In the world of corporate finance and investing, the balance sheet serves as a roadmap to a company’s stability and future potential. Among the various metrics found on this financial statement, “Net Fixed Assets” (NFA) stands out as a critical indicator of a firm’s long-term operational capacity. Whether you are an entrepreneur managing your own business or an investor looking for the next big opportunity, understanding what net fixed assets are—and how they impact a company’s bottom line—is essential for making informed financial decisions.

At its core, net fixed assets represent the residual value of a company’s long-term tangible assets after accounting for the wear and tear that occurs over time. This metric provides a realistic view of what a company’s physical infrastructure is worth today, rather than what it cost when it was first purchased.

Understanding the Components of Net Fixed Assets

To grasp the concept of net fixed assets, one must first break down the components that contribute to the final figure. Net fixed assets are not a single purchase; they are the result of a calculation involving gross assets and the accounting measures used to track their usage.

Gross Fixed Assets: The Initial Investment

Gross fixed assets refer to the original purchase price of all long-term tangible assets owned by a business. These are often categorized as Property, Plant, and Equipment (PP&E). Common examples include land, buildings, heavy machinery, specialized tools, office furniture, and company vehicles.

It is important to note that gross fixed assets are recorded at “historical cost.” This means the value on the books does not change based on market fluctuations. If a company bought a factory for $10 million ten years ago, the gross fixed asset value remains $10 million until the asset is sold or retired, regardless of whether the real estate market has boomed or crashed.

Accumulated Depreciation: The Cost of Time

Most physical assets lose value as they age and undergo usage. This process is captured through depreciation. Accumulated depreciation is the total amount of depreciation expense that has been recorded against a fixed asset since it was put into service.

Depreciation is a non-cash expense. It doesn’t represent money leaving the bank account every month; rather, it is an accounting mechanism to spread the cost of an asset over its “useful life.” By subtracting accumulated depreciation from gross fixed assets, we arrive at the “net” value. This tells us how much of the asset’s original economic utility remains.

Impairment Charges and Write-Downs

Occasionally, an asset’s value drops suddenly due to unforeseen circumstances, such as technological obsolescence or physical damage. In these cases, the company must record an “impairment.” This reduces the net fixed asset value beyond standard depreciation. For instance, if a printing company owns a massive offset press that becomes obsolete due to a shift toward digital 3D printing, the value of that press may be “written down” to reflect its diminished market worth.

How to Calculate Net Fixed Assets

Calculating net fixed assets is a straightforward process, but the implications of the resulting number are profound. The basic formula is a pillar of fundamental analysis.

The Standard Formula

The mathematical representation of net fixed assets is:

Net Fixed Assets = (Total Purchase Price of Fixed Assets + Capital Improvements) – (Accumulated Depreciation + Impairment Losses)

In many simplified balance sheets, you will see this expressed as:

Net Fixed Assets = Gross Fixed Assets – Accumulated Depreciation

Capital improvements are added to the gross value because they extend the life or increase the efficiency of the asset. For example, if a company spends $50,000 to install a new high-efficiency engine in an old delivery truck, that $50,000 is capitalized (added to the asset’s value) rather than expensed as a simple repair.

