In the modern financial landscape, few tickers command as much attention as NVDA. When investors ask, “What is Nvidia stock at?” they are rarely looking for a simple price quote. Instead, they are inquiring about the health of the broader technology sector, the momentum of the artificial intelligence (AI) revolution, and the current state of market liquidity. Nvidia has transitioned from a niche hardware manufacturer for gamers into a global economic powerhouse, often acting as a bellwether for the S&P 500 and the Nasdaq-100.

Understanding Nvidia’s stock price requires a multi-faceted approach that goes beyond the daily fluctuations on the exchange. It involves analyzing market capitalization, price-to-earnings (P/E) ratios, and the institutional sentiment that drives trillions of dollars in trade volume. To truly grasp where Nvidia stands today, one must look at the intersection of supply chain economics, massive enterprise spending, and the fiscal discipline that has allowed the company to maintain industry-leading margins.

Understanding Nvidia’s Current Market Positioning

To answer the question of where Nvidia’s stock is currently situated, we must first look at its ascent into the exclusive “Trillion Dollar Club.” Nvidia’s valuation is not merely a reflection of past success but a massive bet by the global market on the future of computation. As of recent fiscal reporting, Nvidia’s market capitalization has rivaled that of tech giants like Apple and Microsoft, making it one of the most influential components of passive index funds and retirement portfolios worldwide.

Real-Time Valuation Metrics and Market Cap

When evaluating where the stock is “at,” the market capitalization is the most telling figure. It represents the total dollar market value of a company’s outstanding shares of stock. For Nvidia, this figure has seen unprecedented growth, often swinging by billions of dollars in a single trading session. Investors monitor the “support” and “resistance” levels—technical terms for the price points where the stock historically struggles to fall below or rise above.

Beyond the raw share price, institutional investors look at the “Free Cash Flow” (FCF). Nvidia’s ability to generate cash while maintaining high capital expenditures for research and development is a key reason the stock maintains its premium pricing. When the stock price reaches new all-time highs, it is often because the company has exceeded “whisper numbers”—the unofficial earnings expectations held by top-tier Wall Street analysts.

