A paycheck stub, also known as a payslip or earnings statement, is a crucial document that accompanies every salary payment you receive. While its primary function is to detail your income and deductions, it serves as far more than just a receipt. In the complex world of personal finance and employment, understanding your paycheck stub is fundamental to managing your money effectively, ensuring accurate compensation, and navigating your financial future. This guide will demystify the paycheck stub, breaking down its components, highlighting its importance, and exploring how it intersects with broader themes in technology, branding, and money management.

![]()

Decoding the Components of Your Paycheck Stub

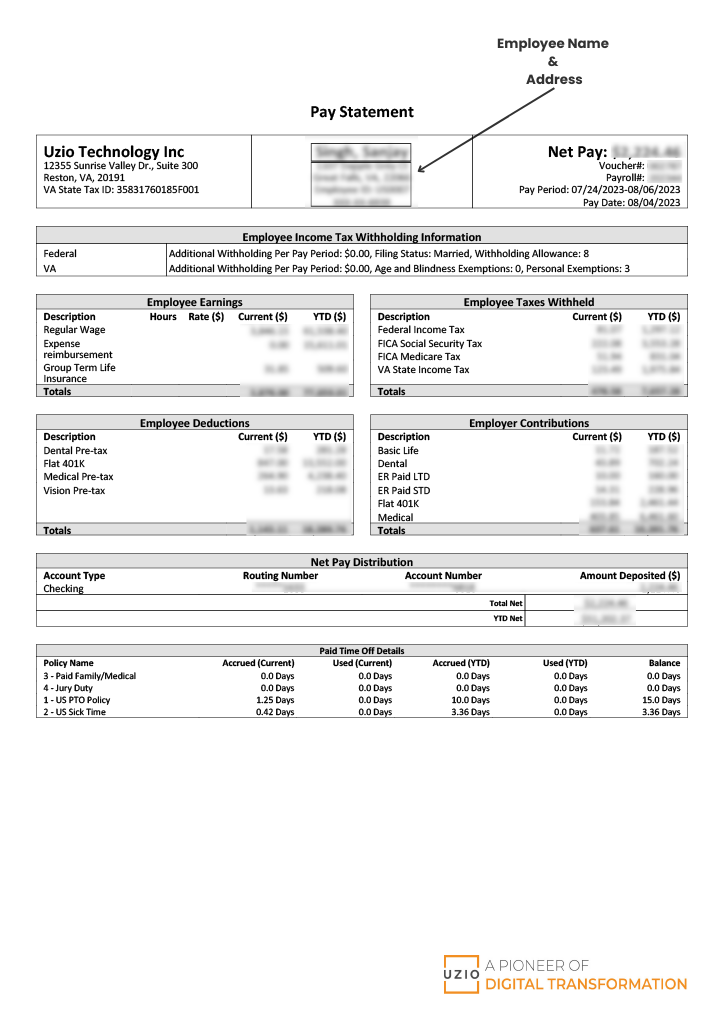

At its core, a paycheck stub is a standardized report that breaks down your gross pay, deductions, and net pay. While formats can vary slightly between employers and payroll systems, several key pieces of information are consistently present. Understanding these elements empowers you to verify your pay and identify any discrepancies.

Gross Pay: The Starting Point

Gross pay is the total amount of money you earn before any deductions are taken out. This is the figure that reflects your hourly wage multiplied by the hours worked, or your fixed salary for the pay period.

- Hourly Employees: For those paid hourly, gross pay is calculated by multiplying your hourly rate by the number of hours you worked during that pay period. Overtime pay, often calculated at a higher rate (e.g., 1.5 times your regular rate), will also be included here if applicable.

- Salaried Employees: Salaried employees receive a fixed amount of pay for a set period, regardless of the exact hours worked. Their gross pay for the pay period is typically a fraction of their annual salary.

- Bonuses and Commissions: Any additional payments, such as performance bonuses, sales commissions, or other incentives, will also contribute to your gross pay for the period. These are crucial to track as they can significantly impact your overall earnings.

It’s important to note that gross pay is not the amount that will land in your bank account. It’s simply the foundation upon which your net pay is calculated.

Deductions: What Comes Out of Your Gross Pay

Deductions are the amounts subtracted from your gross pay. These can be mandatory (required by law or contract) or voluntary (chosen by you). Understanding these deductions is vital for managing your finances and comprehending where your money is going.

Mandatory Deductions

These are the deductions that are legally required or mandated by your employment agreement.