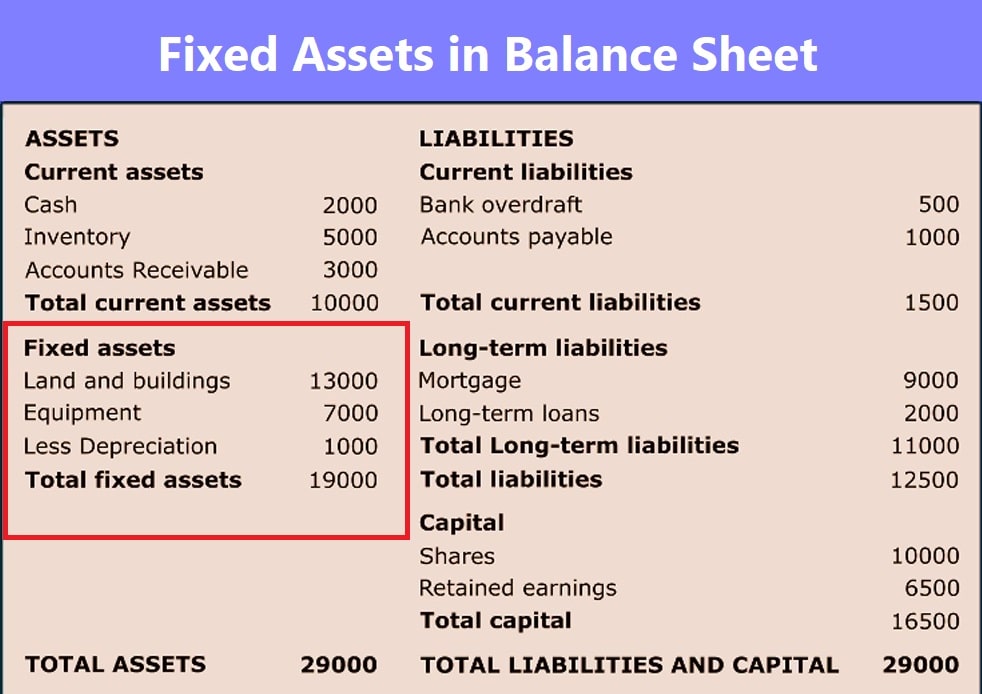

Real-World Example: A Manufacturing Case Study

Imagine a boutique coffee roasting company called “Apex Beans.” To start the business, Apex Beans purchases the following:

- A roasting facility (Building): $500,000

- Industrial Roasters (Machinery): $200,000

- Delivery Vans: $100,000

Their Gross Fixed Assets total $800,000.

Five years later, the company has recorded $300,000 in Accumulated Depreciation ($150k on the building, $100k on machinery, and $50k on the vans).

Their Net Fixed Assets would be:

$800,000 (Gross) – $300,000 (Depreciation) = $500,000.

This $500,000 figure tells the business owner and potential lenders that while they originally spent nearly a million dollars on equipment, the current book value of their infrastructure is half a million.

Why Net Fixed Assets Matter to Investors and Managers

Net fixed assets are more than just a line item on a balance sheet; they are a window into a company’s operational strategy and financial health.

Measuring Capital Intensity and Efficiency

Different industries require different levels of investment in fixed assets. A software company (which is “asset-light”) will have very low net fixed assets compared to an airline or a steel manufacturer (which are “asset-heavy”).

