In the modern landscape of digital banking, the traditional binary of “checking” and “savings” is increasingly being replaced by more nuanced financial tools. One of the most prominent examples of this evolution is the PNC Virtual Wallet, a suite of accounts designed to help consumers manage their money with greater granularity. At the heart of this system is the PNC Reserve account.

While many banking customers are familiar with primary checking accounts for daily expenses and savings accounts for long-term goals, the Reserve account occupies a unique middle ground. It is specifically designed to act as a secondary checking account that earns interest, serving as a tactical buffer for short-term planning and overdraft protection. This article explores the mechanics of the PNC Reserve account, how it fits into the broader Virtual Wallet ecosystem, and how you can leverage it to improve your financial health.

Understanding the PNC Virtual Wallet Ecosystem

To understand the Reserve account, one must first understand the “Virtual Wallet” concept. PNC Bank introduced the Virtual Wallet to move away from fragmented account management. Instead of seeing your money as a single lump sum or two separate buckets, the Virtual Wallet organizes your finances into three distinct roles.

The Triple-Account Strategy: Spend, Reserve, and Growth

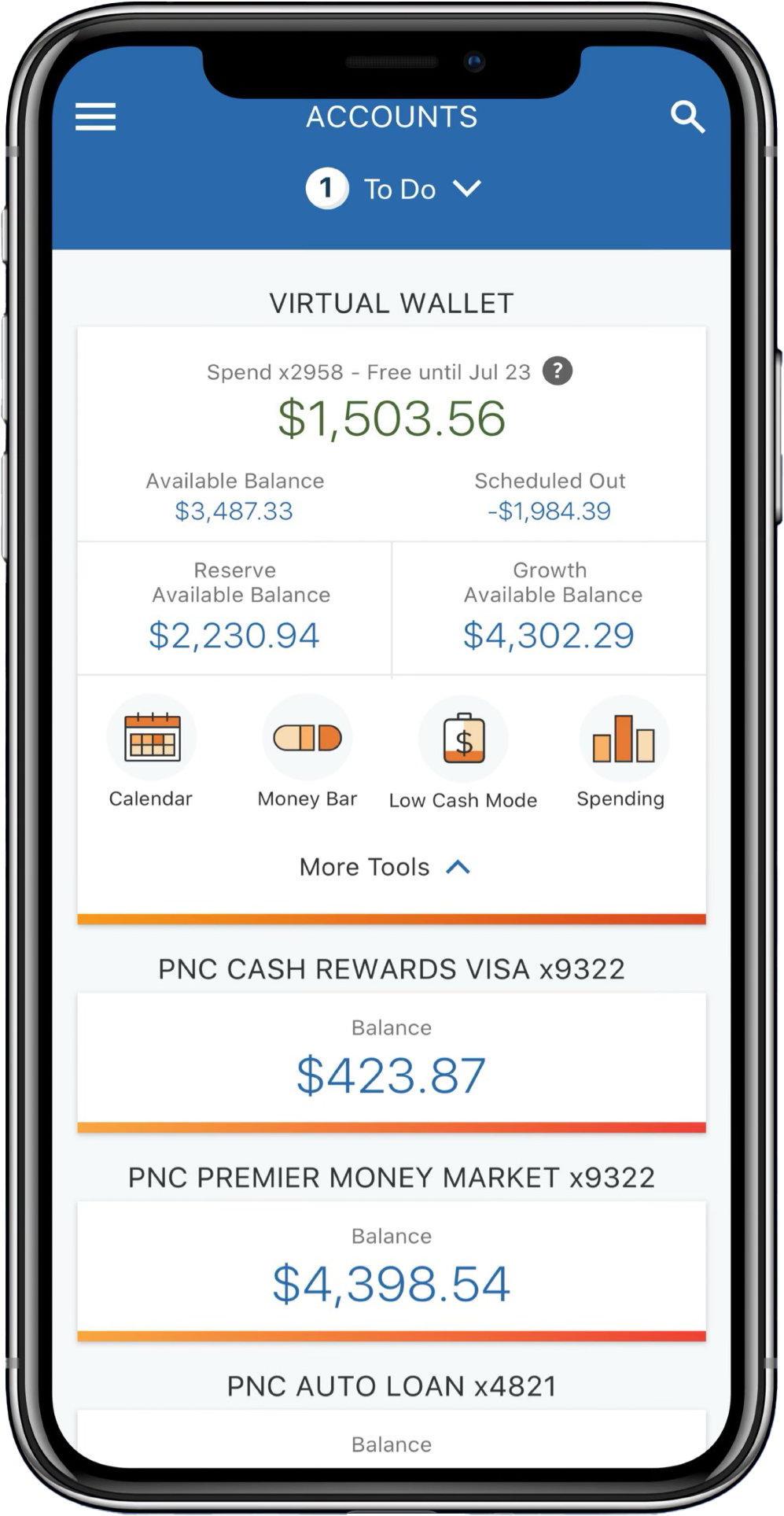

The Virtual Wallet consists of three interconnected accounts:

- Spend Account: This is your primary checking account. It is where your direct deposit lands and where you pay your monthly bills, use your debit card, and handle everyday transactions.

- Reserve Account: This is a secondary checking account. It is intended for money you plan to spend in the near future but not today. It is often referred to as a “holding pen” for upcoming expenses or a dedicated space for short-term savings goals.

- Growth Account: This is a long-term savings account. It typically offers the highest interest rate among the three and is intended for money you don’t plan to touch for months or years, such as an emergency fund or a down payment on a home.

How the Reserve Account Bridges the Gap

The Reserve account acts as the connective tissue between your immediate liquidity and your long-term wealth. In a traditional banking setup, if you leave all your bill money in your primary checking, it’s easy to overspend and accidentally use funds meant for the rent or mortgage. Conversely, if you move that money into a separate savings account, it may be subject to federal transaction limits (like Regulation D) or may not be instantly accessible for bill pay.

The Reserve account solves this by being a “checking” account by classification but a “savings” account by intent. It allows you to set aside money for next month’s car insurance or an upcoming vacation without losing the ability to move that money back to “Spend” instantly or use it as a safety net for unexpected charges.

