Leasing a house represents a distinctive financial arrangement in the real estate market, often misconstrued as simple renting. While sharing some superficial similarities with a traditional rental agreement, house leasing, particularly in its lease-to-own variant, introduces a complex layer of financial commitments and potential future ownership that demands careful consideration. It’s a contractual agreement between two parties—the lessee (tenant) and the lessor (owner)—where the lessee pays a periodic fee for the exclusive right to occupy a property for a specified term, frequently with an embedded option to purchase the property at a predetermined price. This structure bridges the gap between renting and buying, offering a pathway to homeownership for individuals who might not immediately qualify for a traditional mortgage.

Understanding House Leasing: More Than Just Renting

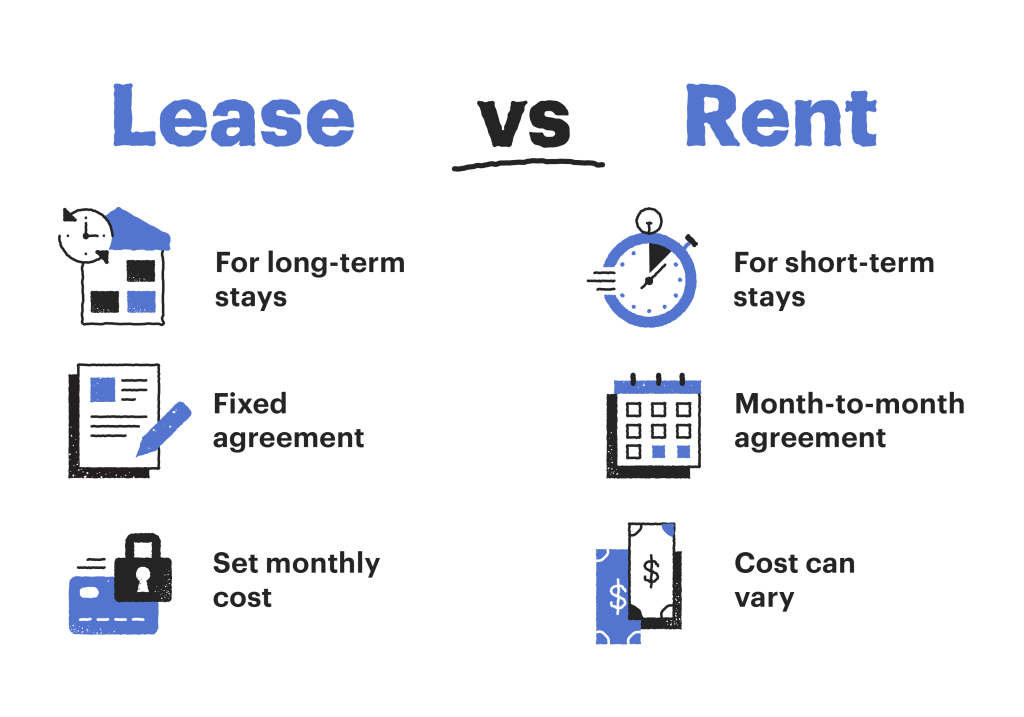

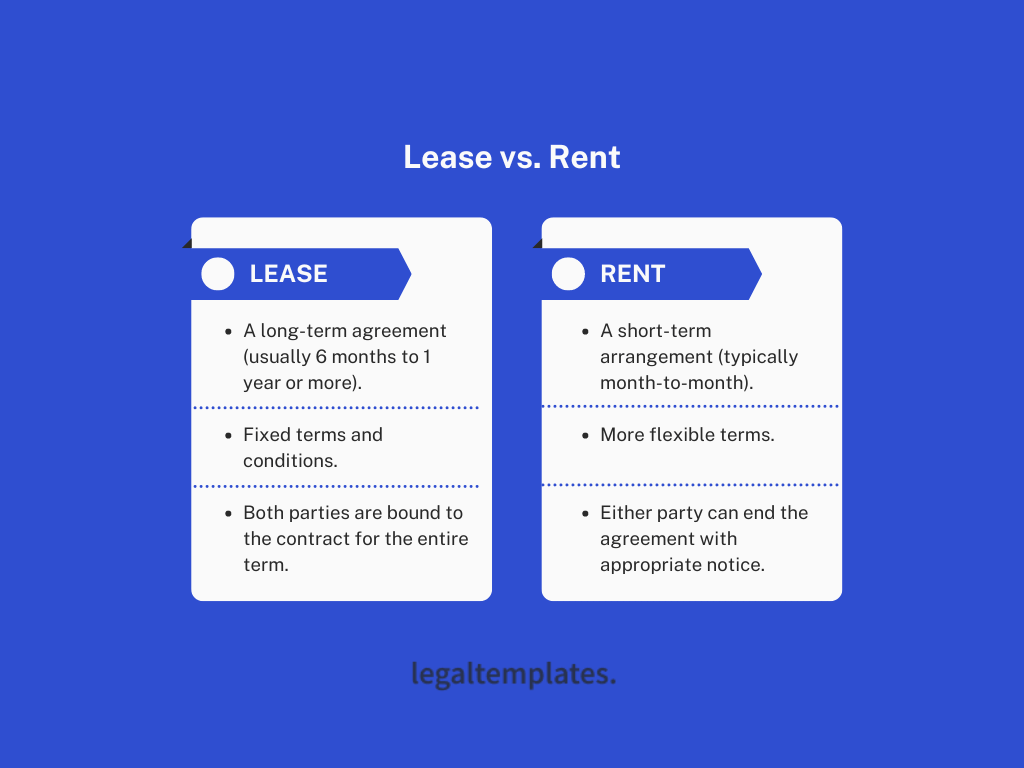

At its core, house leasing is a long-term rental contract that often includes clauses for eventual property acquisition. This financial tool is designed to provide stability for both parties while allowing the lessee to transition towards ownership. It contrasts sharply with the short-term, less financially binding nature of typical rental agreements.

Defining House Leasing

A house lease agreement is a legal document outlining the terms and conditions under which a tenant occupies a property for an extended period, typically one to three years, though longer terms are not uncommon. Unlike standard rentals where the tenant’s financial obligation is limited to rent and utilities, a lease agreement often involves an upfront option fee, which is a non-refundable payment giving the lessee the exclusive right to purchase the property later. The monthly payments in a lease agreement are usually higher than market rent, with a portion of this “rent credit” often applied towards the down payment if the purchase option is exercised. This intricate financial structure provides a clear incentive for the lessee to maintain the property and plan for its eventual acquisition.

Key Differences from Traditional Renting

