For millions of Americans, Social Security represents a cornerstone of their financial future, a promise of income in retirement, and a critical safety net in times of disability or loss. Yet, despite its pervasive influence, many individuals find themselves asking a fundamental question: “What is my Social Security benefit?” Understanding this figure is not just a matter of curiosity; it’s a vital component of informed financial planning, allowing you to project future income, make strategic decisions about retirement timing, and build a comprehensive personal finance strategy.

Social Security, officially known as the Old-Age, Survivors, and Disability Insurance (OASDI) program, is a federal initiative designed to provide a measure of protection to workers and their families. Funded primarily through payroll taxes, it pays monthly benefits to eligible retirees, disabled individuals, and survivors of deceased workers. Far from a mere government handout, it’s an earned benefit, a return on decades of contributions made throughout your working life. Delving into the intricacies of how your benefit is calculated and how you can access this crucial information is the first step toward demystifying this essential program.

Understanding the Pillars of Social Security Benefits

Social Security is a multi-faceted program, offering more than just retirement income. Its design serves to protect families from various life uncertainties, providing financial stability when it’s needed most.

A Lifeline for Millions

At its core, Social Security acts as a social insurance program. It provides three main types of benefits:

- Retirement Benefits: The most widely known, these benefits provide income to eligible workers when they decide to retire. The age at which you claim significantly impacts the amount you receive.

- Disability Benefits: Should you become unable to work due to a severe medical condition that is expected to last at least one year or result in death, Social Security Disability Insurance (SSDI) can provide income replacement.

- Survivors Benefits: In the unfortunate event of a worker’s death, certain family members—including spouses, children, and dependent parents—may be eligible for monthly benefits. This provides crucial financial support during a difficult time.

These pillars collectively form a robust system intended to cushion individuals and families against the economic shocks of old age, disability, and death. Recognizing the breadth of the program underscores its importance in a holistic financial plan.

Who is Eligible?

Eligibility for Social Security benefits is determined by your work history and, more specifically, by the number of “work credits” you accumulate. As you work and pay Social Security taxes, you earn these credits.

- Credit Earning: You can earn up to four credits each year. The amount of earnings required for a credit changes annually but is relatively modest. For instance, in 2024, you earn one credit for every $1,730 in earnings, up to the maximum of four credits for earnings of $6,920 or more.

- General Requirement: Most people need 40 credits, earned over at least 10 years of work, to qualify for retirement benefits. For disability or survivor benefits, the number of required credits can be lower, depending on your age at the time of disability or death. For example, younger workers need fewer credits to qualify for disability benefits.

This credit system ensures that benefits are earned through consistent contributions to the system, reinforcing the insurance-like nature of Social Security.

Factors Influencing Your Social Security Benefit Amount

Calculating your Social Security benefit is not a one-size-fits-all equation. Several critical factors, unique to your work history and claiming decisions, come into play.

Your Earning History

The primary driver of your Social Security benefit is your lifetime earnings record. The Social Security Administration (SSA) calculates your benefit based on your average indexed monthly earnings (AIME) over your 35 highest-earning years.

- Indexing: Your earnings from past years are “indexed” to account for changes in average wages over time. This process brings earlier years’ earnings up to a comparable level with more recent earnings, ensuring that your benefit reflects the real purchasing power of your lifetime contributions.

- The 35-Year Rule: The SSA looks at your entire earnings history but only uses your top 35 years. If you have fewer than 35 years of earnings, the missing years are counted as zeros, which can significantly lower your average. This highlights the importance of consistent employment throughout your career.

- Primary Insurance Amount (PIA): Your AIME is then run through a formula to determine your Primary Insurance Amount (PIA), which is the benefit you would receive if you start collecting at your Full Retirement Age (FRA). The PIA formula is progressive, meaning lower earners receive a higher percentage of their average earnings back as benefits compared to higher earners.

When You Claim Benefits

Perhaps the most impactful decision you’ll make regarding your Social Security benefit is when you choose to start receiving it. This decision can permanently alter your monthly payment amount.

- The Full Retirement Age (FRA) Explained: Your FRA is the age at which you are entitled to 100% of your PIA. This age varies based on your birth year. For those born between 1943 and 1954, FRA is 66. It gradually increases for later birth years, reaching 67 for those born in 1960 or later.

- Claiming Early: You can start receiving retirement benefits as early as age 62. However, claiming before your FRA results in a permanent reduction in your monthly benefit. The reduction can be substantial, as much as 25% to 30% if you claim at 62.

- Delaying Benefits: Conversely, you can choose to delay claiming benefits beyond your FRA, up to age 70. For each year you delay past your FRA, your benefit increases by a certain percentage, known as “delayed retirement credits.” These credits accumulate at 8% per year (for those born 1943 or later), resulting in a significantly higher monthly payment. By delaying until age 70, you could potentially increase your FRA benefit by 24% to 32%.

