In the world of personal and business finance, few numbers hold as much weight as the prime interest rate. Whether you are a first-time homebuyer looking at a line of credit, a small business owner seeking capital for expansion, or an individual managing credit card debt, the prime rate is a silent partner in your financial journey. It serves as the baseline for a vast array of lending products, dictating how much it costs to borrow money and, conversely, how much you can earn on your savings. Understanding what the prime interest rate is today and how it functions is essential for anyone looking to navigate the modern economy with confidence.

What is the Prime Interest Rate and How is it Determined?

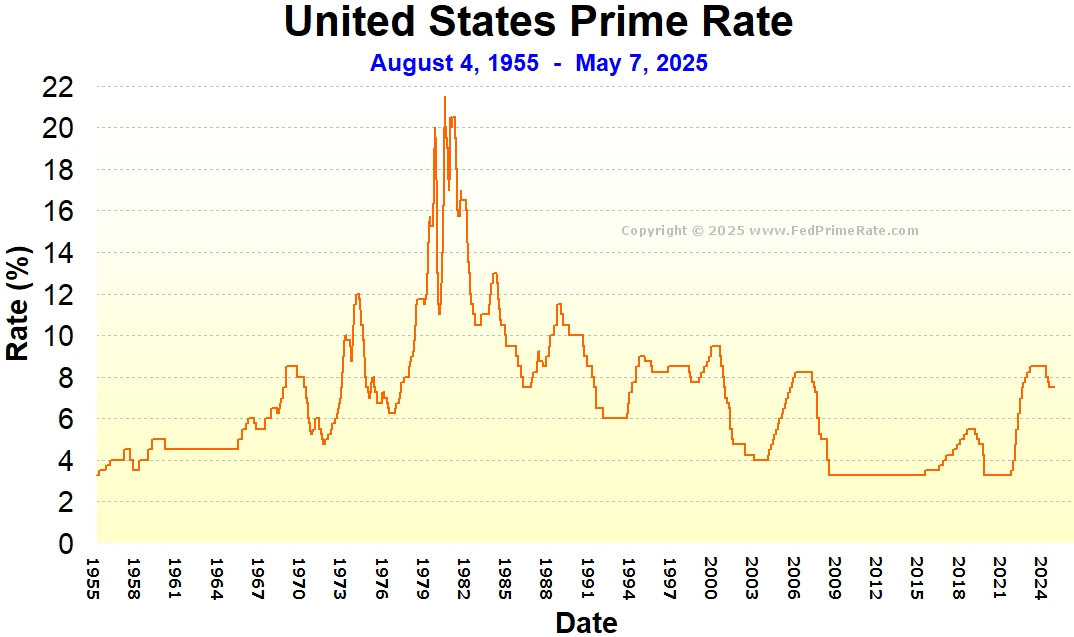

At its core, the prime interest rate—often referred to simply as “the prime”—is the interest rate that commercial banks charge their most creditworthy corporate customers. These are typically large companies with impeccable credit histories and stable balance sheets. While you may not be a Fortune 500 company, the prime rate matters to you because it serves as the foundational index for most consumer loan products.

The Relationship with the Federal Funds Rate

The prime rate does not exist in a vacuum. In the United States, it is directly tied to the federal funds rate, which is the interest rate set by the Federal Open Market Committee (FOMC) of the Federal Reserve. The federal funds rate is the rate at which banks lend to one another overnight to maintain their required reserves.

As a general rule of thumb, the prime rate is traditionally set at 3 percentage points above the federal funds rate. For example, if the Federal Reserve sets the target range for the federal funds rate at 5.25% to 5.50%, the prime rate will typically settle at 8.50%. When the Fed “raises rates” to combat inflation, the prime rate climbs almost instantaneously, making borrowing more expensive across the board.

The Role of the Wall Street Journal Prime Rate

While individual banks can technically set their own prime rates, the financial industry looks to the Wall Street Journal (WSJ) as the official record-keeper. The WSJ surveys the 30 largest banks in the United States and publishes a “consensus” prime rate. When at least 23 out of those 30 banks change their rate, the WSJ updates its published prime rate. This consistency ensures that the lending market remains stable and that consumers have a clear benchmark for their variable-rate loans.

Why the Prime Rate Matters to Your Personal Finances

For the average consumer, the prime rate is the engine behind variable-interest financial products. Unlike a 30-year fixed-rate mortgage, where your interest rate is locked in for the duration of the loan, variable-rate products fluctuate in tandem with the prime rate. Understanding this connection is vital for effective debt management and budgeting.

Impact on Credit Card APRs

The most direct impact of a shift in the prime rate is felt in your wallet via credit card interest. Most credit cards have a variable Annual Percentage Rate (APR) calculated as “Prime + Margin.” For instance, if your credit card agreement specifies a margin of 15% and the prime rate is 8.5%, your total APR is 23.5%.

When the prime rate increases, your credit card issuer typically adjusts your APR within one or two billing cycles. In a high-rate environment, carrying a balance becomes significantly more expensive, potentially leading to a “debt spiral” if the minimum payments only cover the interest rather than the principal.