Key Features and Benefits of the PNC Reserve Account

The Reserve account is more than just a placeholder; it comes with specific functional benefits designed to prevent financial stress. For users who struggle with budgeting, these features provide a structured environment that encourages better habits.

Interest Rates and Earning Potential

Unlike many standard checking accounts that offer zero interest, the PNC Reserve account is an interest-bearing account. While the rates are typically lower than what you might find in a dedicated High-Yield Savings Account (HYSA) or the PNC “Growth” account, it still allows your short-term “holding” money to grow.

This feature is particularly beneficial for those who keep a significant “buffer” in their accounts. Instead of that money sitting idle in a “Spend” account, moving it to “Reserve” allows it to accrue interest until the moment it is needed to cover a scheduled expense.

Overdraft Protection and the “Overdraft Shield”

One of the most significant advantages of the Reserve account is its role in PNC’s Overdraft Shield. Financial institutions often charge hefty fees when a customer’s primary checking account hits a negative balance. With the Virtual Wallet, the Reserve account acts as the first line of defense.

If a transaction exceeds the balance in your “Spend” account, PNC can automatically transfer funds from your “Reserve” account to cover the difference. Because both accounts are part of the same Virtual Wallet, these transfers are typically seamless and can save users from the cascading costs of overdraft fees. This automated safety net provides peace of mind for those with fluctuating monthly expenses.

Budgeting Tools: The Calendar and Wish List

The Reserve account integrates with PNC’s proprietary digital tools, such as the “Calendar” and “Wish List.” The Calendar view allows you to see upcoming “Reserve” items—money you have earmarked for specific dates. This visual representation of cash flow helps users avoid the “illusion of wealth” that occurs when a high checking balance masks upcoming financial obligations.

The “Wish List” feature allows you to set specific goals within your Reserve account. For example, if you are saving $500 for a new laptop, you can track your progress specifically within the Reserve bucket. This psychological separation helps users stay disciplined, as they can see exactly how much “free” money they have versus how much is committed to their goals.

How to Maximize the Use of Your Reserve Account

Simply having a Reserve account isn’t enough; to truly benefit from it, you must integrate it into a comprehensive personal finance strategy. Wealth management is often about the systems we put in place rather than the amount of money we earn.

