In the world of corporate finance and personal investing, the term “Net Income” is often hailed as the holy grail of performance. Frequently referred to as the “bottom line,” it serves as the ultimate indicator of a company’s profitability over a specific period. However, a common point of confusion for many business owners and novice investors is how this figure—traditionally associated with the Income Statement—interacts with the Balance Sheet.

Understanding the relationship between net income and the balance sheet is fundamental to grasping the “double-entry” accounting system. While net income measures the wealth generated during a quarter or a year, the balance sheet records where that wealth goes. To master business finance, one must look beyond the simple profit figure and understand how net income transforms into equity, fueling future growth and stabilizing the company’s financial position.

The Conceptual Bridge: Where Net Income Meets the Balance Sheet

At first glance, the Income Statement and the Balance Sheet seem like two different languages. The Income Statement is a motion picture, showing the flow of money over time. In contrast, the Balance Sheet is a still photograph, capturing a company’s financial health at one specific moment. The bridge between these two documents is Net Income.

The Flow of Profits into Equity

Net income does not simply vanish once the fiscal year ends. Instead, it “flows” into the equity section of the balance sheet. When a company earns a profit, that profit belongs to the owners (shareholders). If the company chooses not to distribute all those profits as dividends, the remaining amount is rolled into the Balance Sheet under a specific line item. This process ensures that the fundamental accounting equation—Assets = Liabilities + Equity—remains in perfect balance.

Retained Earnings Explained

The specific landing spot for net income on the balance sheet is known as Retained Earnings. Retained earnings represent the cumulative net income of a company since its inception, minus any dividends paid out to shareholders. Each time a company reports a positive net income, its retained earnings (and thus its total equity) increase. Conversely, if a company reports a net loss, it must subtract that amount from its retained earnings, potentially leading to “accumulated deficits” if losses persist over many years.

