The question of when to retire is rarely a single date on a calendar; rather, it is a complex intersection of federal regulations, state-specific pension rules, and personal financial readiness. For residents of the Buckeye State, determining the “retirement age” requires navigating a unique landscape, particularly for those employed in the public sector. Unlike many other states, Ohio has a robust independent pension system that operates alongside—and sometimes in lieu of—federal Social Security.

Whether you are a private-sector employee, a public servant, or an entrepreneur, understanding the various milestones of retirement age is critical for long-term wealth preservation and lifestyle planning. This guide explores the financial nuances of retirement ages in Ohio, from Social Security thresholds to the specific tiers of the Ohio Public Employees Retirement System (OPERS).

The Federal Foundation: Social Security and Full Retirement Age (FRA)

For the majority of Ohioans working in the private sector, the primary benchmark for retirement is the Full Retirement Age (FRA) established by the Social Security Administration. While you can technically “retire” at any age if your personal savings allow it, the federal government dictates specific ages at which you gain access to guaranteed income streams.

The 62, 67, and 70 Milestones

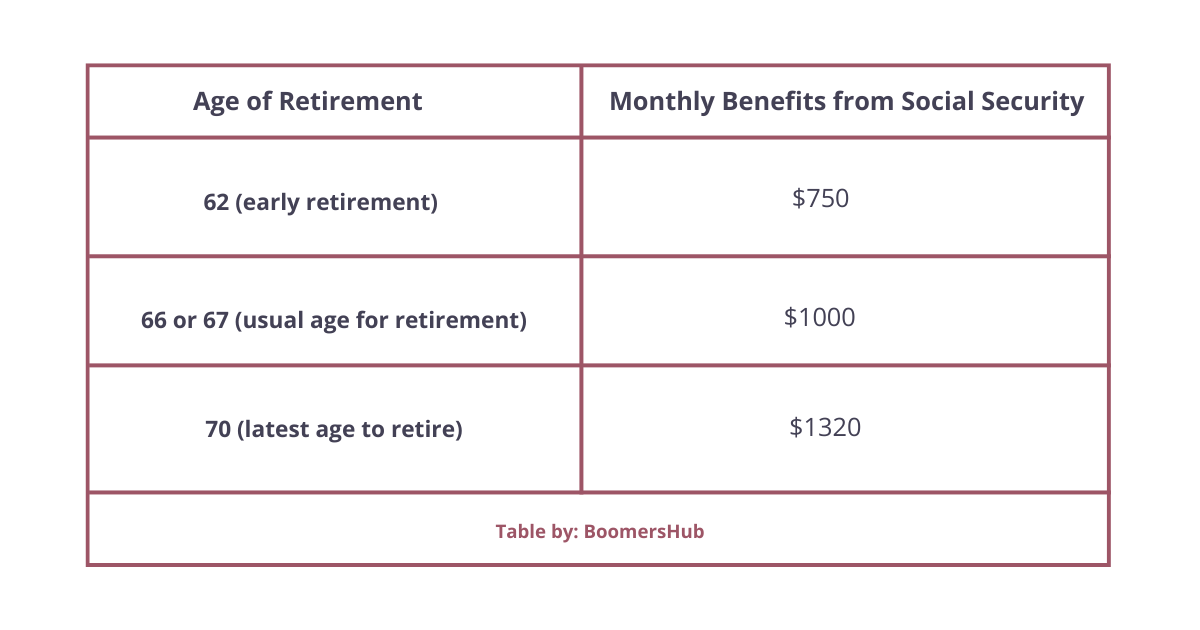

The earliest age you can begin claiming Social Security benefits is 62. However, choosing this path comes with a significant financial “haircut.” If you claim at 62, your monthly benefit is permanently reduced by up to 30% compared to what you would receive at your Full Retirement Age.

For those born in 1960 or later, the FRA is 67. This is the age at which you receive 100% of your primary insurance amount. However, the financial strategy doesn’t end there. For every year you delay claiming benefits beyond age 67—up until age 70—your benefit increases by approximately 8% per year. From a pure investment perspective, few market vehicles offer a guaranteed 8% annual return, making age 70 the “financial” retirement age for those looking to maximize their lifetime inflation-adjusted income.

How Ohio Residency Affects Federal Benefits

While Social Security is a federal program, Ohio is one of the more “retiree-friendly” states regarding how this income is handled. Ohio does not tax Social Security benefits at the state level. This means that when you reach your chosen retirement age, your federal checks go further in Ohio than they might in states that take a secondary cut of your retirement distributions.

Ohio’s Public Pension Landscape: OPERS, STRS, and SERS

Ohio is distinguished by its massive public pension systems. If you work for the state, a county, a municipality, or a public school, your retirement age is governed by different rules than the private sector. The Ohio Public Employees Retirement System (OPERS), the State Teachers Retirement System (STRS), and the School Employees Retirement System (SERS) utilize a “years of service” model that often allows for a much earlier retirement age than Social Security.