- Federal, State, and Local Income Taxes: This is usually the largest deduction. The amount withheld depends on your W-4 form (in the U.S.), which specifies your filing status and the number of dependents you claim. These taxes are paid to the government on your behalf.

- Social Security and Medicare Taxes (FICA in the U.S.): These taxes fund social insurance programs. Social Security provides retirement, disability, and survivor benefits, while Medicare funds the federal health insurance program for seniors and certain disabled individuals.

- Garnishment Orders: In some cases, a portion of your wages may be legally withheld to satisfy debts, such as child support, alimony, or outstanding loans. These are typically court-ordered.

Voluntary Deductions

These are deductions that you opt into, often for benefits or savings.

- Health Insurance Premiums: If your employer offers health insurance, your portion of the premium will likely be deducted from your paycheck.

- Retirement Contributions (e.g., 401(k), IRA): Contributions to employer-sponsored retirement plans are a common voluntary deduction. These pre-tax contributions reduce your taxable income, offering immediate tax benefits and building your long-term financial security.

- Other Benefits: This can include deductions for dental insurance, vision insurance, life insurance, disability insurance, flexible spending accounts (FSAs), or health savings accounts (HSAs).

- Union Dues: If you are part of a union, your membership dues will typically be deducted.

- Company Stock Purchase Plans: Some companies offer plans that allow employees to purchase company stock at a discounted price through payroll deductions.

The breakdown of these deductions is critical. It allows you to see how much is being contributed to your retirement, what your health insurance is costing you, and the actual tax burden you are facing.

Net Pay: The Amount You Actually Receive

Net pay, often referred to as take-home pay, is the amount of money remaining after all deductions have been subtracted from your gross pay. This is the figure that will be directly deposited into your bank account or issued to you as a physical check.

Gross Pay – Total Deductions = Net Pay

It’s essential to understand your net pay. This is the actual spendable income you have for the pay period. All your budgeting, saving, and spending decisions will be based on this figure.

The Importance of Your Paycheck Stub in Personal Finance

Beyond simply confirming your income, your paycheck stub is a powerful tool for financial management, informed decision-making, and safeguarding your rights as an employee. Its implications extend across various facets of personal and business finance.

1. Verifying Your Earnings and Accuracy

The most immediate importance of a paycheck stub is to verify that you have been paid correctly. It allows you to:

- Check Hours Worked and Pay Rate: For hourly employees, this means ensuring that all hours worked, including overtime, have been accurately recorded and compensated.

- Confirm Salary/Wage: For salaried employees, it confirms that the correct salary amount has been processed for the pay period.

- Track Bonuses and Commissions: Verify that any agreed-upon bonuses or commissions have been included.

- Identify Errors: Mistakes can happen. A paycheck stub helps you quickly identify any discrepancies in your pay, such as incorrect deductions or an incorrect gross pay amount. Promptly addressing these errors with your employer’s HR or payroll department can prevent larger issues down the line.

2. Understanding Your Tax Obligations

Your paycheck stub provides a clear picture of how much tax is being withheld from your earnings. This information is crucial for:

- Tax Planning: By reviewing your withholdings, you can assess if you are having too much or too little tax withheld. If you are consistently overpaying, you might consider adjusting your W-4 to receive more take-home pay throughout the year. Conversely, if you are underpaying, you could face a significant tax bill at the end of the year.

- Filing Taxes: While not a substitute for tax forms, your paycheck stubs are valuable during tax season. They provide a running tally of your income and tax payments, simplifying the process of filling out your tax returns.

3. Managing Benefits and Deductions

The detailed breakdown of deductions on your paycheck stub offers insights into your employee benefits and their costs.

- Retirement Planning: Seeing your 401(k) or other retirement contributions helps you track your progress towards your long-term financial goals. It also reminds you of the tax advantages of these contributions, as they are often deducted pre-tax.

- Healthcare Costs: Understanding the exact amount you are paying for health insurance premiums allows you to evaluate the value you are receiving and compare it with other options if available.

- Budgeting: Knowing your net pay is the foundation of any realistic budget. It tells you exactly how much money you have available for rent, groceries, debt payments, entertainment, and savings.

4. Proof of Income for Financial Applications

A paycheck stub is often required as proof of income when applying for loans, mortgages, rental agreements, or even certain credit cards. Lenders and landlords need to verify your ability to meet financial obligations. The consistency and detail on a paycheck stub provide credible evidence of your employment and earnings.