Deconstructing the “Bottom Line”: How Net Income is Derived

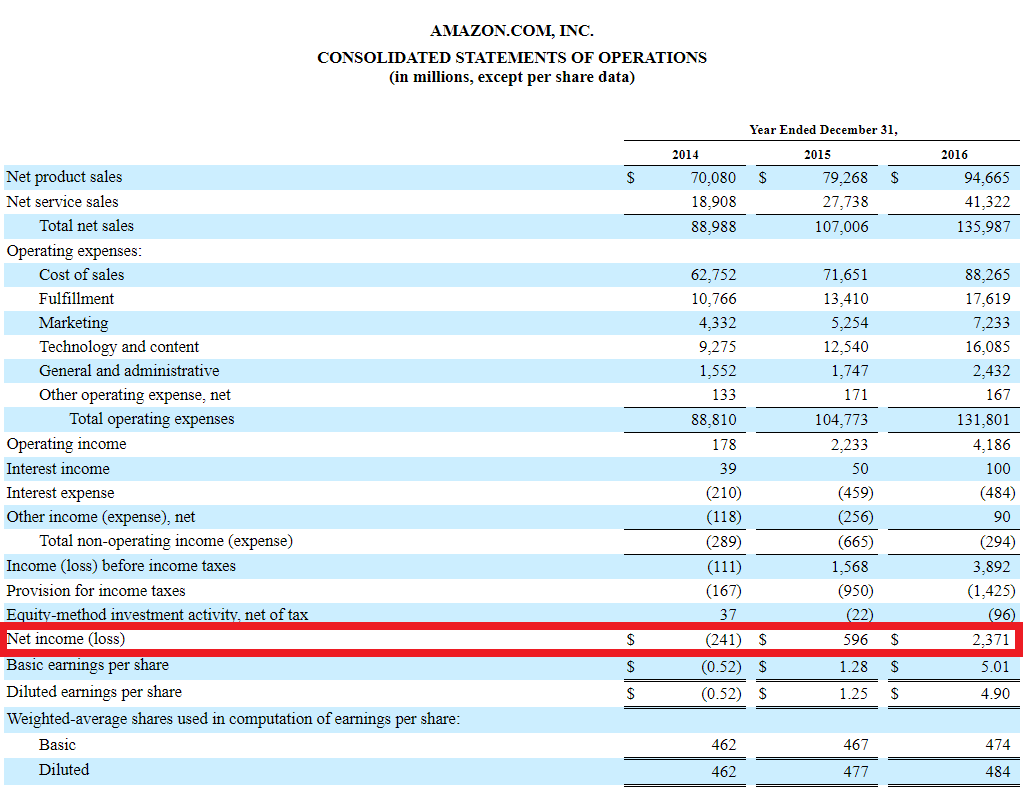

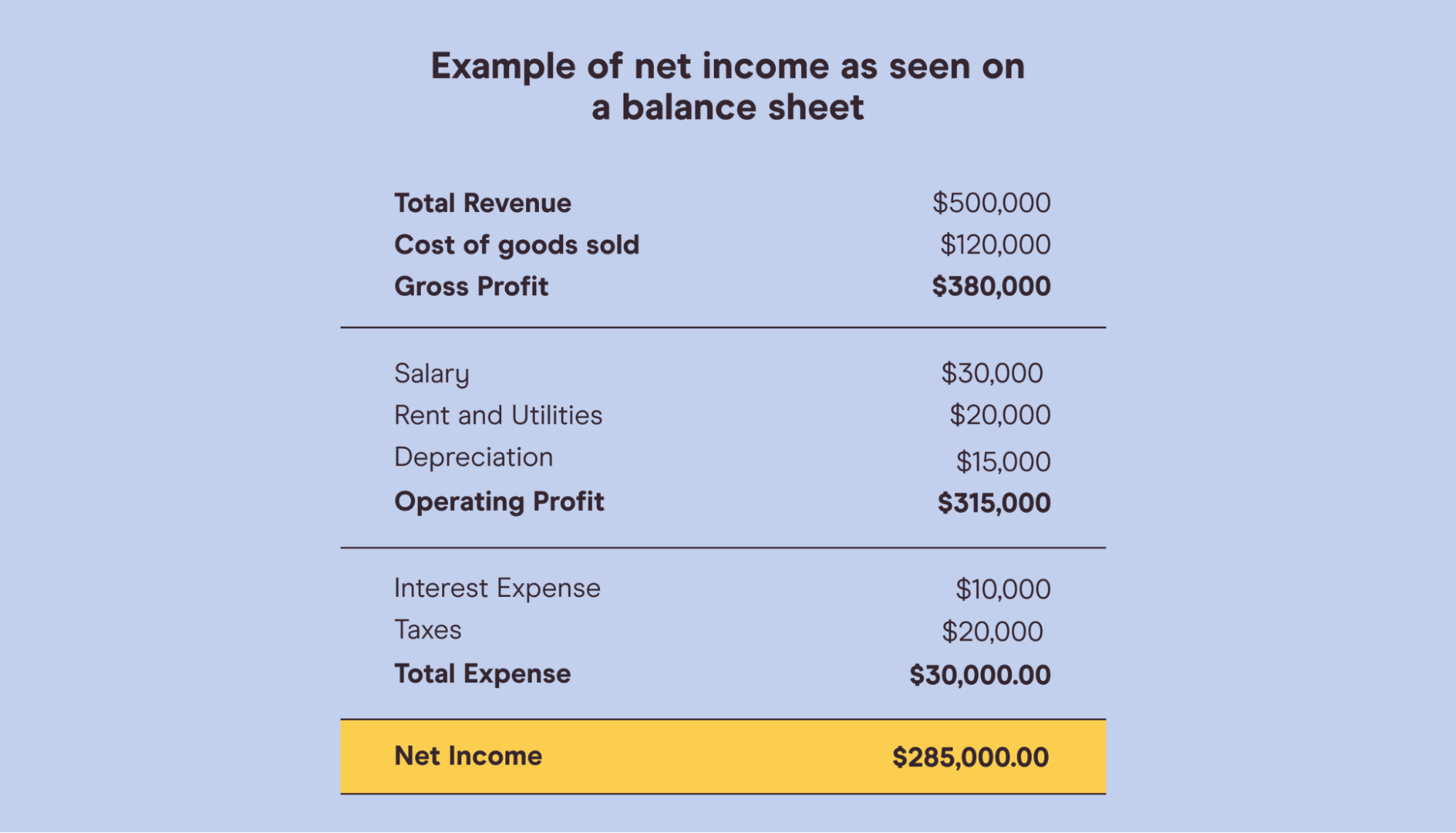

Before one can analyze the impact of net income on the balance sheet, it is vital to understand how that figure is calculated. Net income is the residual amount of earnings left after all operating expenses, interest, taxes, and preferred stock dividends have been deducted from a company’s total revenue.

From Gross Revenue to Operating Income

The journey to net income begins with Total Revenue (top line). From there, the Cost of Goods Sold (COGS) is subtracted to determine Gross Profit. This figure tells us how efficiently a company produces its core products. However, gross profit does not account for the “overhead” of running a business. To get closer to the truth, we subtract Operating Expenses—such as rent, marketing, and payroll—to arrive at Operating Income (or EBIT: Earnings Before Interest and Taxes).