Planning for Non-Monthly Expenses

Most people are good at budgeting for monthly bills like rent or Netflix subscriptions. However, “sinking funds”—expenses that occur quarterly or annually, such as car registration, holiday gifts, or semi-annual insurance premiums—often cause financial crises.

The Reserve account is the perfect home for these sinking funds. By calculating the annual cost of these items and dividing by 12, you can transfer a set amount into your Reserve account every month. When the bill finally arrives, the money is already set aside, earning interest, and safely out of reach of your daily debit card swipes.

Automating Your Savings Transfers

The most successful savers are those who remove the element of human choice from the equation. PNC allows for automated transfers between the Spend, Reserve, and Growth accounts. A professional financial strategy involves setting an automated transfer from your “Spend” to your “Reserve” account every payday.

By treating your Reserve contribution as a “bill” you pay to yourself, you ensure that your short-term goals are funded before you have the chance to spend that money on discretionary items. This “pay yourself first” mentality is a cornerstone of building long-term financial security.

Using the Reserve Account as an Emergency Buffer

While the “Growth” account should hold your 3-6 month emergency fund, the “Reserve” account is ideal for “minor emergencies.” This includes things like a flat tire, a broken kitchen appliance, or a last-minute doctor’s visit. Keeping $500 to $1,000 in your Reserve account ensures that these minor inconveniences don’t force you to dip into your long-term savings or, worse, carry a balance on a high-interest credit card.

Fees, Requirements, and Limitations

While the PNC Reserve account offers numerous benefits, it is essential to understand the terms of service and potential costs associated with the Virtual Wallet. Professional financial management requires a keen eye for the “fine print” to ensure that fees don’t erode your savings.

Minimum Balance and Monthly Service Charges

PNC typically offers several tiers of Virtual Wallet accounts, such as the standard Virtual Wallet, Virtual Wallet with Performance Spend, and Virtual Wallet with Performance Select. Each tier has different requirements to waive the monthly service fee.

Common ways to waive the fee include:

- Maintaining a certain combined average daily balance across the Spend and Reserve accounts.

- Having a qualifying monthly direct deposit (such as your paycheck) credited to the Spend account.

- Being a student (PNC often waives fees for a set period for active students).

Failure to meet these requirements can lead to a monthly maintenance fee, which can quickly negate any interest earned in the Reserve account.

Transaction Limits and Accessibility

While the Reserve account is a checking account, it is important to remember its purpose. It is designed for transfers to the Spend account or for specific bill payments. Unlike the Spend account, you generally do not receive a separate debit card for your Reserve account. Its primary utility is digital.

Furthermore, while the 2020 suspension of Federal Regulation D has made savings account transfers more flexible, banks still reserve the right to monitor account activity. The Reserve account is built for liquidity, but using it as a high-volume transactional account may defeat its purpose as a budgeting tool.

Is the PNC Reserve Account Right for Your Financial Goals?

When evaluating whether the PNC Reserve account fits into your financial life, it is helpful to compare it against more traditional banking structures.

Comparison with Traditional Savings Accounts

A traditional savings account is often “out of sight, out of mind.” For many, this is a good thing. However, the friction required to move money from a traditional savings account to a checking account can sometimes lead to overdrafts if a bill hits unexpectedly.

The PNC Reserve account offers less friction. Because it is part of the “Virtual Wallet” dashboard, you have a holistic view of your money. If you value integration and technological tools that help you visualize your budget, the Reserve account is superior to a standalone savings account at a different bank. However, if you are looking for the absolute highest interest rate available in the market, a specialized online-only High-Yield Savings Account will likely outperform the PNC Reserve and Growth accounts.

The Verdict: Best Use Cases

The PNC Reserve account is an excellent tool for:

- The “Visual” Budgeter: People who want to see their money categorized by purpose rather than just a total balance.

- The Overdraft-Prone: Individuals who want an automated safety net to avoid expensive bank fees.

- The Short-Term Planner: Those saving for goals 3–12 months away.

In conclusion, the PNC Reserve account is a sophisticated financial instrument that encourages proactive money management. By acting as a buffer between daily spending and long-term saving, it provides the structure necessary to maintain a balanced budget. When used correctly—by automating transfers and utilizing the Overdraft Shield—it becomes more than just an account; it becomes a cornerstone of a healthy, modern financial strategy.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.