HELOCs and Variable-Rate Mortgages

Home Equity Lines of Credit (HELOCs) are almost always tied to the prime rate. For homeowners using a HELOC to fund renovations or consolidate debt, a rising prime rate can lead to a sudden and sharp increase in monthly payments. Similarly, while less common today than in previous decades, Adjustable-Rate Mortgages (ARMs) often use the prime rate as an index after the initial fixed-period expires. For those holding these types of debt, monitoring the Federal Reserve’s meetings becomes a monthly necessity to anticipate changes in housing costs.

Auto Loans and Personal Lines of Credit

While many auto loans are fixed-rate, personal lines of credit and some private student loans are indexed to the prime rate. Even for fixed-rate products, the prime rate serves as an indirect influence. When the prime rate is high, banks must pay more to borrow money themselves, which means they will charge higher starting rates for new fixed-rate auto loans and personal loans to maintain their profit margins.

The Broader Economic Implications of Prime Rate Fluctuations

The prime rate is more than just a consumer metric; it is a primary tool for economic steering. The Federal Reserve manipulates interest rates to balance the dual mandate of maximum employment and stable prices (low inflation).

Inflation Control and the Federal Reserve’s Mandate

When inflation rises—meaning the cost of goods and services is increasing too quickly—the Federal Reserve raises interest rates to “cool down” the economy. By increasing the federal funds rate, and subsequently the prime rate, the cost of borrowing increases. This discourages businesses from taking out loans to expand and discourages consumers from spending on credit. As demand for goods and services drops, the pace of price increases typically slows down. Conversely, in a recession, the Fed lowers rates to make borrowing “cheap,” encouraging investment and spending to jumpstart the economy.

Business Borrowing and Economic Expansion

For the business world, the prime rate is the benchmark for commercial loans, small business lines of credit, and construction loans. Small to mid-sized enterprises (SMEs) are particularly sensitive to prime rate movements. High rates can lead to a slowdown in hiring and a reduction in capital expenditures. When the “cost of capital” is high, a project that seemed profitable at a 4% interest rate may no longer be viable at an 8.5% rate. This ripple effect can eventually impact the stock market, as lower corporate earnings forecasts lead to downward pressure on share prices.

Strategies to Navigate a High-Prime-Rate Environment

When the prime interest rate is high, the financial playbook changes. It shifts from a strategy of growth and leverage to one of preservation and strategic debt reduction.

Debt Consolidation and Refinancing Tactics

In a high-rate environment, the first priority should be tackling variable-rate debt. If you are carrying a balance on a credit card with a 24% APR, seeking a 0% intro-APR balance transfer card can provide a temporary reprieve (usually 12–21 months) to pay down the principal without interest accumulation. Additionally, individuals with high-interest personal lines of credit might consider consolidating that debt into a fixed-rate personal loan before rates climb even higher.

High-Yield Savings and Fixed-Income Opportunities

The “silver lining” of a high prime rate is that it usually correlates with higher yields on savings accounts and Certificates of Deposit (CDs). For a decade following the 2008 financial crisis, interest on savings was negligible. Today, however, high-yield savings accounts (HYSAs) and money market accounts often offer rates that track closely with the federal funds rate.

Investors can also look toward “laddering” CDs—buying CDs that mature at different intervals—to lock in high rates while maintaining some liquidity. This allows your “lazy money” to finally start working for you, providing a hedge against the increased costs of borrowing.

Looking Ahead: Future Projections for the Prime Interest Rate

Predicting the future of the prime rate requires keeping a close eye on economic indicators, primarily the Consumer Price Index (CPI) and employment data. The Federal Reserve meets eight times a year to decide the fate of interest rates, and their decisions are “data-dependent.”

Key Indicators to Watch

- The Core CPI: This measures inflation excluding volatile food and energy prices. If this number remains higher than the Fed’s 2% target, the prime rate is likely to stay “higher for longer.”

- Unemployment Claims: A “hot” labor market with low unemployment often gives the Fed more room to keep rates high to fight inflation. If unemployment begins to rise sharply, the Fed may be forced to cut rates to prevent a deep recession.

- Yield Curve Inversions: Financial analysts often look at the difference between short-term and long-term Treasury yields. An “inverted” curve has historically been a reliable, though not infallible, predictor of an upcoming recession, which eventually leads to lower prime rates.

Conclusion: Staying Proactive in a Changing Market

The prime interest rate today is a reflection of the complex tug-of-war between economic growth and inflation control. While a high prime rate presents challenges—particularly for those with significant variable-rate debt—it also offers opportunities for disciplined savers and strategic investors.

By understanding how the prime rate is calculated and identifying which of your financial products are tied to it, you can make informed decisions. Whether that means locking in a fixed rate, aggressively paying down credit card balances, or moving your emergency fund to a high-yield account, staying proactive ensures that you remain in control of your financial future, regardless of which way the Federal Reserve moves the needle. Finance is rarely static; those who monitor the prime rate are better equipped to weather the storms and capitalize on the sunshine of the economic cycle.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.