For millions of Americans, the journey toward higher education is paved with student loans. However, once the degree is earned and the graduation caps are tossed, a new name often enters the borrower’s lexicon: MOHELA. If you have recently checked your financial statements or received an email regarding your federal student loans, you might be asking yourself, “What is MOHELA, and why do they have my debt?”

In the complex ecosystem of personal finance, understanding who manages your debt is just as important as understanding the debt itself. MOHELA is not just a random acronym; it is a pivotal player in the federal student loan landscape. This guide will explore the institution’s role, its specific financial responsibilities, and how you can strategically manage your relationship with them to achieve financial freedom.

The Foundation: Who Is MOHELA?

To understand MOHELA’s role in your personal finances, it is essential to first define what it is. MOHELA stands for the Missouri Higher Education Loan Authority. Established in 1981, it is a leading student loan servicer and one of the largest in the United States. While its name suggests a regional focus, it operates on a national scale as a primary contractor for the U.S. Department of Education.

From a State Entity to a National Powerhouse

MOHELA was originally created as a quasi-governmental entity to provide a secondary market for student loans within the state of Missouri. Over the decades, its scope expanded significantly. Today, it serves as a federal loan servicer, meaning the federal government hires them to handle the administrative side of your loans. They do not “own” your federal debt—the Department of Education does—but MOHELA is the entity you interact with for everything from monthly payments to balance inquiries.

The Distinction Between Lender and Servicer

In the realm of money management, it is crucial to distinguish between a lender and a servicer. The lender (in the case of Direct Loans, the U.S. Government) provides the capital. The servicer (MOHELA) manages the logistics. Think of MOHELA as the property manager for a building owned by the government. They collect the “rent” (loan payments), manage the paperwork, and provide customer support, but they are bound by the rules set by the owner.

Core Responsibilities: Managing Your Debt Lifecycle

As a borrower, your primary financial touchpoint for your student debt is your servicer. MOHELA handles a wide array of tasks that directly impact your monthly budget and long-term financial health. Understanding these services allows you to utilize their tools more effectively.

