In the vast ecosystem of the financial world, banking is often perceived as a utility—a place to store a paycheck, pay bills, and perhaps secure a mortgage. However, for high-net-worth individuals (HNWIs) and families with significant capital, banking transcends these basic functions. This is the realm of private banking.

Private banking is not merely a service; it is a dedicated financial partnership designed to preserve, grow, and transition wealth across generations. It combines traditional banking services with sophisticated investment strategies, tax planning, and concierge-level attention. To understand what a private bank is, one must look beyond the teller window and into a world of bespoke financial engineering.

The Foundation of Private Banking

At its core, private banking is a suite of financial services provided by banks and other financial institutions to individuals who possess high levels of investable assets. While a standard retail bank focuses on the “mass market,” private banks cater to a refined segment of the population, offering a “white-glove” experience that prioritizes the client’s total financial health.

Defining the Private Banking Relationship

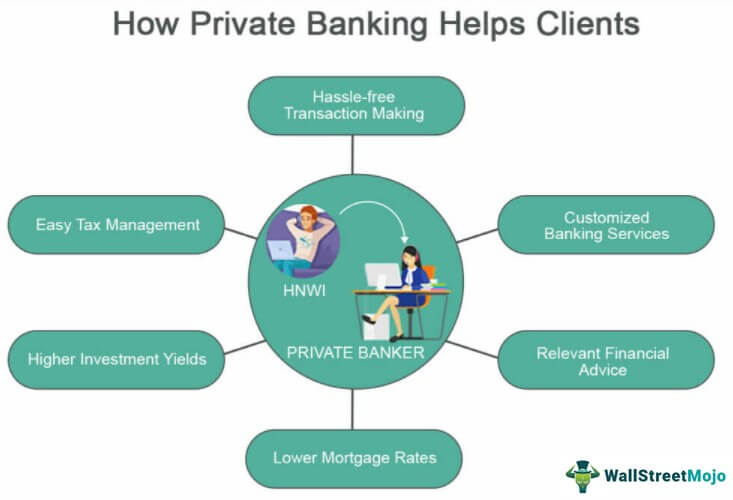

The hallmark of private banking is the relationship. Unlike retail banking, where a customer might interact with whichever representative is available at a branch or call center, private banking clients are assigned a dedicated Relationship Manager (RM). This individual acts as the single point of contact for all financial needs.

The RM’s role is to understand the client’s lifestyle, risk tolerance, and long-term aspirations. They coordinate with a team of specialists—including tax advisors, estate lawyers, and investment analysts—to ensure that every financial move is aligned with a master strategy. This holistic approach ensures that the client’s wealth is not just managed in silos but viewed as a unified engine for growth and legacy.

The Threshold: Who Qualifies for Private Banking?

Private banking is defined by its exclusivity. Because the level of service is so high and the resources allocated to each client are so significant, banks set specific entry requirements. These are usually measured in “investable assets”—cash or securities that can be managed by the bank, excluding primary residences or business equity.

While every institution has its own criteria, most entry-level private banking tiers begin at $1 million in investable assets. For “Ultra-High-Net-Worth” (UHNW) segments, the requirements can soar to $10 million, $50 million, or even $100 million. For those who do not yet meet these benchmarks but show a high income trajectory, many banks offer “Premier” or “Priority” banking as a bridge to full private services.

Core Services Offered by Private Banks

A private bank is more than just a place to hold money; it is an arsenal of financial tools. The services provided are designed to address the complexities that come with significant wealth—complexities that standard retail banks are simply not equipped to handle.

Bespoke Investment Management

Investment management is the engine room of private banking. Instead of choosing from a menu of standardized mutual funds, private banking clients receive customized portfolio management. This begins with a deep dive into the client’s risk profile and time horizon.

The bank’s investment team constructs portfolios that may include global equities, fixed income, and specialized currencies. Because of the size of the assets under management, private banks can often negotiate lower institutional fees on products, a benefit passed directly to the client. Furthermore, the bank provides active management, rebalancing portfolios in real-time to respond to global economic shifts, geopolitical events, or changes in the client’s personal circumstances.

Estate Planning and Wealth Transfer

For the wealthy, the goal is often not just to accumulate assets, but to ensure they reach the next generation with minimal friction. Private banks offer extensive estate planning services to navigate the labyrinth of inheritance taxes, gift taxes, and legal hurdles.

This involves the creation and management of trusts, the drafting of complex wills, and the establishment of family foundations. By integrating estate planning with daily banking, the private bank ensures that the client’s liquidity needs are met while simultaneously securing the future for their heirs. This “intergenerational wealth management” is a cornerstone of the private banking value proposition.

Specialized Credit and Lending Solutions

While most people think of loans as a burden, for the high-net-worth individual, credit is a strategic tool for liquidity. Private banks offer specialized lending products that are rarely available to the general public.