The divergence from traditional renting is primarily financial and aspirational. In a traditional rental scenario, the tenant builds no equity and accrues no financial benefit beyond shelter; their monthly payments are purely for occupancy. With a house lease, especially a lease-to-own arrangement, a portion of the monthly payment often acts as a forced savings mechanism, accumulating credit towards the future purchase price. Furthermore, the lessee in a lease agreement typically assumes more responsibility for property maintenance and repairs, similar to an owner, as they have a vested interest in the property’s condition for their potential future acquisition. This shift in responsibility is a critical financial distinction, moving costs from the lessor to the lessee, which must be factored into a lessee’s budget.

The Lease-Purchase Option Explained

The lease-purchase option is the cornerstone of many house leasing arrangements. It grants the lessee the exclusive right, but not the obligation, to buy the property at a specific price at the end of the lease term. This purchase price is usually agreed upon at the outset of the lease, offering the lessee protection against rising market values and the lessor a guaranteed future sale price. The financial implications are significant: the option fee paid upfront is usually non-refundable, meaning if the lessee decides not to purchase the house, that initial investment is lost. This financial risk necessitates thorough due diligence before entering such an agreement, as the opportunity cost of the option fee can be substantial. For the lessor, it secures a potential buyer and an income stream, reducing vacancy risk and marketing costs.

Financial Mechanics of a House Lease Agreement

Understanding the financial architecture of a house lease is paramount for both lessees and lessors. It involves more than just monthly rent, encompassing various fees, credits, and responsibilities that shape the overall cost and benefit.

Lease Payments and Rent Credits

The monthly lease payments in a house leasing agreement are typically structured to be higher than conventional market rent for comparable properties. This premium is not arbitrary; a predetermined portion of these payments is often designated as a “rent credit” or “option credit,” which accumulates over the lease term and is applied towards the eventual purchase price or down payment. For instance, if the monthly lease payment is $2,000 and $300 is allocated as a rent credit, after a 36-month lease, the lessee would have accumulated $10,800 towards their home purchase. This mechanism acts as a form of forced savings, helping lessees build equity and a down payment while occupying the property. However, it’s crucial to understand that if the purchase option is not exercised, these accumulated rent credits are typically forfeited, representing a significant financial loss.