Taxes, Interest, and Non-Operating Items

The final steps involve accounting for the costs of financing and the government’s share. Interest expense on debt is subtracted, and non-operating income (such as interest earned on cash reserves) is added. Finally, corporate income taxes are deducted. What remains is the Net Income. This figure is “clean”—it represents the actual profit available to be reinvested into the business or returned to shareholders. For a business to be considered sustainable, it must demonstrate a consistent ability to produce positive net income after all these obligations are met.

Analyzing the Impact of Net Income on the Balance Sheet Equation

The balance sheet is governed by the formula: Assets = Liabilities + Shareholders’ Equity. Net income plays a starring role in the “Equity” portion of this equation, but its influence ripples across the entire document.

The Double-Entry Connection

Every dollar of net income must be accounted for on both sides of the balance sheet. When a company earns $100,000 in net income, its Equity increases by $100,000 via Retained Earnings. To keep the equation balanced, the “Assets” side must also increase by $100,000. This increase in assets could manifest as an increase in Cash, an increase in Accounts Receivable (money owed by customers), or a decrease in Liabilities (using profit to pay off debt).

How Losses Impact the Balance Sheet

Just as net income builds wealth, a “Net Loss” erodes it. When expenses exceed revenues, the resulting negative number is pulled into the balance sheet, reducing the Retained Earnings account. If a company continues to lose money, its equity can eventually become negative. This is a red flag for investors and creditors, as it suggests the company is “hollowing out” its value and may eventually become insolvent. In the world of business finance, a shrinking equity base due to consistent net losses is often the first sign of a looming bankruptcy.

Why Net Income Matters for Business Health and Valuation

For those focused on the “Money” niche—investors, entrepreneurs, and financial analysts—net income is more than just a number; it is a signal of valuation and strategic capability.

Assessing Profitability Ratios

Net income is the primary input for several key financial ratios used to evaluate a company’s performance. The most famous is Return on Equity (ROE), calculated by dividing net income by shareholders’ equity. ROE measures how effectively management is using the owners’ capital to generate profit. Another critical metric is Earnings Per Share (EPS), which divides net income by the number of outstanding shares. A rising EPS is often the primary driver of a company’s stock price over the long term.

Distinguishing Profit from Cash Flow

A professional analysis must acknowledge one of the most important lessons in finance: Net income is not the same as cash. Because most businesses use “accrual accounting,” net income includes non-cash items. For instance, depreciation is an expense that reduces net income on the Income Statement but does not involve an actual cash outflow. Similarly, a company might report high net income because it made many sales on credit, even if it hasn’t collected the cash yet. Understanding how net income translates into actual “Cash Flow from Operations” on the Cash Flow Statement is essential for determining if a company’s profits are “high quality.”

Strategic Management of Net Income and Retained Earnings

Corporate leadership faces a critical strategic choice at the end of every profitable period: what should be done with the net income? The decision directly dictates the future appearance of the balance sheet.

Reinvestment for Growth

Many high-growth companies, particularly in the tech or emerging market sectors, choose to retain 100% of their net income. By keeping these profits as Retained Earnings, they build up a “war chest” of equity. This equity can be used to purchase new equipment (increasing fixed assets), fund research and development, or acquire smaller competitors. For the investor, the value is not found in a check in the mail, but in the appreciation of the company’s book value and stock price.

Dividends and Share Buybacks

Mature companies with stable cash flows often find they have more net income than they can profitably reinvest. In these cases, they may pay out a portion of net income as Dividends. When a dividend is paid, the amount is deducted from Retained Earnings on the balance sheet. Another option is a Share Buyback, where the company uses its earnings to purchase its own stock from the market. This reduces the number of shares outstanding, effectively increasing the “slice of the pie” for remaining shareholders. Both strategies are ways of transferring the wealth represented by net income back to the individuals who own the brand.

Conclusion: The Holistic View of Financial Success

In summary, net income is the engine that drives the balance sheet. While the Income Statement tells you how much fuel you’ve added, the Balance Sheet tells you how much is currently in the tank and how the vehicle’s structure is holding up. A company with high net income but a weak balance sheet (too much debt, too little liquidity) is a house built on sand. Conversely, a company with a fortress-like balance sheet but no net income is a stagnant entity that will eventually deplete its reserves.

For anyone navigating the world of personal or business finance, mastering the interplay between these two documents is non-negotiable. Net income on a balance sheet is the ultimate record of progress—it is the proof that a business strategy is working, that value is being created, and that the organization is growing stronger with every passing fiscal period. By looking at net income through the lens of the balance sheet, you gain a 360-degree view of financial reality, allowing for smarter investments and more resilient business operations.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.