Payment Processing and Account Management

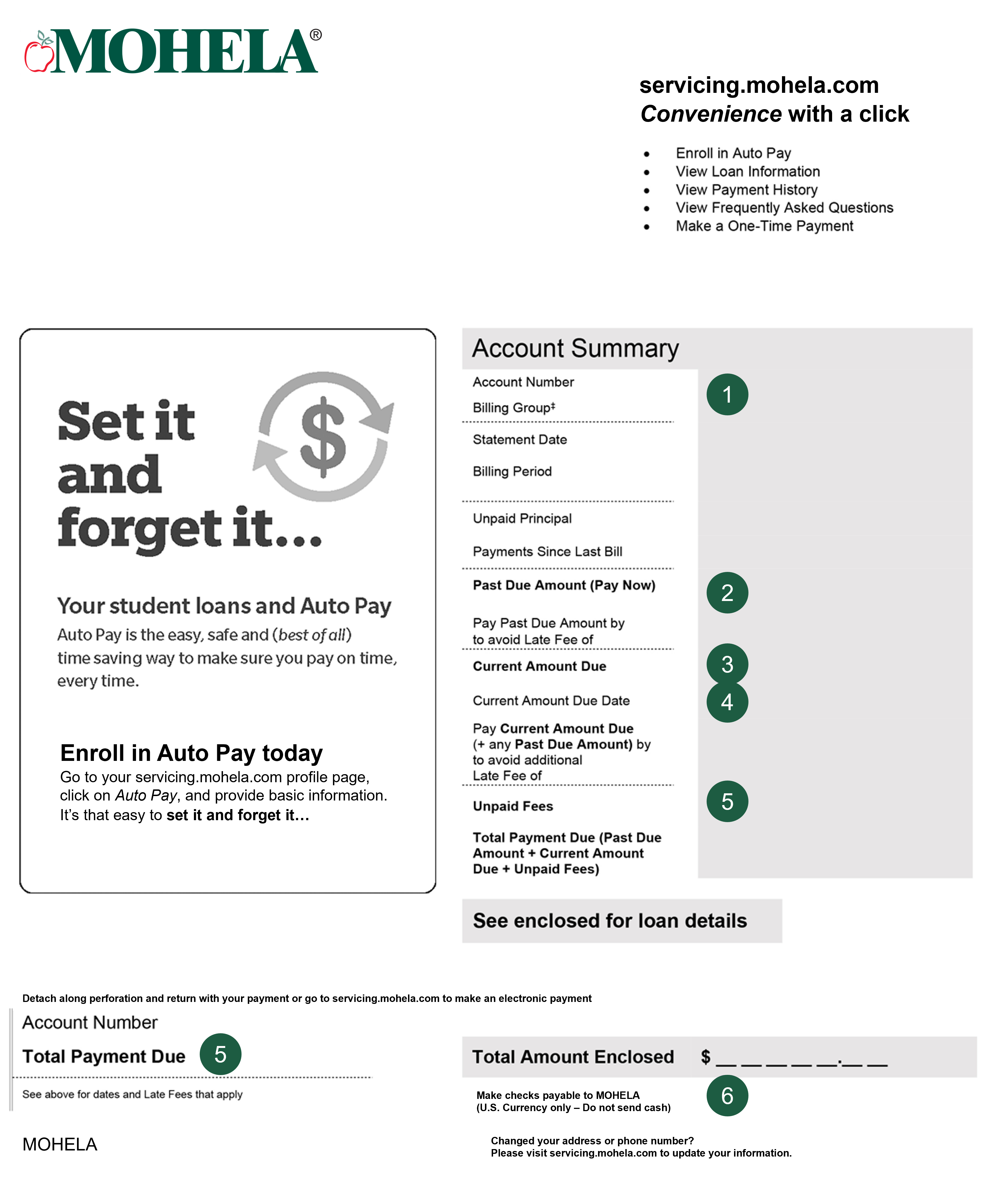

The most visible role of MOHELA is the collection and application of payments. When you send money to MOHELA, they are responsible for distributing that payment across your various loan sequences. They must apply the funds according to federal regulations: first to accrued interest, then to the principal balance. For a savvy investor or a disciplined budgeter, ensuring these payments are applied correctly is vital for reducing the total cost of the loan over time.

Income-Driven Repayment (IDR) Administration

For many borrowers, the standard 10-year repayment plan is financially stifling. MOHELA is responsible for processing applications for Income-Driven Repayment (IDR) plans, such as the SAVE (Saving on a Valuable Education) plan, PAYE, and IBR. These plans are essential financial tools that cap your monthly payment at a percentage of your discretionary income. MOHELA’s role is to verify your income documentation annually and adjust your payment amounts accordingly.

Loan Consolidation and Deferment

If you choose to consolidate multiple federal loans into a single Direct Consolidation Loan, MOHELA may be the entity that facilitates this transition. Furthermore, if you encounter financial hardship, MOHELA manages requests for deferment or forbearance. While these options should be used sparingly due to interest accrual, they are critical safety nets in a comprehensive financial plan.

MOHELA and Public Service Loan Forgiveness (PSLF)

Perhaps the most significant reason MOHELA has gained national attention in recent years is its specific designation regarding the Public Service Loan Forgiveness (PSLF) program. For a long period, MOHELA was the sole servicer responsible for managing all accounts for borrowers pursuing PSLF.

The Transition of PSLF Management

In 2022, the Department of Education transitioned all PSLF-eligible accounts from the former servicer, FedLoan Servicing, to MOHELA. This made MOHELA the central hub for teachers, nurses, firefighters, and non-profit employees. If you are working toward tax-free forgiveness after 120 qualifying payments, MOHELA is the entity that tracks your employment certification forms and tallies your progress.

Strategic Implications for Public Servants

Managing a PSLF account requires meticulous record-keeping. Because MOHELA handles the verification of your “qualifying payments,” borrowers must be proactive. Financial experts recommend downloading your payment history annually and keeping copies of all certified employment forms. In recent months, the Department of Education has begun moving some of the PSLF tracking functions directly to StudentAid.gov to streamline the process, but MOHELA remains the primary servicer for the actual payment accounts of these borrowers.

Optimizing Your Experience: Strategies for Financial Success

Dealing with a large bureaucracy like MOHELA can be frustrating, but from a personal finance perspective, there are several strategies you can employ to ensure your loans are handled efficiently and your credit remains protected.