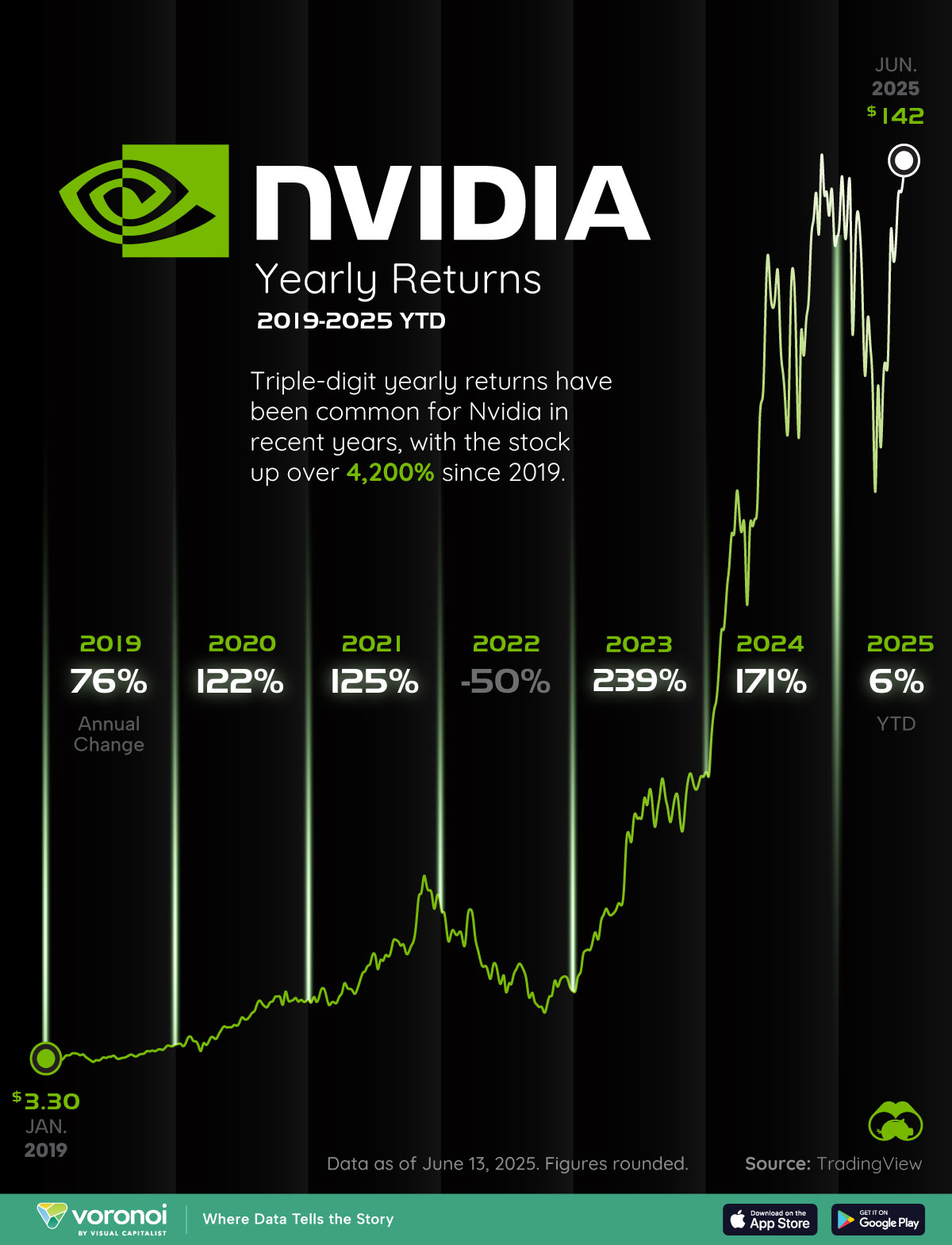

Historical Context: The Meteoric Rise

To understand the current price, one must look at the trajectory. Over the last decade, Nvidia has undergone several stock splits to keep its shares accessible to retail investors. Each split historically signals management’s confidence in continued upward momentum. The shift from the $100 billion valuation mark to the $2 trillion mark occurred with a velocity rarely seen in financial history. This rise was fueled by the transition from General Purpose Computing to Accelerated Computing, a shift that Nvidia effectively monopolized.

The Financial Drivers Behind the Stock Price

Nvidia’s stock price is fundamentally anchored to its earnings reports. In the world of high-growth investing, “revenue surprises” and “forward guidance” are the two engines that move the needle. Unlike many “dot-com” era companies that traded on hype alone, Nvidia’s stock price is backed by a massive surge in net income.

Data Center Dominance and Revenue Growth

The primary driver of Nvidia’s current stock valuation is its Data Center division. This segment provides the H100 and Blackwell architecture chips that power large language models (LLMs) like ChatGPT and Gemini. When tech giants—often referred to as “Hyperscalers”—announce increased capital expenditure budgets, Nvidia’s stock often reacts positively. This is because a significant portion of that budget is destined for Nvidia’s coffers.

The revenue growth in the Data Center segment has been described by many financial analysts as “parabolic.” For an investor, the sustainability of this growth is the most important factor in determining if the current stock price is a bargain or an overextension. As long as the Return on Investment (ROI) for AI remains high for Nvidia’s customers, the demand for their hardware—and by extension, the demand for their stock—remains robust.

Margin Analysis and Profitability

One of the most impressive aspects of Nvidia’s financial health is its gross margins. In many hardware industries, competition drives prices down, leading to “margin compression.” However, Nvidia has maintained gross margins that exceed 70%, a figure usually reserved for software companies with zero marginal costs. This level of profitability provides a “cushion” for the stock price; even if revenue growth slows down, the sheer efficiency of the business model ensures high earnings per share (EPS).