The Interplay of Paycheck Stubs with Technology, Branding, and Money Management

The seemingly simple paycheck stub is increasingly influenced by and integrated with broader trends in technology, branding, and personal finance.

Technology and the Evolution of Paycheck Stubs

The digital revolution has transformed how paycheck stubs are generated, delivered, and accessed.

- Digital Payslips: Many companies now issue electronic pay stubs, accessible through an employee portal or via email. This offers several advantages:

- Environmental Friendliness: Reduces paper waste.

- Convenience: Employees can access their stubs anytime, anywhere, without waiting for a physical copy.

- Enhanced Security: Secure online portals can offer better protection against loss or theft compared to paper copies.

- Integration with Financial Apps: Digital stubs can often be linked to personal finance management (PFM) apps, allowing for automatic categorization of income and expenses.

- Payroll Software and AI: Sophisticated payroll software, often powered by Artificial Intelligence (AI), is automating payroll processing, improving accuracy, and reducing human error. AI tools can also help analyze payroll data to identify trends, optimize staffing, and forecast labor costs for businesses.

- Mobile Access: Many employers provide mobile apps that allow employees to view their pay stubs, track hours, and even request time off directly from their smartphones.

Branding and the Employee Experience

While not as direct as marketing a product, the way an employer presents and handles employee compensation, including the paycheck stub, contributes to their brand.

- Employer Branding: A clear, accurate, and easy-to-understand paycheck stub reflects positively on an employer’s professionalism and transparency. A poorly managed payroll system or confusing payslips can negatively impact employee morale and the company’s reputation as an employer.

- Employee Communication: The paycheck stub serves as a tangible piece of communication from the employer to the employee. Clear formatting, helpful annotations, and easy access demonstrate a commitment to supporting their workforce.

- Personal Branding for Freelancers and Gig Workers: For individuals operating as freelancers or in the gig economy, their invoices and payment statements (which function similarly to paycheck stubs) are a critical part of their professional brand. Accurate invoicing, clear payment terms, and timely receipts build trust and encourage repeat business.

Money Management and Financial Literacy

The paycheck stub is a cornerstone of sound money management.

- Budgeting and Financial Planning: As discussed, the net pay figure is the starting point for all personal budgets. Understanding deductions allows for informed decisions about retirement savings, insurance choices, and overall financial health.

- Investing: Knowing your regular income and tax situation, as revealed by your paycheck stub, is crucial for making informed investment decisions. It helps determine how much disposable income you have available to invest and what tax implications your investments might have.

- Side Hustles and Online Income: For those pursuing side hustles or online income streams, understanding how these earnings are taxed and tracked is vital. While not traditional “paycheck stubs,” the records of income and expenses for these ventures are equally important for financial management.

- Financial Tools: Numerous financial apps and software tools can help you analyze your paycheck stub, track your spending, and build a budget based on your net income. These tools leverage the data from your payslips to provide actionable insights.

Frequently Asked Questions About Paycheck Stubs

Q1: What is the difference between gross pay and net pay?

Gross pay is your total earnings before any deductions. Net pay is your take-home pay after all deductions have been subtracted.

Q2: How often should I receive a paycheck stub?

You should receive a paycheck stub every time you are paid, whether that’s weekly, bi-weekly, semi-monthly, or monthly.

Q3: What should I do if I find an error on my paycheck stub?

Contact your employer’s Human Resources or Payroll department immediately to report the discrepancy. Be prepared to provide your paycheck stub and relevant details.

Q4: Can I keep my old paycheck stubs?

Yes, it’s highly recommended to keep your paycheck stubs for at least several years (e.g., 3-7 years) for tax purposes and as proof of income. Many employers provide digital access for a limited time, so it’s wise to download and save them.

Q5: How do taxes get calculated on my paycheck?

Taxes are calculated based on your gross pay, your filing status, and the number of allowances you claim on your W-4 form (in the U.S.). This information is used by payroll software to determine the amount of federal, state, and local income tax to withhold.

Conclusion

The paycheck stub is an indispensable document in the life of any employed individual. It’s more than just a record of payment; it’s a gateway to understanding your financial standing, managing your money effectively, and making informed decisions about your future. By familiarizing yourself with its components, recognizing its importance, and appreciating its connection to evolving technologies and financial literacy, you can transform this often-overlooked document into a powerful tool for achieving your personal and financial goals. In an era where technology is streamlining processes and financial awareness is paramount, mastering the paycheck stub is a fundamental step towards financial empowerment.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.