Upfront Costs and Option Fees

Entering a house lease agreement invariably involves upfront financial outlays beyond a standard security deposit. The most prominent of these is the “option fee” or “option consideration.” This fee is a non-refundable payment made by the lessee to the lessor at the beginning of the lease, securing the exclusive right to purchase the property at a later date. Option fees can range anywhere from 1% to 10% of the property’s agreed-upon purchase price, representing a substantial initial investment. While this fee buys the lessee time and the option to buy, its non-refundable nature means that if the lessee fails to secure financing or simply changes their mind about purchasing, this entire sum is lost. This makes the option fee a critical financial risk that prospective lessees must weigh carefully against the potential benefits of the lease-to-own path.

Who Covers Maintenance and Repairs?

One of the key financial distinctions between a lease and a traditional rental lies in the responsibility for property maintenance and repairs. In a standard rental, the landlord is typically responsible for most major repairs and structural maintenance. However, in a house lease, particularly a lease-to-own, the agreement often shifts a significant portion, if not all, of these responsibilities to the lessee. This is because the lessee has a vested interest in the property’s condition, anticipating future ownership. While this means the lessee can customize and improve the property without direct landlord approval in some cases, it also means bearing the financial burden of leaky roofs, HVAC failures, or plumbing issues. Lessees must budget for potential maintenance costs, much like a homeowner, as these expenses can significantly impact their overall financial viability of the agreement.

Property Taxes and Insurance Considerations

Financial responsibility for property taxes and homeowner’s insurance can also vary in a house lease. In most cases, especially if the lessor still holds the mortgage, they remain legally responsible for paying property taxes and maintaining homeowner’s insurance. However, the lease agreement may stipulate that the lessee reimburses the lessor for these costs, or a prorated amount, as part of their monthly payments. Alternatively, the agreement might require the lessee to obtain renter’s insurance that specifically covers their personal belongings and liability, and in some more complex lease-to-own structures, the lessee may even be responsible for acquiring a specific type of insurance that covers the structure as well. Understanding who carries these financial burdens is crucial, as they represent substantial annual costs that directly impact the overall affordability and risk exposure of the lease agreement for both parties.

Benefits and Drawbacks for Prospective Lessees

For individuals considering a house lease, particularly a lease-to-own arrangement, a balanced understanding of its financial advantages and disadvantages is essential for informed decision-making.

Advantages: Pathway to Homeownership, Credit Building, Flexibility

One of the primary financial benefits of leasing a house is that it offers a viable pathway to homeownership for those who may not immediately qualify for a traditional mortgage due due to a low credit score, insufficient down payment savings, or self-employment income challenges. The lease period provides lessees with time to improve their credit profile, save for a larger down payment through rent credits, and stabilize their financial situation. Moreover, making timely lease payments can positively impact credit scores if reported to credit bureaus, further strengthening their mortgage application prospects. While residing in the home, lessees also gain practical experience with the responsibilities and costs of homeownership, such as maintenance and utilities, which can be invaluable financial preparation. This “trial run” can prevent future financial shocks associated with homeownership.

Disadvantages: Higher Costs, Limited Appreciation, Potential Loss of Fees

Despite the allure of eventual homeownership, house leasing carries significant financial drawbacks. Monthly lease payments are typically higher than standard rent, and the upfront option fee can be substantial and is almost always non-refundable. If the lessee ultimately decides not to purchase the property, or if they cannot secure financing at the end of the lease term, all accumulated rent credits and the initial option fee are forfeited, representing a considerable financial loss. This makes the agreement highly conditional on the lessee’s ability to complete the purchase. Furthermore, while the lessee is paying towards the property, they do not accrue actual equity in the home during the lease term. Any market appreciation only benefits the lessor until the purchase is finalized, meaning the lessee misses out on potential investment gains. There’s also the risk that the property’s value could decline, making the predetermined purchase price higher than market value at the time of option exercise, trapping the lessee in an unfavorable financial position or forcing them to walk away and lose their investment.