Valuation Analysis: Is the Premium Justified?

A common debate in the “Money” niche is whether Nvidia is overvalued. When a stock climbs as rapidly as Nvidia has, it naturally invites comparisons to historical bubbles. However, a deep dive into the valuation metrics suggests a more nuanced story.

P/E Ratios and Forward Earnings

The Price-to-Earnings (P/E) ratio is the standard tool for measuring whether a stock is expensive. While Nvidia’s trailing P/E (based on past profits) often looks high, its forward P/E (based on projected future profits) frequently appears more reasonable. This is because Nvidia’s earnings have often grown faster than its stock price.

Investors also utilize the PEG ratio (Price/Earnings to Growth). If a company has a P/E of 30 but is growing at 40% per year, its PEG ratio is less than 1.0, which many value investors consider an indicator of an undervalued stock. Nvidia often finds itself in this paradoxical position: looking expensive on the surface while appearing fundamentally sound when adjusted for growth projections.

Comparing Nvidia to the “Magnificent Seven”

Nvidia does not exist in a vacuum; it is part of the “Magnificent Seven”—a group of high-performing tech stocks that include Meta, Amazon, and Alphabet. When analyzing where Nvidia’s stock is at, professional traders compare its performance relative to its peers. If the rest of the tech sector is flat but Nvidia is rising, it indicates a “flight to quality,” where investors move capital into the most profitable and dominant player in a specific niche.

Risk Factors and Market Volatility

No investment is without risk, and Nvidia’s high valuation makes it susceptible to significant “drawdowns” or price corrections. Investors must be aware of the external factors that could influence the stock price negatively, regardless of the company’s internal performance.

Supply Chain Constraints and Geopolitical Risks

Nvidia is a “fabless” semiconductor company, meaning it designs its chips but relies on partners like TSMC (Taiwan Semiconductor Manufacturing Company) for fabrication. Any geopolitical tension in the Taiwan Strait or disruptions in the global supply chain can lead to immediate volatility in Nvidia’s stock price. Furthermore, U.S. export controls on high-end AI chips to certain regions represent a “headwind” that investors must factor into their long-term valuation models.

Competition and Market Saturation

While Nvidia currently holds a dominant market share in AI training chips, competition is mounting. Traditional rivals like AMD and Intel, as well as custom silicon developed in-house by companies like Amazon (Trainium) and Google (TPU), aim to chip away at Nvidia’s moat. If these competitors successfully offer a better “performance-per-dollar” ratio, Nvidia may be forced to lower its prices, which would impact the margins that currently support its high stock price.

Long-Term Outlook for Investors

For the individual investor, knowing “what the stock is at” today is less important than knowing where it will be in five to ten years. Investing in Nvidia is essentially a play on the continued digitalization of the global economy.

The Dividend vs. Growth Debate

Nvidia pays a small dividend, but it is primarily classified as a “growth stock.” Most of the value returned to shareholders comes through capital appreciation rather than quarterly payouts. For those focused on “Online Income” or “Side Hustles,” Nvidia represents a vehicle for long-term wealth accumulation rather than immediate cash flow.

Strategic investors often use “Dollar-Cost Averaging” (DCA) to build a position in Nvidia. By investing a fixed amount of money at regular intervals, they mitigate the risk of buying at a temporary “peak” and benefit from the stock’s long-term upward trend.

Conclusion: Strategic Allocation in a Tech-Driven Portfolio

In conclusion, Nvidia stock is currently at a crossroads of extreme growth and high expectations. It is no longer just a “tech stock”; it is a foundational asset for the modern financial era. Whether you are a retail investor looking at your first share or a seasoned portfolio manager, understanding Nvidia requires looking beyond the daily price ticker. It requires an analysis of earnings quality, a respect for market volatility, and an understanding of the pivotal role that accelerated computing plays in the global economy. As AI continues to integrate into every sector from healthcare to finance, Nvidia’s financial narrative will remain one of the most important stories in the world of money and investing.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.