Navigating the landscape of modern banking requires more than just knowing your account balance; it requires a fundamental understanding of the digital plumbing that moves money across the globe. For customers of Capital One, one of the most vital pieces of information in this infrastructure is the routing number. Whether you are setting up a direct deposit for a new job, authorizing an automated bill payment, or initiating a wire transfer to close on a home, your routing number serves as the essential GPS coordinate for your funds.

In the realm of personal finance, precision is synonymous with security. Understanding how Capital One utilizes routing numbers—and why they might differ depending on your account type or location—is a cornerstone of proactive financial management.

The Fundamentals: What a Routing Number Represents in the Financial Ecosystem

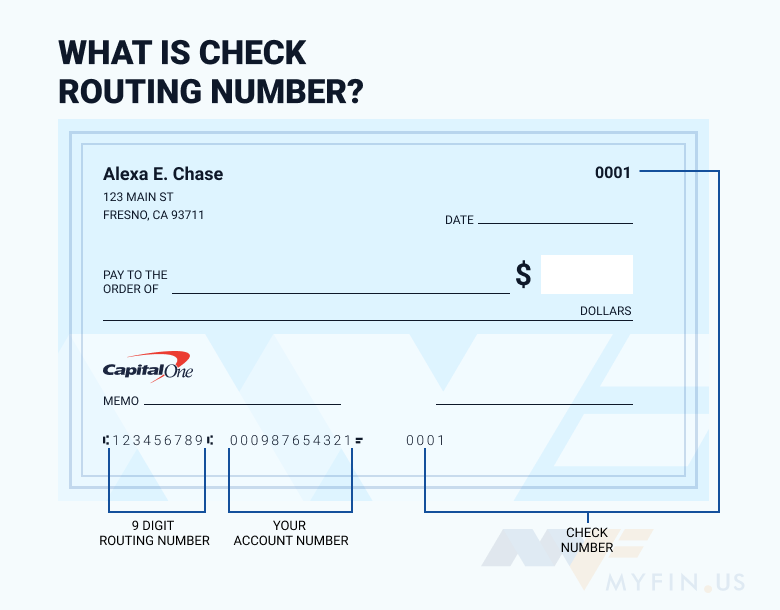

A routing transit number (RTN) is a nine-digit code used by financial institutions to identify themselves within the United States. Developed by the American Bankers Association (ABA) in 1910, this system was originally designed to facilitate the sorting and shipping of paper checks. Today, it serves as the backbone of the Automated Clearing House (ACH) network and electronic funds transfers.

The Anatomy of the Nine-Digit Code

Every routing number is structured with specific intent. The first four digits represent the Federal Reserve Bank district through which the institution’s electronic items are routed. The next two digits indicate the specific thrift or bank identifier, and the seventh digit identifies the specific Federal Reserve check processing center. Finally, the ninth digit serves as a “check digit,” a mathematical verification tool used to ensure the integrity of the previous eight digits during automated processing.

Why the Routing Number Matters for Your Net Worth

From a personal finance perspective, the routing number is the gateway to automation. Financial success is often built on the “set it and forget it” principle—automating savings, investments, and bill payments. Without the correct routing number, this automation fails, potentially leading to missed investment opportunities, late fees, or disrupted cash flow. For Capital One customers, ensuring this number is accurate is the first step in building a frictionless financial life.

Locating Your Capital One Routing Number: A Strategic Approach

Capital One is a unique entity in the banking world, having evolved from a credit card specialist into a full-service banking powerhouse. Because of its history of acquisitions—such as the purchase of ING Direct—the bank utilizes different routing numbers based on the type of account you hold and the state in which you opened it.

Capital One 360 vs. Traditional Retail Banking

The most common distinction for Capital One customers is between “360” accounts (primarily digital-first accounts) and traditional retail banking accounts.

- Capital One 360 Accounts: Most Capital One 360 checking and savings accounts utilize a unified routing number, often associated with their operations in St. Cloud, Minnesota. This simplification is part of the brand’s effort to streamline digital banking.

- Traditional Bank Accounts: If you opened an account at a physical Capital One branch (particularly in states like New York, New Jersey, Texas, or Louisiana), your routing number is likely tied to the specific geographic charter of that region.

