Indiana, often recognized for its agricultural heritage, burgeoning tech sector, and vibrant motorsports culture, also boasts a distinct and generally favorable state tax structure that impacts residents, businesses, and investors. Understanding the intricacies of Indiana’s tax landscape is crucial for effective personal finance planning, business budgeting, and investment strategies within the Hoosier State. This comprehensive overview delves into the various components of Indiana’s state and local tax system, shedding light on what taxpayers can expect and how to navigate their financial obligations.

Understanding Indiana’s Income Tax System

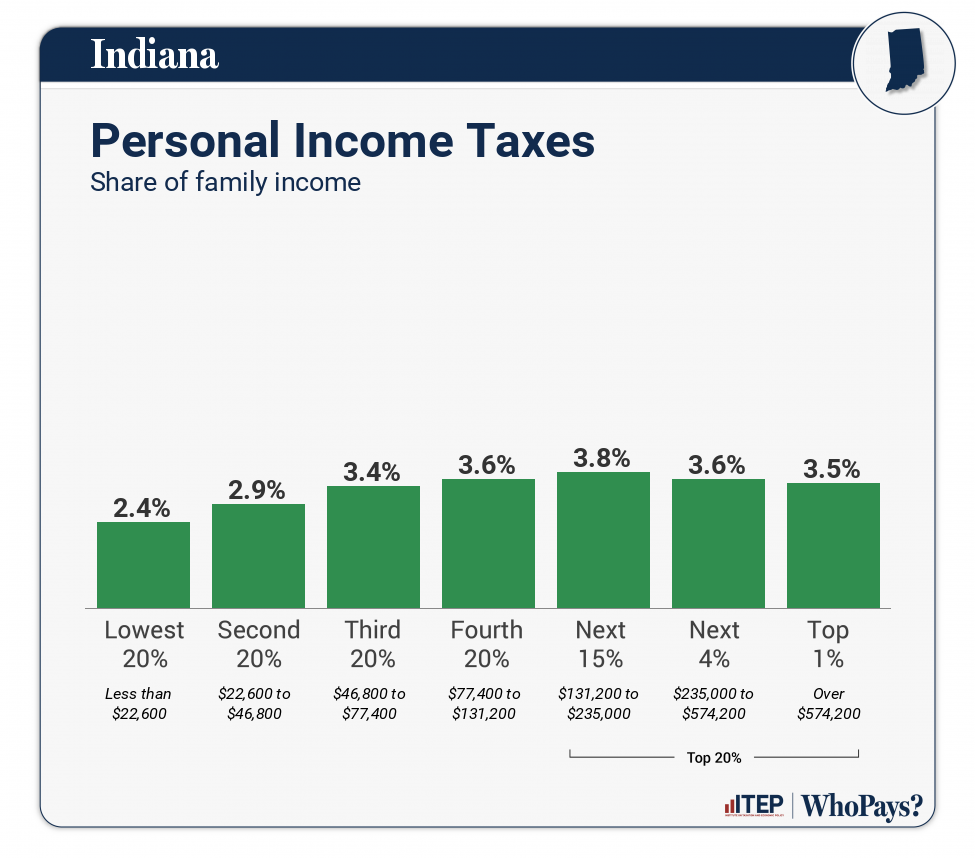

Indiana employs a relatively straightforward income tax system that combines a flat state rate with additional local county taxes. This dual structure means that while the state tax rate is consistent, the total income tax burden can vary significantly depending on where one lives or earns income within Indiana.

