantial wealth over several decades, often outperforming much larger contributions made later on due to the power of extended compounding. This highlights why financial advisors consistently advocate for beginning retirement savings as soon as one starts earning an income.

Avoiding Common Saving Pitfalls

Despite the clear benefits, many individuals fall prey to common saving pitfalls. These include lifestyle inflation (increasing spending as income rises, rather than saving more), succumbing to impulsive purchases, failing to plan for large irregular expenses, neglecting to automate savings, and not regularly reviewing and adjusting financial goals. Overcoming these pitfalls requires discipline, regular financial check-ups, and a commitment to long-term vision over short-term desires.

In conclusion, “what is saving?” is a question with a profound and comprehensive answer in the realm of personal finance. It is an act of deliberate financial planning, a psychological battle against immediate gratification, and a strategic allocation of resources designed to build security, achieve aspirations, and foster long-term prosperity. By understanding its fundamental principles, adopting effective strategies, and leveraging the power of compounding, individuals can transform the abstract concept of saving into a tangible pathway to a secure and abundant financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.