Cost-of-Living Adjustments (COLAs)

Once you start receiving Social Security benefits, your payments are not static. They are subject to annual Cost-of-Living Adjustments (COLAs), designed to help your benefits keep pace with inflation. These adjustments are typically announced in October and take effect the following January, based on changes in the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). While not guaranteed every year, COLAs are a critical feature that protects the purchasing power of your benefits over time.

How to Find Your Estimated Social Security Benefit

Given the complexity of the calculations, it might seem daunting to figure out your specific benefit. Fortunately, the Social Security Administration provides user-friendly tools to give you accurate estimates.

The Power of the my Social Security Account

The most direct and reliable way to find your estimated Social Security benefit is by creating a “my Social Security” account online at the SSA’s official website (www.ssa.gov).

- Account Creation: The process involves verifying your identity, which is a secure multi-step process. Once established, this account provides personalized information tailored to your earnings record.

- Accessing Your Statement: Your “my Social Security” account grants you instant access to your Social Security Statement. This statement is a personalized report that includes your detailed earnings history and estimates of your future benefits.

Understanding Your Social Security Statement

Your Social Security Statement is a treasure trove of vital information. Key sections include:

- Estimated Benefits: It provides estimated monthly benefits at different claiming ages: your current age if you became disabled, at your full retirement age, and at age 70. This allows for direct comparison and planning.

- Earnings Record: A comprehensive list of your annual earnings as reported to the SSA. It’s crucial to review this carefully for any discrepancies, as errors could impact your future benefits.

- Tax Information: Details on the amount of Social Security and Medicare taxes you and your employers have paid.

- Program Information: General information about Social Security, how benefits are calculated, and how to apply.

Regularly reviewing your Social Security Statement—at least once a year—is a recommended financial habit. It ensures your earnings record is accurate and keeps you informed about your projected benefits, allowing you to adjust your financial plans as needed.

Online Calculators and Tools

In addition to your personalized statement, the SSA website offers various online calculators that can help you explore different claiming scenarios. These tools allow you to input different retirement ages, future earnings projections, and other variables to see how they might impact your benefit. While these are estimates, they provide valuable insights for strategic planning.

Strategic Considerations for Maximizing Your Benefits

Knowing your estimated benefit is just the beginning. Strategic planning can help you maximize the overall value you derive from Social Security.

The Impact of Spousal and Survivor Benefits

Social Security is not just for individual workers; it also provides benefits to family members.

- Spousal Benefits: If you are married, divorced (under certain conditions), or widowed, you may be eligible for benefits based on your spouse’s (or former spouse’s) earnings record, even if you never worked or earned significantly less. A spouse can receive up to 50% of their partner’s FRA benefit.

- Survivor Benefits: As mentioned, surviving spouses and children can receive benefits. These can be particularly crucial for families with young children or a surviving spouse who has not yet reached retirement age.

- Claiming Strategies: For married couples, sophisticated claiming strategies exist to maximize combined lifetime benefits. This often involves one spouse delaying benefits while the other claims, or one claiming spousal benefits while deferring their own worker benefit.

Working While Receiving Benefits

If you claim Social Security benefits before your full retirement age and continue to work, your earnings may cause your benefits to be temporarily reduced.

- Earnings Limit: The SSA sets an annual earnings limit. If you earn above this limit, a portion of your benefits will be withheld. For instance, in 2024, if you are under FRA, $1 in benefits is withheld for every $2 you earn above $22,320.

- No Earnings Limit at FRA: Once you reach your FRA, the earnings limit disappears, and you can earn as much as you like without any reduction in your Social Security benefits.

- Benefit Recalculation: Any benefits withheld due to the earnings limit are not lost forever. When you reach your FRA, the SSA will recalculate your benefit amount to account for the months benefits were withheld, effectively increasing your future monthly payments.