Financial Considerations for Property Owners (Lessors)

From the perspective of a property owner, leasing a house also presents a unique set of financial opportunities and risks that must be carefully evaluated.

Consistent Income Stream and Tenant Stability

For lessors, a house lease agreement can provide a consistent and often higher income stream compared to traditional renting, due to the premium incorporated into monthly payments and the upfront option fee. This premium helps offset carrying costs and potentially contributes to the lessor’s overall investment return. Furthermore, lessees in lease-to-own agreements tend to be more stable and responsible tenants, as they have a vested interest in the property’s future condition and a clear financial incentive to fulfill their contractual obligations, including making timely payments. This reduces turnover rates, minimizing vacancy periods and the associated costs of marketing, cleaning, and preparing the property for new tenants. The long-term nature of these agreements also offers predictability in financial planning.

Tax Implications and Depreciation

Lessors must also consider the tax implications of a house lease. During the lease term, the property is generally still considered an investment property in the eyes of tax authorities. This means the lessor can continue to claim deductions for mortgage interest, property taxes, insurance, and crucially, depreciation. Depreciation deductions can significantly reduce a lessor’s taxable income, improving the net financial return on the property. However, when the purchase option is exercised, the sale of the property will trigger capital gains taxes, the calculation of which will be influenced by the adjusted basis (original cost minus depreciation) and the final sale price. Lessors need to work with a financial advisor to understand how these elements impact their overall tax liability and investment strategy.

Risk Mitigation and Property Management

While lease agreements often shift some maintenance responsibilities to the lessee, lessors still bear residual risks. The primary risk is that the lessee may ultimately default on payments or fail to exercise the purchase option, leading to the forfeiture of the option fee and rent credits but potentially forcing the lessor to find a new buyer or tenant. This can result in periods of vacancy and additional marketing costs. To mitigate this, lessors must carefully vet prospective lessees’ financial stability and creditworthiness. From a property management standpoint, while lessees with an ownership mindset may require less day-to-day oversight, lessors must still ensure compliance with the lease terms, particularly regarding property maintenance, to protect their asset until the sale is complete.

Navigating the Lease-to-Own Process: Financial Due Diligence

Successfully engaging in a house lease, especially with a purchase option, requires meticulous financial due diligence and strategic planning from the lessee’s perspective.

Reviewing the Lease Agreement Critically

The lease agreement is a complex financial and legal document that dictates all terms of the arrangement. Lessees must review it critically, paying close attention to the purchase price, the option fee amount and its non-refundable nature, the portion of monthly payments credited towards purchase, and the specific timeline for exercising the option. Clauses regarding maintenance responsibilities, property taxes, insurance, and penalties for late payments or default are equally important. Engaging an independent real estate attorney to review the contract is not an option but a necessity. This professional guidance ensures that the lessee fully understands their financial obligations, rights, and the potential risks involved, preventing costly misunderstandings down the line.

Financial Planning for the Purchase Phase

The lease period serves as a crucial window for financial preparation for the eventual purchase. Lessees should prioritize improving their credit score, reducing existing debt, and saving additional funds beyond the accumulated rent credits for a down payment and closing costs. It’s advisable to meet with a mortgage lender early in the lease term to understand their qualifying criteria and receive guidance on necessary financial adjustments. Establishing a clear budget that accounts for both current lease payments and future mortgage obligations, property taxes, insurance, and potential homeownership expenses is vital. A robust financial plan will dictate the success of transitioning from lessee to homeowner, ensuring the investment made during the lease term culminates in property acquisition.

Consulting Financial and Legal Professionals

Given the significant financial commitments and complexities involved, consulting both financial advisors and legal professionals is indispensable for anyone considering leasing a house with a purchase option. A financial advisor can help assess the long-term affordability, evaluate the investment potential, and strategize for mortgage qualification. They can also help compare the financial benefits and risks of a lease-to-own against other housing options. A real estate attorney, as mentioned, is critical for reviewing the lease agreement, clarifying legal nuances, protecting the lessee’s interests, and ensuring that all terms are fair and legally sound. These professionals provide the expert guidance needed to navigate the intricate financial landscape of house leasing, mitigating risks and optimizing the pathway to homeownership.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.