Individual Income Tax

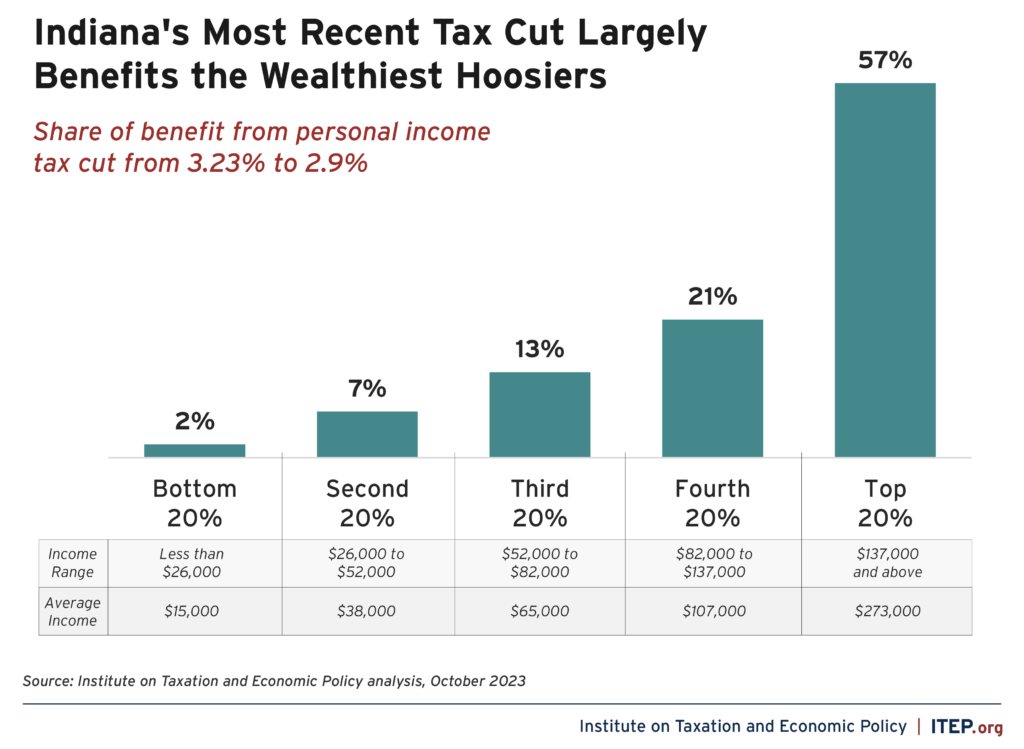

At the state level, Indiana imposes a flat income tax rate on all taxable income. This means that regardless of how much an individual earns, the same percentage applies, distinguishing it from progressive tax systems where rates increase with income. For many years, Indiana has aimed to maintain a competitive flat rate to attract and retain residents and businesses.

Beyond the state levy, nearly all Indiana counties impose their own local income taxes. These county rates vary widely across the state, ranging from zero in a few select counties to over 3%. Crucially, these county income taxes are generally deductible for federal income tax purposes if you itemize. Residents are typically subject to the county income tax rate of their county of residence as of January 1st, while non-residents working in a county with a local income tax may also be subject to that county’s rate on income earned there. This layered approach necessitates that individuals understand both the statewide rate and their specific county’s contribution to accurately project their total income tax liability.

Taxable income for Indiana purposes largely mirrors federal adjusted gross income (AGI), with a few state-specific modifications. Residents and non-residents earning income in Indiana are required to file Form IT-40 or IT-40PNR, respectively.

Business Income Tax

Indiana’s approach to business taxation is multifaceted, primarily focusing on the Corporate Adjusted Gross Income (AGI) tax. This tax is levied on the adjusted gross income of corporations doing business in Indiana. The state has consistently worked to reduce this rate over time, aiming to foster a business-friendly environment.

For pass-through entities, such as S-corporations, partnerships, and most limited liability companies (LLCs), the business itself is generally not subject to the corporate AGI tax. Instead, the income “passes through” to the owners’ individual tax returns, where it is taxed at the individual income tax rates (state and county). This structure avoids double taxation—once at the corporate level and again at the individual level—making Indiana an attractive state for entrepreneurs and small businesses structured as pass-through entities.

Financial institutions, including banks and credit unions, are subject to a specific financial institutions tax rather than the general corporate AGI tax. This specialized tax recognizes the unique nature of financial services within the economy.

Withholding and Estimated Taxes

For most employees, Indiana income taxes (state and county) are withheld from their paychecks throughout the year. Employers are responsible for remitting these withheld amounts to the Indiana Department of Revenue. Self-employed individuals, independent contractors, and those with significant income from investments or other sources not subject to withholding are generally required to make estimated tax payments quarterly. Failing to make sufficient estimated tax payments can result in penalties, underscoring the importance of careful financial planning for non-wage earners.

Indiana Sales Tax: What You Need to Know

Indiana levies a statewide sales tax on the retail sale of tangible personal property and certain services. The sales tax rate has remained stable for an extended period, providing consistency for consumers and businesses alike.

Currently, the Indiana sales tax rate is 7%. This tax applies to a broad range of goods purchased for consumption, use, or storage in Indiana. Examples include clothing, electronics, vehicles, and most restaurant meals. Businesses are responsible for collecting this tax from customers and remitting it to the state.

Common Exemptions

While the sales tax applies widely, Indiana provides several significant exemptions designed to reduce the tax burden on essential goods and promote specific economic activities:

- Food for Home Consumption: Most groceries purchased for preparation and consumption at home are exempt from sales tax. This exemption helps alleviate the financial burden on households for basic necessities.

- Prescription Drugs and Medical Devices: Essential health-related items, including prescription medications and many medical devices, are exempt.

- Manufacturing Equipment: Purchases of certain machinery and equipment used directly in manufacturing are exempt, a policy aimed at encouraging industrial growth and job creation within the state.

- Agricultural Equipment: Machinery and equipment used in agricultural production are often exempt to support the state’s significant farming industry.

- Utilities: Residential utility services, such as electricity, natural gas, and water, are generally exempt from sales tax.