Digital Tools for Instant Retrieval

In the age of mobile-first finance, you do not need to hunt for a paper checkbook to find your routing number. Capital One provides several secure digital avenues:

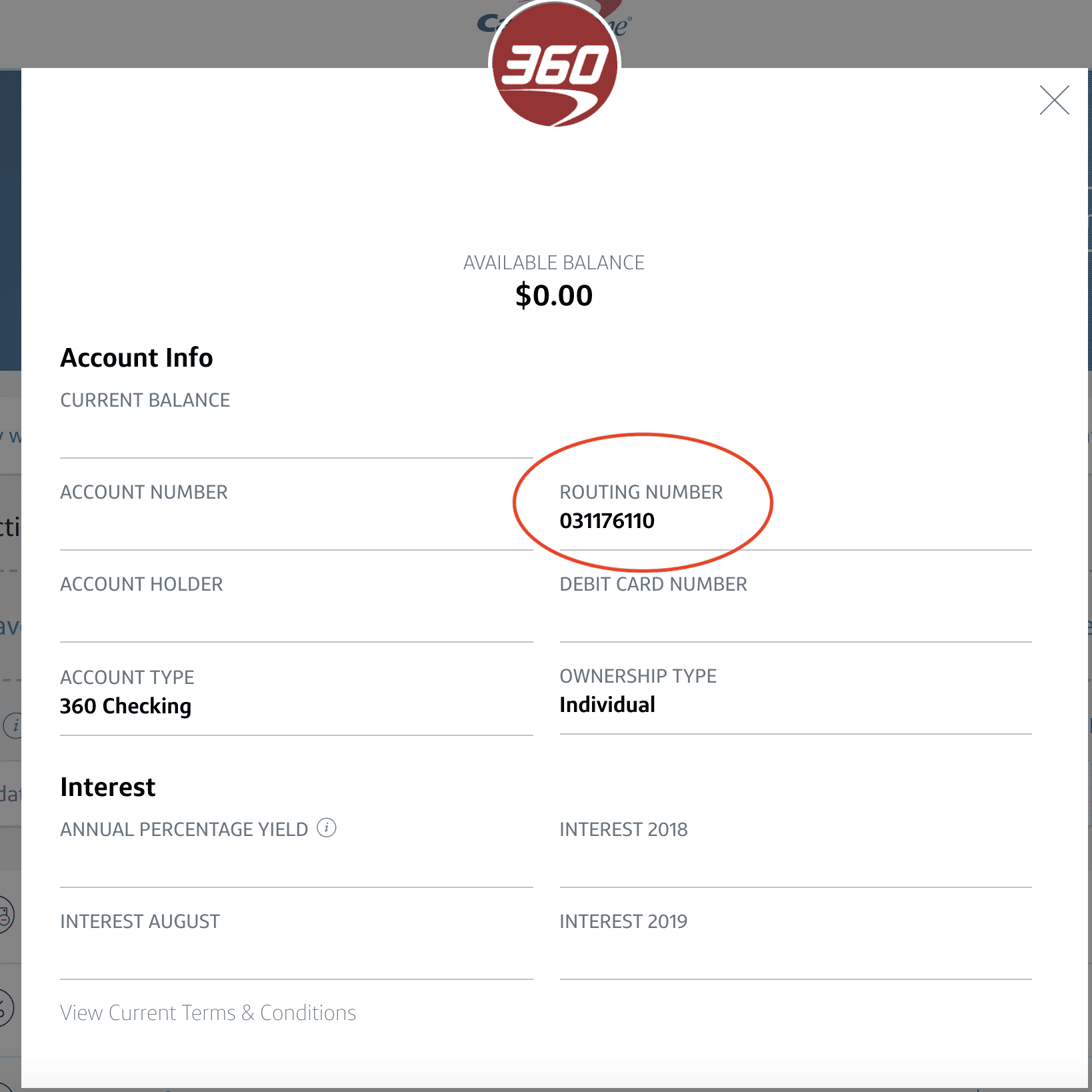

- The Capital One Mobile App: By selecting your specific checking or savings account and navigating to “Account Details,” the routing and account numbers are clearly displayed.

- Online Banking Portal: Similar to the app, the web interface provides a “Show Number” toggle under the account summary.

- Electronic Statements: Every monthly PDF statement generated by Capital One includes the routing number in the header or the account summary section.

Geographic Variations

For those with legacy or retail accounts, the routing number can vary significantly by state. For example, a customer in Virginia will have a different routing number than a customer in Texas. It is imperative to verify the specific number for your state of residence at the time of account opening, as using the wrong regional number can result in rejected transfers or “return-to-sender” notifications on electronic payments.