Leveraging Automation for Interest Reductions

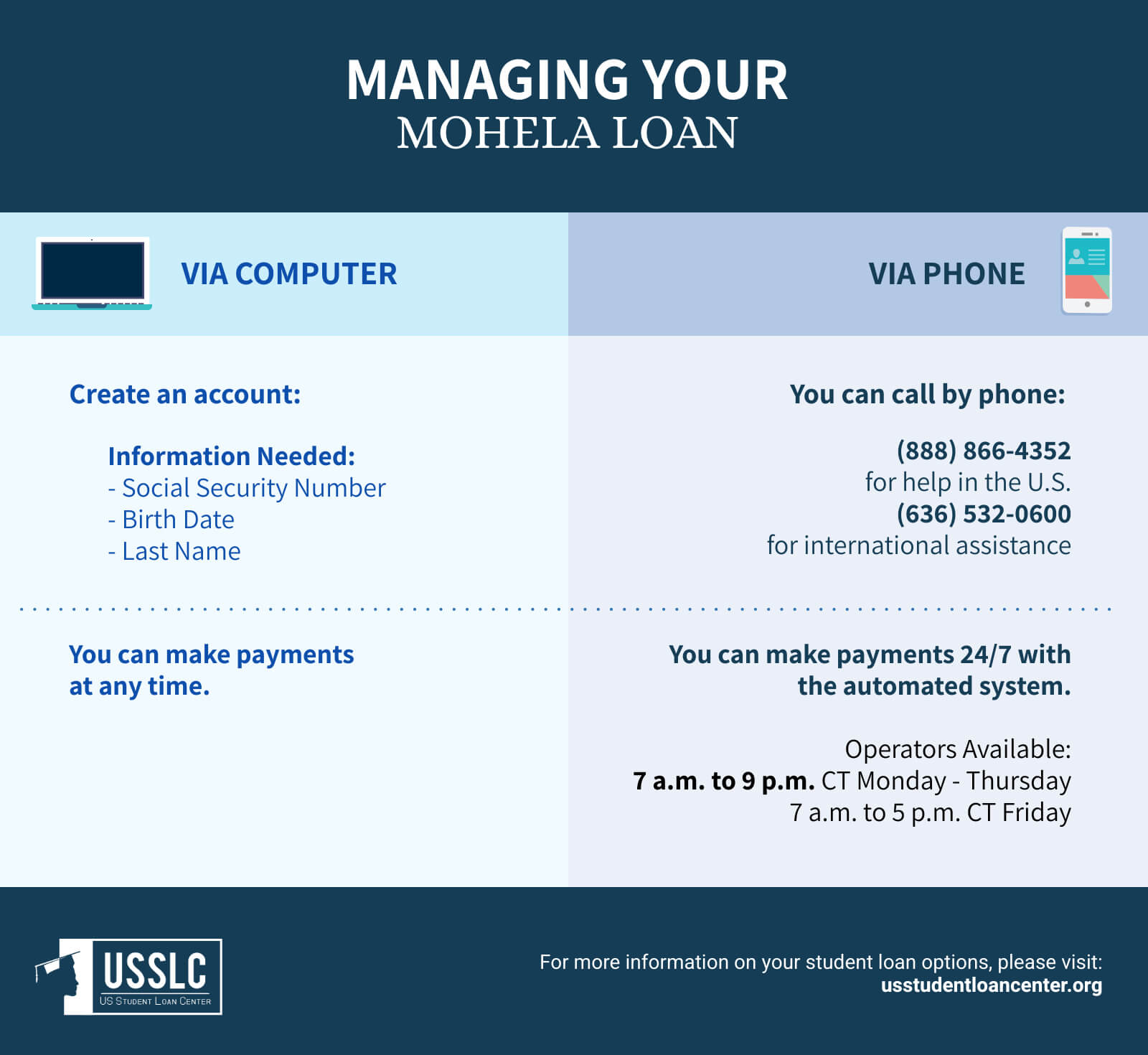

One of the simplest financial wins for any borrower is signing up for “Auto-Pay” through the MOHELA portal. Most federal servicers, including MOHELA, offer a 0.25% interest rate reduction for borrowers who enroll in automatic debit. While a quarter of a percentage point may seem small, over the life of a $50,000 or $100,000 loan, this can save thousands of dollars in interest and shave months off your repayment timeline.

Monitoring Credit Reporting Accuracy

Your student loan performance is a major component of your credit score. MOHELA reports your payment status to the major credit bureaus (Experian, Equifax, and TransUnion). It is imperative to monitor your credit report to ensure that MOHELA is accurately reflecting your balance and on-time payment history. If you enter a period of administrative forbearance (often initiated by the servicer during plan transitions), verify that it is not being incorrectly reported as a missed payment.

Escalating Disputes and Seeking Resolution

If you encounter errors in your account—such as misapplied payments or incorrect interest calculations—you must act quickly. Start by using MOHELA’s internal secure messaging system to create a paper trail. If the issue is not resolved, the next financial step is to contact the Federal Student Aid (FSA) Ombudsman Group. This is an impartial resource designed to resolve disputes between borrowers and servicers.

The Shifting Landscape of Student Loan Servicing

The world of student debt is currently in a state of flux. Legislative changes, court rulings on debt relief, and new repayment models mean that your relationship with MOHELA may change over time.

The Impact of Modernization Initiatives

The Department of Education is currently working on the “Unified Servicing and Data Solution” (USDS). This initiative aims to create a more seamless experience for borrowers, potentially moving more account management features to the central StudentAid.gov portal. For MOHELA borrowers, this means that while MOHELA will still handle the money, the interface and the way you interact with your data might become more standardized across all federal servicers.

Staying Informed in an Evolving Market

Financial literacy requires staying ahead of the curve. Whether it is the introduction of the SAVE plan or adjustments to how interest capitalizes, these changes directly affect your net worth. Borrowers should regularly check for updates regarding MOHELA’s contract status and any new federal regulations that might allow for balance adjustments or one-time account reviews.

Conclusion: Taking Control of Your Financial Future

Understanding “What is MOHELA” is the first step in taking ownership of your financial destiny. While the student loan system can feel overwhelming, MOHELA is simply a tool—a servicer through which you execute your repayment strategy. By understanding their role in payment processing, their specific grip on programs like PSLF, and the technical ways you can lower your interest rates, you transform from a passive debtor into an active financial manager.

Your student loans are a significant part of your financial portfolio. By maintaining clear communication with MOHELA, utilizing IDR plans effectively, and keeping meticulous records, you can navigate the path to repayment with confidence, ensuring that your education remains an investment in your future rather than a permanent weight on your wealth-building potential.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.