A common example is “Lombard Lending” or securities-backed lending. This allows a client to borrow money against their investment portfolio without having to sell their stocks or bonds. This provides immediate liquidity for a real estate purchase or a business venture while allowing the client’s investments to continue growing. Additionally, private banks provide custom financing for “luxury assets” such as private jets, yachts, and high-end art collections—assets that traditional mortgage lenders would find too risky or complex to value.

The Strategic Advantages of Private Banking

The reason individuals choose private banking over traditional wealth management firms often comes down to the unique strategic advantages provided by integrated banking institutions.

The Dedicated Relationship Manager

The value of a Relationship Manager cannot be overstated. In the world of high finance, time is the most valuable commodity. Having a single professional who understands your entire history—from your business’s cash flow needs to your children’s educational goals—streamlines decision-making.

The RM acts as a gatekeeper and an advocate. If a client needs a complex mortgage for an overseas property, the RM handles the internal negotiations with the credit department. if a client wants to engage in a new investment trend, such as ESG (Environmental, Social, and Governance) investing, the RM brings in the appropriate subject matter experts. This level of personalized service creates a frictionless financial life.

Privacy and Discretion in a Digital Age

The term “private” in private banking is literal. Discretion is a fundamental pillar of the industry. High-net-worth individuals often require a level of anonymity to protect themselves from fraud, solicitation, or public scrutiny.

Private banks have robust protocols to ensure that a client’s net worth, transaction history, and investment choices remain confidential. While modern regulations like “Know Your Customer” (KYC) and Anti-Money Laundering (AML) laws require transparency with regulators, the bank ensures that this information is shielded from the public eye, providing a secure environment for the management of significant capital.

Access to Alternative Investments

One of the biggest draws of private banking is access to “Alternative Investments” that are generally closed to the retail public. This includes Private Equity, Venture Capital, Hedge Funds, and Real Estate Investment Trusts (REITs) that require high minimum buy-ins.

Private banks often have their own internal private equity arms or partnerships with top-tier global funds. This allows clients to diversify their wealth beyond the volatility of the public stock market and participate in the growth of pre-IPO companies or large-scale infrastructure projects. These “alts” are essential for building a truly resilient, multi-asset class portfolio.

Comparing Private Banking vs. Premier and Retail Banking

It is easy to confuse different tiers of banking, but the distinctions are significant in terms of both cost and service depth.

Service Depth and Customization

Retail banking is a product-driven model. You are offered a credit card, a savings account, or a standard mortgage. Premier banking (often called Preferred Banking) is a service-driven model that offers better rates and shorter lines, but the products remain largely standardized.

Private banking is a solution-driven model. If a standard product doesn’t fit the client’s needs, the bank creates a new one. This might involve structuring a derivative to hedge against a specific currency risk or creating a custom lending facility for a niche business need. The ratio of clients to staff is also drastically different; while a retail branch might serve thousands, a private banker may only handle 30 to 50 families, ensuring a high level of attentiveness.

Fee Structures and Transparency

The cost of private banking is generally higher than retail banking, reflecting the specialized expertise involved. Fees are typically structured as a percentage of “Assets Under Management” (AUM), usually ranging from 0.5% to 1.5% annually.

While this may seem higher than a “free” checking account, it covers a wide array of services that would otherwise cost thousands in separate legal and accounting fees. Furthermore, the “all-in” nature of private banking fees often includes the cost of trades, financial planning, and concierge services, making it a comprehensive value package for those with complex needs.

Is Private Banking Right for Your Financial Future?

Deciding to move into private banking is a significant milestone in an individual’s financial journey. It marks the transition from “saving and spending” to “wealth optimization and legacy.”

Evaluating the Cost-to-Value Ratio

For those who meet the asset threshold, the primary question is whether the benefits outweigh the AUM fees. If your financial life is relatively simple—consisting perhaps of one house and a retirement account—the overhead of a private bank might not be necessary.

However, if you own multiple properties, have international business interests, are concerned about estate taxes, or want access to exclusive investment deals, the value provided by a private bank is immense. The tax savings and investment outperformance alone often more than cover the annual fees.

Transitioning from Retail to Private Wealth Management

As wealth grows, the complexity of managing it increases exponentially. Transitioning to a private bank is about reclaiming time and gaining peace of mind. By centralizing your financial affairs under one roof, you ensure that your investments, taxes, and estate plan are all pulling in the same direction.

When choosing a private bank, it is essential to look for a firm with a global footprint, a strong fiduciary reputation, and a culture that aligns with your personal values. Whether it is a storied European institution with centuries of history or a modern, tech-forward American bank, the right private banking partner will be the architect of your financial legacy, ensuring that your wealth serves your goals today and for generations to come.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.