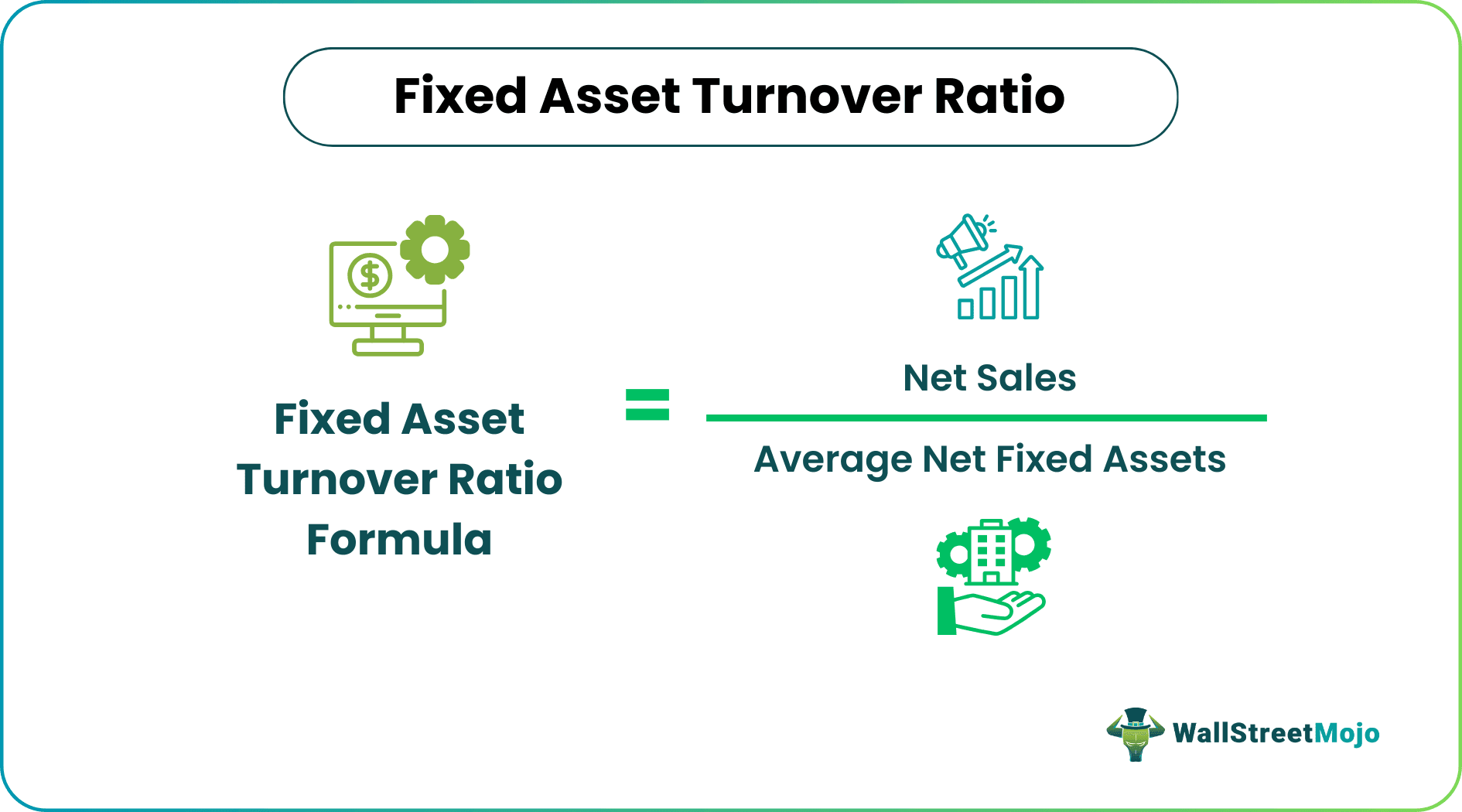

Investors use NFA to calculate the Fixed Asset Turnover Ratio (Revenue / Net Fixed Assets). This ratio measures how efficiently a company uses its physical assets to generate sales. A rising ratio suggests the company is getting more “bang for its buck” from its machinery and facilities. Conversely, a declining ratio might indicate that the company has over-invested in equipment that isn’t producing enough revenue.

Determining the Age of the Asset Base

By comparing net fixed assets to gross fixed assets, analysts can estimate the average age of a company’s infrastructure. If the net fixed assets are very low relative to the gross assets (meaning accumulated depreciation is high), it suggests the company’s equipment is old and may soon require a massive capital infusion for replacements.

This is a critical insight for “Value” investors. A company might look profitable today because it has stopped spending on new equipment, but if its machines are on the verge of breaking down, a massive “Capital Expenditure” (CapEx) bill is looming in the future.

Impact on Solvency and Collateral

For business owners seeking loans, net fixed assets often serve as collateral. Banks are much more likely to lend money against a company with high NFA because these assets have tangible value that can be liquidated if the loan defaults. A high NFA strengthens a company’s balance sheet and improves its creditworthiness, allowing for better interest rates and financing terms.

Net Fixed Assets vs. Other Financial Metrics

To fully understand a company’s position, it is helpful to distinguish net fixed assets from other commonly confused terms.

NFA vs. Current Assets

Current assets include cash, accounts receivable, and inventory—items expected to be converted into cash within one year. Net fixed assets, however, are “long-term” or “non-current.” They are held for use in production rather than for direct sale. While you can sell inventory to pay an immediate bill, you cannot easily sell a factory floor without disrupting your entire business. Therefore, NFA represents “illiquid” wealth.

NFA vs. Total Net Assets (Equity)

“Total Net Assets” is often used interchangeably with “Shareholders’ Equity” (Total Assets – Total Liabilities). Net Fixed Assets is only a subset of the “Assets” portion of that equation. A company could have $1 million in net fixed assets but still have negative equity if they owe $2 million in bank loans. NFA tells you the value of the “stuff” you own; Equity tells you what’s left for the owners after all debts are paid.

NFA vs. Book Value

The “Book Value” of a company is the total value of all its assets minus liabilities. Net fixed assets are the book value of specifically the physical equipment. In the modern economy, many companies have a market value much higher than their book value or NFA because of “Intangible Assets” like brand reputation, patents, and proprietary software.

Strategic Management of Net Fixed Assets for Business Growth

Successful businesses manage their net fixed assets strategically to maximize tax benefits and ensure long-term sustainability.

The Lifecycle of Reinvestment

A healthy company usually maintains a steady relationship between depreciation and capital expenditure. If depreciation is consistently higher than capital expenditure, the net fixed asset base is shrinking. While this might boost short-term cash flow (since the company isn’t spending on new gear), it eventually leads to operational decline. High-growth companies often have capital expenditures that far exceed depreciation, indicating they are aggressively building out their capacity for future production.

Tax Implications and Accelerated Depreciation

Governments often use depreciation rules to encourage business investment. For example, “Section 179” or “Bonus Depreciation” allows businesses to deduct the full purchase price of certain fixed assets in the first year, rather than spreading it out over a decade.

While this lowers the “Net Fixed Asset” value on the tax books more quickly, it provides a massive “Money” benefit by reducing the company’s taxable income and keeping more cash in the business. Strategic managers must balance the desire for a “strong-looking” balance sheet (high NFA) with the desire for “tax efficiency” (low taxable income).

Conclusion

Net fixed assets are a vital pulse-check for any physical-goods business. By accounting for the original cost of investment and the inevitable decline in value over time, NFA provides a realistic picture of a company’s tangible worth.

For the investor, it is a tool to measure efficiency and predict future spending needs. For the business owner, it is a metric of collateral and a guide for when to reinvest in the business. In the grand landscape of business finance, understanding net fixed assets ensures that you aren’t just looking at what a company spent, but what it actually possesses to drive future success. By keeping a close eye on this figure, you can better navigate the complexities of long-term financial planning and wealth preservation.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.