Understanding the Three Tiers of OPERS

Due to pension reforms over the last decade, your retirement age in the Ohio public sector depends heavily on when you were hired. OPERS categorizes members into three groups:

- Group A: Members who were eligible to retire on or before August 1, 2013.

- Group B: Members with at least 20 years of service credit or who were at least age 60 as of August 1, 2013.

- Group C: Newer employees or those who were far from retirement when the laws changed.

For Group C, the “unreduced” retirement age is typically 67 with 10 years of service, or age 55 with 32 years of service. This “Rule of 32” (or similar service-credit requirements) allows many Ohio public servants to retire in their mid-to-late 50s with a lifetime defined-benefit pension, a luxury rarely seen in the modern corporate world.

The Windfall Elimination Provision (WEP)

A critical financial trap for Ohio public employees is the Windfall Elimination Provision. Because many Ohio public positions do not pay into Social Security, if you have also worked in the private sector, your Social Security benefits may be reduced. When calculating your retirement age and expected income, you must account for this reduction. Relying on a standard Social Security statement without factoring in the WEP can lead to a significant shortfall in your retirement budget.

Private Sector Milestones: 401(k)s, IRAs, and the 59½ Rule

While the government and pension boards define ages for benefits, the tax code defines the age for access. For many Ohioans, “retirement age” is defined by the moment they can access their 401(k) or IRA without paying a 10% early withdrawal penalty to the IRS.

The 59½ Threshold

Regardless of whether you are in Cleveland, Cincinnati, or Columbus, the age of 59½ is a universal milestone for personal finance. This is the point at which the IRS allows penalty-free distributions from traditional IRAs and 401(k) plans. If you are planning an early retirement in Ohio, your financial strategy must bridge the gap between your stop-work date and age 59½.

Strategies such as the “Rule of 55″—which allows employees who leave their job in or after the year they turn 55 to take penalty-free distributions from their current employer’s 401(k)—are essential for those looking to exit the workforce before the standard thresholds.

Required Minimum Distributions (RMDs)

On the opposite end of the spectrum is the “maximum” retirement age, or more accurately, the age at which the government forces you to start spending your tax-advantaged savings. Under the SECURE Act 2.0, the age for Required Minimum Distributions (RMDs) has shifted to 73 (and will eventually move to 75). This is a crucial age for tax planning in Ohio. High-net-worth retirees must manage these distributions carefully to avoid being pushed into a higher state and federal tax bracket, potentially negating the benefits of Ohio’s lower cost of living.

Evaluating the Cost of Retirement in the Buckeye State

The age at which you can afford to retire in Ohio is heavily influenced by the state’s economic environment. Retirement age is not just a number of years lived; it is a calculation of whether your “nest egg” can withstand the local cost of living and tax burdens.

Ohio Tax Treatment of Retirement Income

Beyond Social Security, Ohio offers specific tax credits for retirees. Residents can claim a retirement income credit if their adjusted gross income is below certain thresholds. Furthermore, while some states tax all pension income, Ohio provides a graduated credit based on the amount of retirement income received. This financial buffer often allows Ohioans to retire 1-2 years earlier than they might in high-tax states like New York or California, as their “after-tax” purchasing power is higher.

Healthcare and the Medicare Bridge

Perhaps the biggest factor in determining retirement age is healthcare. Medicare eligibility begins at age 65. For those retiring in Ohio at age 60 via a pension or private savings, the cost of private health insurance for those five “gap years” can be astronomical. A savvy financial plan for an Ohio resident must include a dedicated Health Savings Account (HSA) or a cash reserve specifically to cover premiums until the age 65 Medicare milestone is reached.

Crafting Your Retirement Timeline: A Strategic Financial Framework

Ultimately, “what is the retirement age in Ohio” is a question that you answer through meticulous financial modeling. There is the age the law allows, and the age your balance sheet allows.

The 4% Rule and Inflation Hedging

To determine your personal retirement age, apply the 4% rule to your projected expenses in Ohio. If you plan to live on $60,000 a year, you generally need a portfolio of $1.5 million. However, given Ohio’s manufacturing-heavy economy and varying property tax rates (which can be high in suburban areas like Dublin or Upper Arlington), you must adjust your “age of exit” to account for local inflation. If your property taxes rise, your retirement age might need to shift back six months to ensure portfolio longevity.

Sequence of Returns Risk

The year you choose to retire is just as important as the age. “Sequence of returns risk” suggests that if the market dips in the first two years of your retirement, your portfolio may never recover. Therefore, the “safest” retirement age is one where you have at least 2–3 years of living expenses in liquid, low-risk vehicles (like Ohio municipal bonds or high-yield savings accounts) to avoid selling equities in a down market.

In conclusion, the retirement age in Ohio is a multifaceted concept. It is age 67 for full Social Security, age 59½ for penalty-free 401(k) access, and potentially as early as age 55 for public employees with decades of service. By aligning these legal milestones with a disciplined investment strategy and an understanding of Ohio’s tax advantages, you can move from asking “what is the retirement age” to declaring “this is my retirement age.”

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.