Optimizing Cash Flow: When and How to Use Your Routing Number

In the world of business and personal finance, timing is everything. Knowing which number to use—and when—can save you both time and money in the form of avoided fees and faster liquidity.

Streamlining Income via Direct Deposit

The most frequent use of a routing number is for direct deposit. By providing your employer with your Capital One routing and account numbers, you bypass the “float” of a physical check. Furthermore, Capital One often offers “Early Payday,” a feature where they credit your account as soon as they receive the payroll notification from your employer, sometimes up to two days early. This acceleration of cash flow allows for earlier debt repayment or immediate allocation into high-yield savings vehicles.

ACH Transfers vs. Domestic Wire Transfers

It is a common misconception that routing numbers are universal for all types of transfers. While your standard 9-digit routing number works for ACH transfers (like utility bills or transferring money between your own banks), it may not always be the number required for a domestic wire transfer.

- ACH Transfers: Generally free but take 1–3 business days.

- Wire Transfers: Usually incur a fee (at both the sending and receiving ends) but offer near-instantaneous movement of large sums of money.

Before initiating a wire, always confirm with Capital One if they require a specific “Wire Routing Number,” which can sometimes differ from the standard ACH routing number.

International Logistics: SWIFT and BIC Codes

If you are receiving funds from an international source, a standard US routing number is insufficient. You will need a SWIFT code (Society for Worldwide Interbank Financial Telecommunication) or a BIC (Bank Identifier Code). For Capital One, international transfers often involve intermediary banks, and specific instructions must be followed to ensure the currency is converted and routed correctly without excessive “hidden” fees.

Safeguarding Your Financial Identity: Security Protocols

While a routing number is not “secret” in the same way a Social Security number is—after all, it is printed on the bottom of every check you write—it is still a critical piece of the identity theft puzzle. In the wrong hands, combined with your account number, it can be used to initiate unauthorized ACH debits.

Protecting Your Information in a Digital World

To maintain high levels of digital security, Capital One customers should practice “financial hygiene.” This includes:

- Avoiding Public Wi-Fi: Never access your banking app or copy your routing/account numbers while on unsecured public networks.

- Monitoring Account Activity: Use Capital One’s “Eno” assistant and real-time alerts to monitor for any unauthorized ACH transactions.

- Encryption: Only share your routing and account numbers through secure, encrypted portals provided by reputable employers or service providers.

What to Do in Case of Compromise

If you suspect that your account and routing number combination has been compromised, the protocol is swift: contact Capital One’s fraud department immediately. In many cases, they will need to close the existing account and issue a new account number. Interestingly, your routing number will likely stay the same (as it identifies the bank, not you), but the new account number will sever the link that hackers were attempting to exploit.

The Future of Routing: Fintech Integration and Evolution

The concept of a routing number is over a century old, but its role is changing as Capital One integrates more deeply with fintech tools. From Venmo and Cash App to sophisticated investment platforms like Vanguard or Robinhood, the routing number remains the primary bridge between traditional banking and the “New Economy.”

Integrating with Third-Party Financial Tools

When you link your Capital One account to a budgeting app like YNAB (You Need A Budget) or an investment platform, you are essentially creating a digital handshake. Capital One uses secure APIs (Application Programming Interfaces) to allow these tools to interact with your account. However, some older systems still require the manual entry of your routing and account numbers. In these instances, the precision of your routing number determines the success of your “round-up” savings or automated monthly contributions to your Roth IRA.

Moving Toward Real-Time Payments (RTP)

The banking industry is currently shifting toward Real-Time Payments (RTP). While the 9-digit routing number remains the standard for identification, the speed at which the “pipes” behind that number work is increasing. Capital One is at the forefront of this shift, participating in networks that aim to make the “three-day wait” for ACH transfers a relic of the past. As a consumer, this means your routing number will soon facilitate the movement of money with the speed of a text message, further enhancing your ability to manage liquidity in real-time.

Conclusion: Mastery of Your Financial Infrastructure

A routing number might seem like a dry, technical detail, but in the context of personal finance, it is a tool of empowerment. For Capital One customers, it represents the gateway to a sophisticated suite of financial products designed to build wealth and manage debt. By understanding the nuances of your specific routing number—whether it’s for a 360 Checking account or a regional retail branch—you ensure that your financial engine runs smoothly, securely, and efficiently.

Mastering these basics allows you to move beyond simple transactions and into the realm of strategic financial planning, where every dollar is routed exactly where it needs to be, exactly when it needs to be there.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.