Use Tax

Indiana also imposes a use tax at the same rate as the sales tax. The use tax applies to purchases of tangible personal property or specified services made outside of Indiana for use, storage, or consumption within the state, where Indiana sales tax was not collected by the seller. This often occurs with online purchases from out-of-state retailers who do not have a physical presence (nexus) in Indiana. Residents are responsible for remitting this use tax directly to the state, typically when filing their annual income tax return. Failure to report and pay use tax can lead to penalties.

Property Taxes in Indiana: A Local Burden

Unlike income and sales taxes, which are primarily state-administered (with county add-ons for income), property taxes in Indiana are almost entirely a local affair. They are assessed, collected, and utilized by local governmental units—counties, townships, cities, towns, and school corporations—to fund public services such as schools, police and fire protection, roads, and libraries.

Assessment Process

Property taxes are levied on both real property (land and buildings) and business personal property (machinery, equipment, inventory for businesses). County assessors are responsible for valuing all taxable property within their jurisdiction. Properties are assessed at their market value, meaning the price a willing buyer would pay a willing seller in an arm’s-length transaction. Assessments are conducted periodically, and taxpayers have the right to appeal their property’s assessed value if they believe it is incorrect.

Property Tax Caps (Circuit Breaker)

A unique and significant feature of Indiana’s property tax system is its “circuit breaker” property tax caps. These caps limit the maximum amount of property tax that can be charged on different types of property, regardless of the assessed value or the local tax rates. The caps are:

- 1% of assessed value for homesteads (owner-occupied residences).

- 2% of assessed value for residential rental properties and agricultural land.

- 3% of assessed value for all other real property and business personal property.

These caps provide a crucial safeguard against excessively high property tax bills, offering predictability and protection for homeowners and businesses. If the calculated tax bill exceeds these percentages of the property’s gross assessed value, the amount is “capped” at the maximum allowable percentage.

Homestead Exemptions and Other Deductions

Indiana offers several deductions and exemptions that can reduce a property’s assessed value, thereby lowering the tax bill. The most significant of these is the Homestead Deduction, which provides a substantial reduction in assessed value for owner-occupied primary residences. Other common deductions include:

- Mortgage Deduction: For properties with a mortgage.

- Supplemental Homestead Deduction: Provides an additional reduction for homesteads.

- Over 65 Deduction: For qualifying seniors.

- Disabled Veteran Deduction: For veterans with service-connected disabilities.

Utilizing these deductions is vital for homeowners to minimize their property tax obligations. Applications for deductions are typically filed with the county auditor’s office.

Other Key Indiana Taxes and Fees

Beyond the primary income, sales, and property taxes, Indiana has several other taxes and fees that contribute to state and local revenue and impact specific sectors of the economy.

Fuel Taxes

Indiana levies excise taxes on gasoline and special fuels (like diesel). These taxes are typically included in the price at the pump and are a significant source of funding for road and bridge construction and maintenance across the state. The rates are subject to change and impact transportation costs for individuals and businesses.

Vehicle Excise Tax

When registering a motor vehicle in Indiana, owners must pay an annual excise tax. This tax is based on the vehicle’s age and manufacturer’s retail price (MSRP) when new, categorizing vehicles into different classes. The excise tax is in lieu of property tax on vehicles, reflecting a simplified approach to taxing personal automobiles.

Gaming Taxes

Indiana generates substantial revenue from various forms of legal gambling, including the state lottery, riverboat casinos, and racinos. These activities are subject to specific gaming taxes and fees, which contribute significantly to the state’s general fund and other designated programs.

Inheritance and Estate Taxes (Repealed)

It’s important to note that Indiana does not currently impose a state-level inheritance tax or estate tax. The inheritance tax was repealed for individuals who died after December 31, 2012. This absence simplifies estate planning for residents and can be a significant financial advantage compared to states that still levy such taxes.

Navigating Indiana Tax Credits and Deductions

To further influence economic behavior, support specific industries, or provide relief to taxpayers, Indiana offers various tax credits and deductions. These can reduce an individual’s or business’s tax liability dollar-for-dollar (credits) or by reducing taxable income (deductions).

Common examples of state-specific credits and deductions include:

- College Savings Deductions: Contributions to the Indiana CollegeChoice 529 plan are eligible for a state income tax credit.

- Residential Historic Rehabilitation Tax Credit: Encourages the preservation of historic homes.

- Economic Development Credits: Various credits are offered to businesses that create jobs, make significant capital investments, or locate in specific economic development zones.

- Research and Development Tax Credit: Modeled after the federal credit, this incentivizes innovation and technological advancements.

- Teacher Creativity Grants Credit: Supports educators in professional development.

Staying informed about available credits and deductions is crucial for optimizing one’s financial position in Indiana. Given the complexity and potential for changes in tax law, consulting with a qualified tax professional is highly recommended to ensure compliance and maximize benefits for both individuals and businesses. Understanding the full scope of Indiana’s tax system is an essential component of sound financial management in the Hoosier State.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.