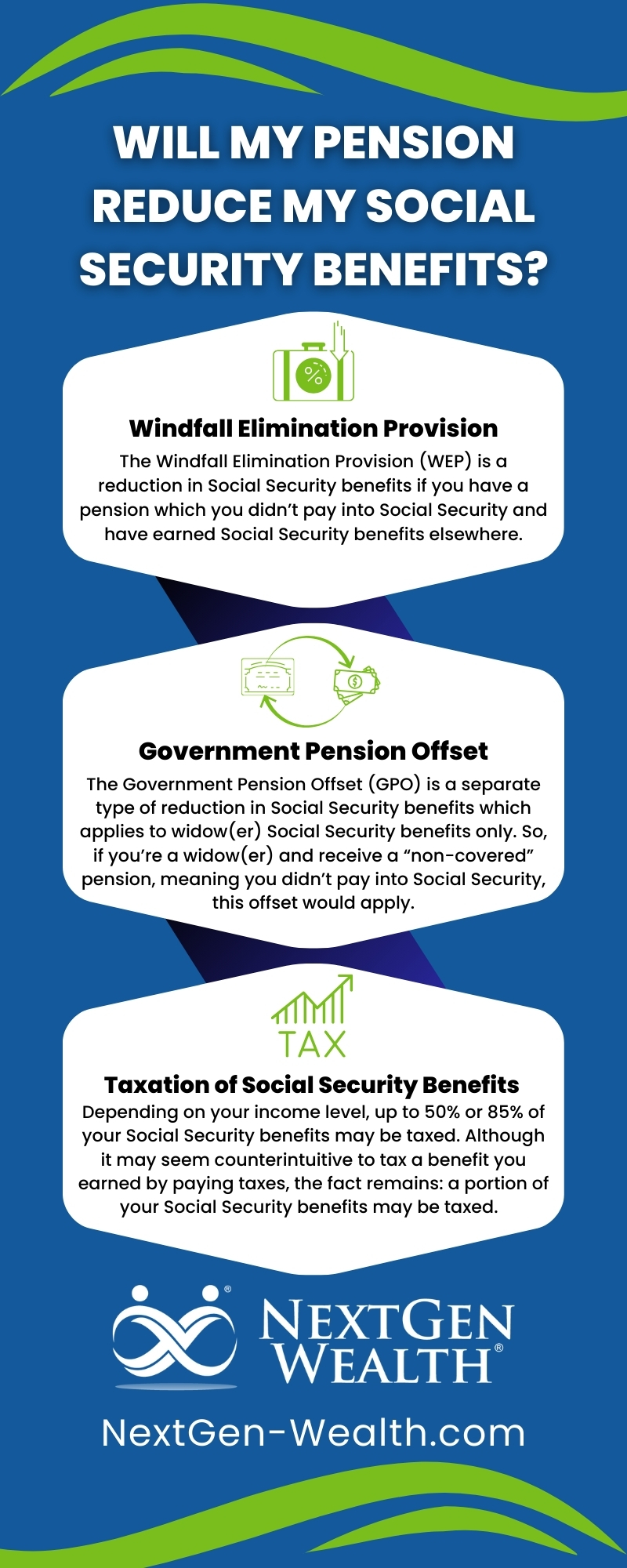

Taxation of Social Security Benefits

While Social Security benefits are a source of income, they may be subject to federal income tax, depending on your “provisional income.”

- Provisional Income: This includes your adjusted gross income, tax-exempt interest income, and half of your Social Security benefits.

- Tax Thresholds: If your provisional income exceeds certain thresholds ($25,000 for single filers, $32,000 for married filing jointly), a portion of your Social Security benefits (up to 85%) may become taxable.

- State Taxes: A few states also tax Social Security benefits, so it’s important to check your state’s specific laws.

Understanding these tax implications is crucial for accurate retirement income planning and tax efficiency.

Coordinating with Other Retirement Income

Social Security is rarely the sole source of retirement income. For most individuals, it’s one piece of a broader financial puzzle that includes 401(k)s, IRAs, pensions, and personal savings.

- Holistic Planning: Consider how your Social Security claiming strategy integrates with withdrawals from other retirement accounts. For instance, delaying Social Security may mean drawing down more from your 401(k) in early retirement, but it secures a higher, inflation-adjusted income stream later in life.

- Longevity Risk: A higher Social Security benefit, secured by delayed claiming, offers excellent protection against longevity risk – the risk of outliving your other savings.

The Future of Social Security and Your Financial Planning

Social Security, like any large government program, faces ongoing challenges and discussions about its long-term sustainability. While these discussions are important, they should not deter you from planning with the program as a vital component of your retirement strategy.

Addressing Solvency Concerns

Projections from the Social Security Trustees indicate that the program can pay 100% of promised benefits until around the mid-2030s, after which it will be able to pay about 80% of scheduled benefits if no legislative changes are made. These projections are often misinterpreted as the program going “broke.” In reality, Social Security will still be able to pay a significant portion of benefits even without intervention, as long as people continue to work and pay taxes. However, potential adjustments like small increases in the full retirement age, modest tax rate adjustments, or changes to the benefit formula are topics of ongoing debate.

The Importance of Diversified Retirement Savings

Regardless of future legislative changes, the fundamental principle remains: Social Security should be viewed as one, albeit significant, leg of your retirement income stool, not the entire structure.

- Personal Responsibility: It underscores the importance of personal savings through 401(k)s, IRAs, and other investment vehicles. A diversified approach ensures that your financial security is not solely reliant on any single source.

- Flexibility: Relying on multiple income streams provides greater flexibility and resilience in retirement, allowing you to adapt to economic changes or unexpected expenses.

Conclusion

Understanding “what is my Social Security benefit” is an essential step towards securing a comfortable and predictable retirement. From comprehending the factors that shape your benefit – your earnings history, claiming age, and COLAs – to actively using your “my Social Security” account to access personalized estimates, taking control of this information empowers you to make informed decisions.

Remember that Social Security is more than just a check; it’s a vital component of your financial ecosystem, offering protection in various life stages. By strategically considering when and how you claim your benefits, coordinating them with other retirement income sources, and staying informed about the program’s future, you can effectively leverage Social Security to build a robust and resilient financial plan for your future. Don’t leave this critical piece of your retirement puzzle to chance; educate yourself and plan proactively.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.